What a time it’s been for Mercury Systems. In the past six months alone, the company’s stock price has increased by a massive 50.1%, reaching $110.84 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Mercury Systems, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Mercury Systems Not Exciting?

Despite the momentum, we’re swiping left on Mercury Systems for now. Here are three reasons you should be careful with MRCY, plus one stock we’d rather own.

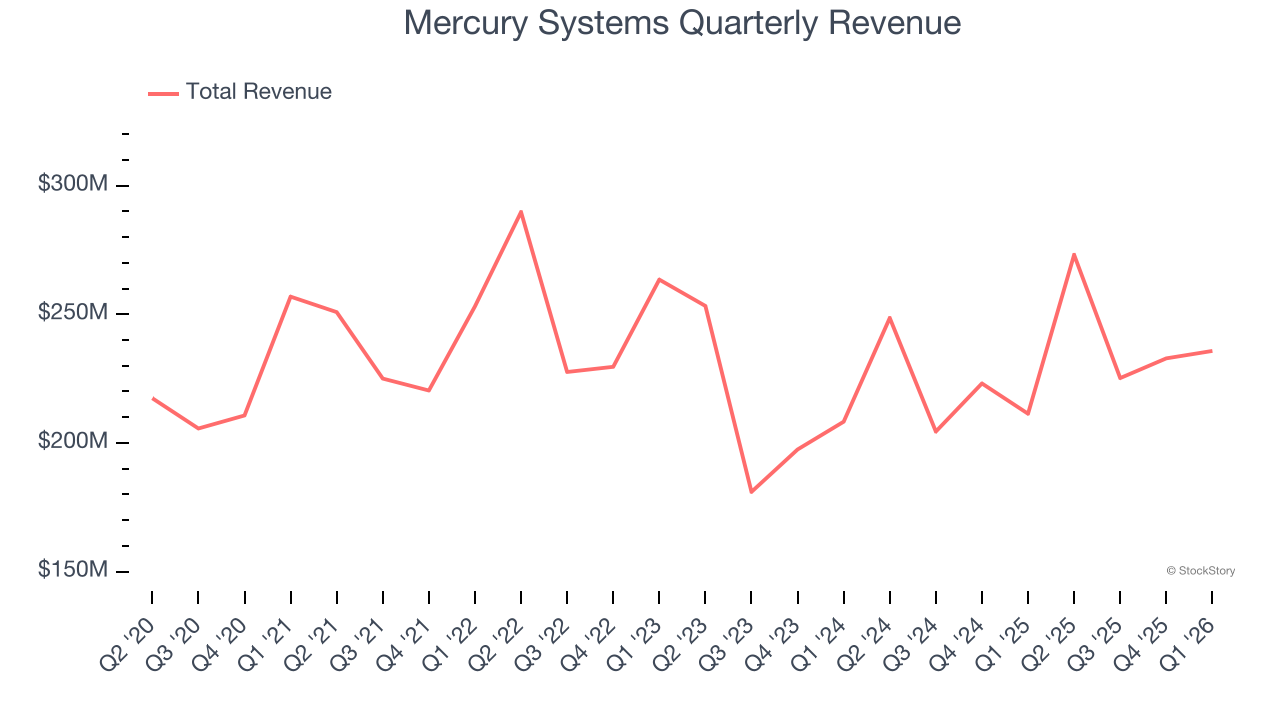

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Mercury Systems’s sales grew at a sluggish 1.7% compounded annual growth rate over the last five years. This was below our standards.

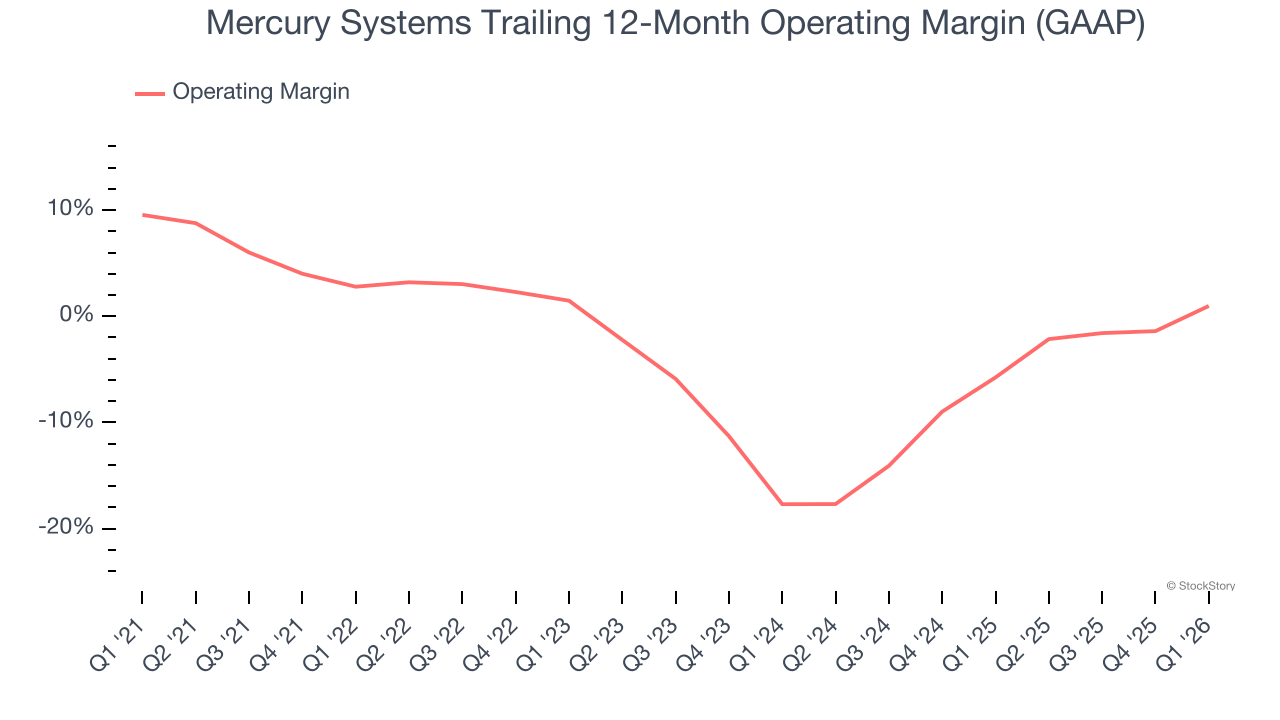

2. Operating Losses Sound the Alarm

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Although Mercury Systems was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 3.2% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

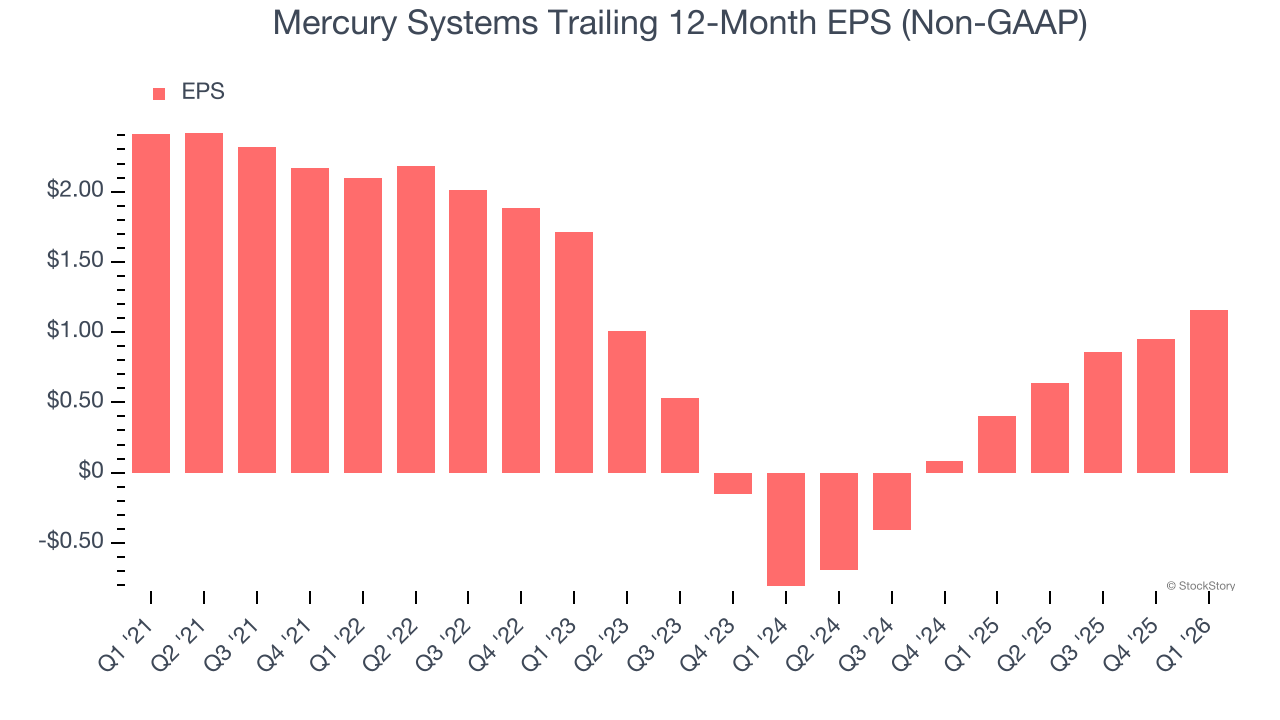

3. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Mercury Systems, its EPS declined by 13.6% annually over the last five years while its revenue grew by 1.7%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Mercury Systems isn’t a terrible business, but it doesn’t pass our quality test. After the recent surge, the stock trades at 78.9× forward P/E (or $110.84 per share). At this valuation, there’s a lot of good news priced in - you can find more timely opportunities elsewhere. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

Stocks We Like More Than Mercury Systems

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.