Palantir Technologies, Inc. (PLTR) stock may be forming a bottom here. Its underlying value is much higher. As a result, it makes sense to sell short out-of-the-money (OTM) puts in PLTR with one-month expiry and use the proceeds to buy 6-month in-the-money (ITM) PLTR calls.

PLTR is now down to $128.71 in midday trading on Feb. 24. It's down over $65 from $194.17 on Dec. 24, 2025, a 33% drop in 2 months. That provides a huge opportunity for value buyers.

I described Palantir's underlying value in a recent Feb 18 Barchart article and how to play it in a follow-up February 22 Barchart article, “If Palantir is Near a Bottom, What's the Best Play in PLTR Stock?”

I showed that PLTR could be worth between $189 and $245 over the next year, and one play was to sell short one-month out-of-the-money (OTM) puts at the $120 and $125 strike prices.

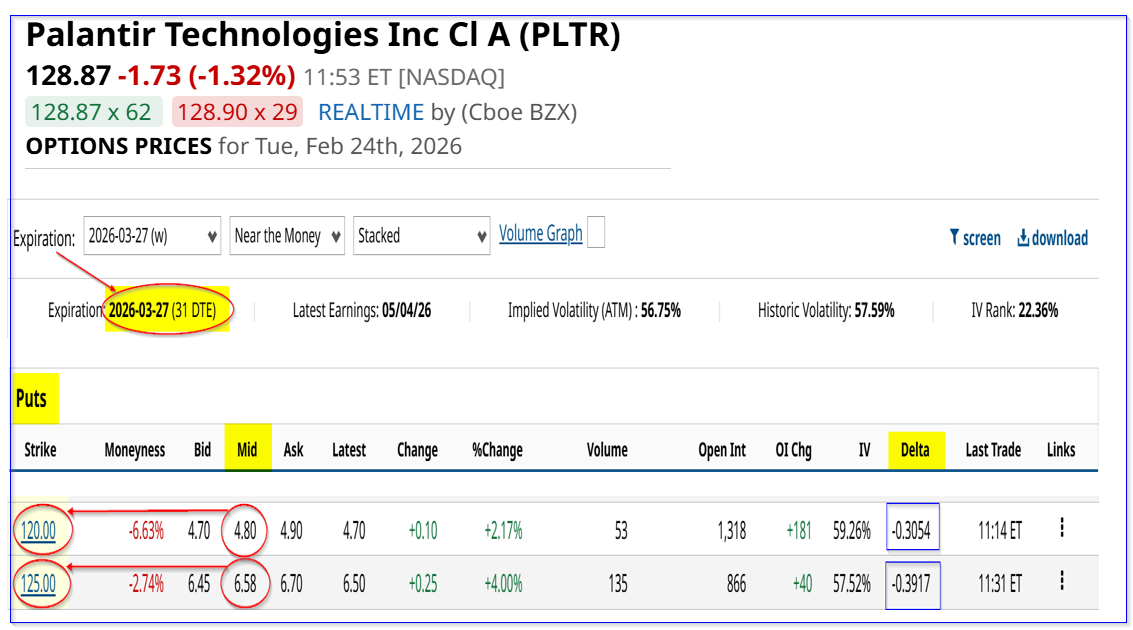

Shorting OTM One-Month Puts

The reason is that the premiums are high and also provide a high one-month yield and potentially lower buy-in breakeven points.

For example, the $125 strike price put expiring March 27 has a midpoint premium of $6.58 and $4.80 for the $120 strike price put.

That means the investor who shorts either one of these puts makes an immediate yield of 5.264% ($6.58/$125.00) or $4.0% ($4.80/$120.00) over the next month.

The idea here is that this sets a potentially lower attractive breakeven buy-in point for value investors:

$125 - $6.58 = $118.42 breakeven, i.e., -8.1% lower

$120 - $4.80 - $115.20 breakeven, i.e., -10.6% lower

In addition, if the investor can repeat this income play over the next 3 months, assuming there is no assignment, it could help pay for the purchase of an in-the-money (ITM) call.

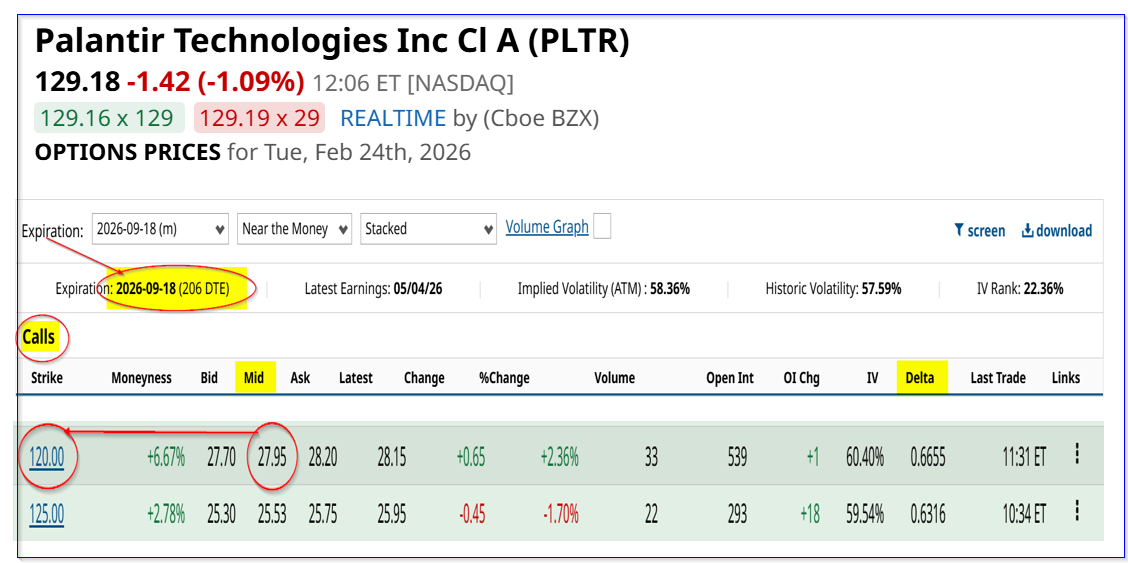

Buying In-the-Money (ITM) Long-Dated Calls

For example, the Sept. 18 call option, which is 206 days to expiry (DTE), at the $120.00 strike price has a midpoint premium of $27.95.

That means the breakeven point is $147.95, which is $18.77 higher than today's price of $129.18. The $18.77 part is known as the extrinsic value portion of the premium paid.

That extrinsic value could be more than paid for by an investor who shorts one-month put options and collects $4.80 each month:

$4.80 x 6 = $28.80

Now, there is no guarantee that an investor can continue to collect $4.80 each month by shorting out-of-the-money puts. But it would help mitigate the call option purchase.

So why do this? The answer is that it leverages the investor's potential upside in owning PLTR.

Potential Upside

Let's say an investor is willing to buy 100 shares of PLTR today, costing them $12,918. The better play is to short the March 27 $120.00 put option, by paying $12,000 in collateral, and then buying a Sept. 18 call at the $120 strike price.

Here is how that works out:

Cost: PLTR Put collateral: $12,000 (100 x $120)

PLTR Call: $2,795 (100 x $27.95)

Total Cost ……………..$14,795

Net Income: Shorting PLTR OTM puts for 6 months: $4.80 x 6 x 100 = $2,800

Net Cost …………………. $14,795-$2,800 = $11,915

Let's say that by Sept. 18, 2026, PLTR has recovered to $180.00. Here is the potential return:

Call option value: $180 - $120 strike = $60.00 x 100 = $6,000

Return on Investment: $6,000 / $11,915 = 50.4%

Note that the $12,000 secured collateral is actually not even a forever outlay, since, unless PLTR falls to $120 over the next month, that collateral is released by the brokerage firm to the investor. So the potential return is exponentially much higher.

Note that an investor today in PLTR stock, if PLTR closes at $180.00 on Sept. 18, makes just 39%:

$180/$129.18 = 1.393

So, this shows that the short-put one-month play combined with a 6-month call buy is a better play.

Downside Risk and Protection

Moreover, the investor also has downside protection in the ITM call purchase.

For example, let's say that PLTR stays at $130.00 by Sept. 18. Here is the downside:

$130-$120 = $10 x 100 = $1,000

+ Short Put income: $2,800: Total Value: $3,800

Net: $2,795 call option cost - $3,800 value left = $1,005 return over 6 months

$1,005 / $12,000 collateral invested = 0.08375 = 8.375% over 6 months, or 16.75% annualized

The bottom line is that the investor still makes at least 8.375% or 16.4% annualized even if PLTR stays flat.

That is why doing this play, given PLTR's high put OTM premiums and low ITM call prices, is attractive.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Microsoft Stock Just Flashed an Ultra-Rare Bullish Signal for Options Traders

- Buying In-the-Money Palantir Calls Looks Attractive Here for Value Buyers

- Are the Best Days Over for IBM Stock? What Price Volatility Tells Us and How You Can Trade IBM Now.

- The Smart Way to Bet Against Snowflake Stock Before Earnings on February 25