The past few weeks have seen global government bond market prices sell off (rising yields) due to worries about the spike in global energy prices from the Iran War creating problematic inflation, and in turn, prompting central banks hold their interest rates steady or even tighten their monetary policies.

More recently, however, bond traders’ attitudes have flip-flopped as prices this week have rallied (lower yields) due to revised notions that a prolonged war in Iran, including the associated higher energy costs, would be a significant drag on world economies, prompting central banks to lower their interest rates.

So which theory is correct? The answer to that question is that at present, nobody knows. What recent price action in the bond markets does once again prove is that traders and markets are fickle — even the bond traders, who many consider to be the smartest guys and gals in the room.

My Bias and What the Gold Market Is Telling Us

In the paragraph above I said nobody knows what the war in the Middle East will do to inflation. However, like many others, I have an opinion and it is this: The energy price spike will not last long — maybe a couple more months.

However, I don’t think that Nymex WTI crude oil (CLK26) will drop back down to the $60 to $65 a barrel area that was seen in the weeks before the war started. My bias is that WTI crude prices will be trading in the $70 to $80 range by mid-summer. Why? Right now, there is a major “war premium” baked into the price of crude oil. While that war premium will significantly shrink in the coming weeks, it won’t completely evaporate for a long time to come.

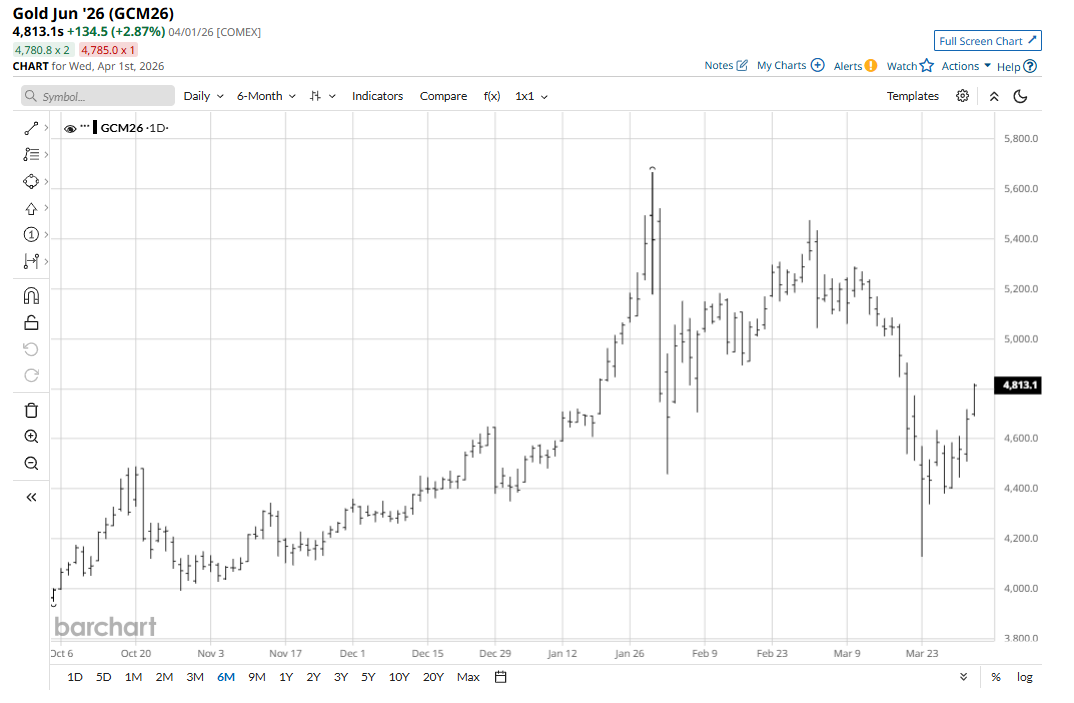

If I am correct, any significant rise in inflation will only be temporary. That’s what the gold (GCM26) market is also presently telling us.

Gold’s rally of around $600 off the late-March low is suggesting global interest rates will not significantly rise and may even decline in the coming months. Ironically, gold prices are rallying despite risk aversion in the general marketplace that is receding. For sure there is still safe-haven demand for gold as the Middle East war is still running hot. However, the bigger bullish drivers for the gold market at present are ideas that the war won’t be a long one and that central banks won’t have to tighten their monetary policies due to inflation fears. That scenario extrapolates into much better consumer and commercial demand for precious metals in the coming months.

My opinion on any problematic inflation not occurring, or at worst being just a blip, is bullish for stock and bond markets, as well as other raw commodity markets.

Gold and silver (SIK26) markets are in major, extended bull runs. Many veteran market watchers would call that a tired trade. I do think there is more price upside for gold and silver in the very near term and in the very long term. However, I agree with the tired trade moniker for the two metals. I also believe commodity market speculators are eyeing other sectors for the next major bull market run. I think that sector will be the grains. Stay tuned!

Tell me what you think. I enjoy hearing from my valued Barchart readers from all around the globe. Email me at jim@jimwyckoff.com.

On the date of publication, Jim Wyckoff did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.