Let’s dig into the relative performance of CoStar (NASDAQ: CSGP) and its peers as we unravel the now-completed Q1 data & business process services earnings season.

A combination of increasing reliance on data and analytics across various industries and the desire for cost efficiency through outsourcing could mean that companies in this space gain. As functions such as payroll, HR, and credit risk assessment rely on more digitization, key players in the data & business process services industry could be increased demand. On the other hand, the sector faces headwinds from growing regulatory scrutiny on data privacy and security, with laws like GDPR and evolving U.S. regulations potentially limiting data collection and monetization strategies. Additionally, rising cyber threats pose risks to firms handling sensitive personal and financial information, creating outsized headline risk when things go wrong in this area.

The 9 data & business process services stocks we track reported a strong Q1. As a group, revenues beat analysts’ consensus estimates by 2.5% while next quarter’s revenue guidance was in line.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 6.1% since the latest earnings results.

CoStar (NASDAQ: CSGP)

With a research department that makes over 10,000 property updates daily to its 35-year-old database, CoStar Group (NASDAQ: CSGP) provides comprehensive real estate data, analytics, and online marketplaces for commercial and residential properties in the U.S. and U.K.

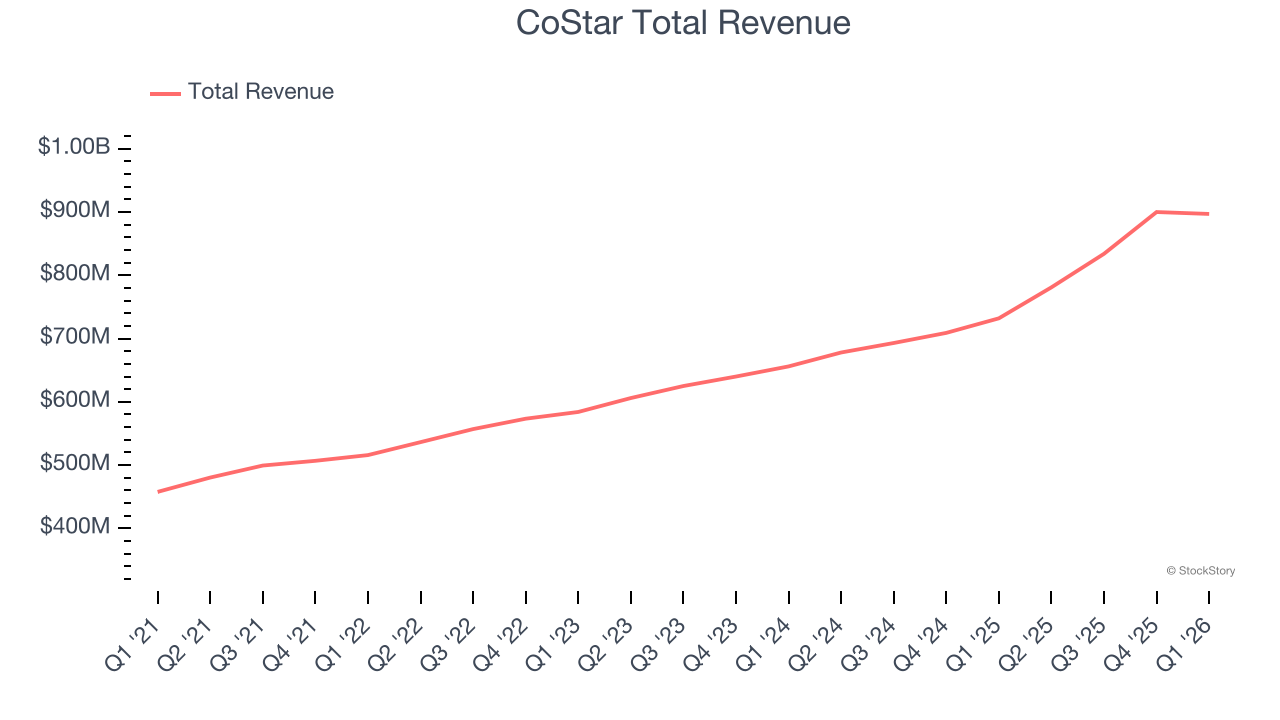

CoStar reported revenues of $897 million, up 22.5% year on year. This print was in line with analysts’ expectations, and overall, it was a strong quarter for the company with a beat of analysts’ EPS estimates.

“CoStar Group produced $67 million in net new bookings in the first quarter of 2026, an increase of 20% year-over-year. We have delivered 60 consecutive quarters of consistent, double-digit revenue growth in a wide range of economic conditions,” said Andy Florance, Founder and Chief Executive Officer of CoStar Group.

CoStar scored the highest full-year guidance raise but had the weakest performance against analyst estimates of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 8.9% since reporting and currently trades at $32.75.

Is now the time to buy CoStar? Access our full analysis of the earnings results here, it’s free.

Best Q1: Fair Isaac Corporation (NYSE: FICO)

Creator of the three-digit number that can determine whether you get a mortgage or credit card, Fair Isaac Corporation (NYSE: FICO) develops analytics software and the widely used FICO Score, which is the standard measure of consumer credit risk in the United States.

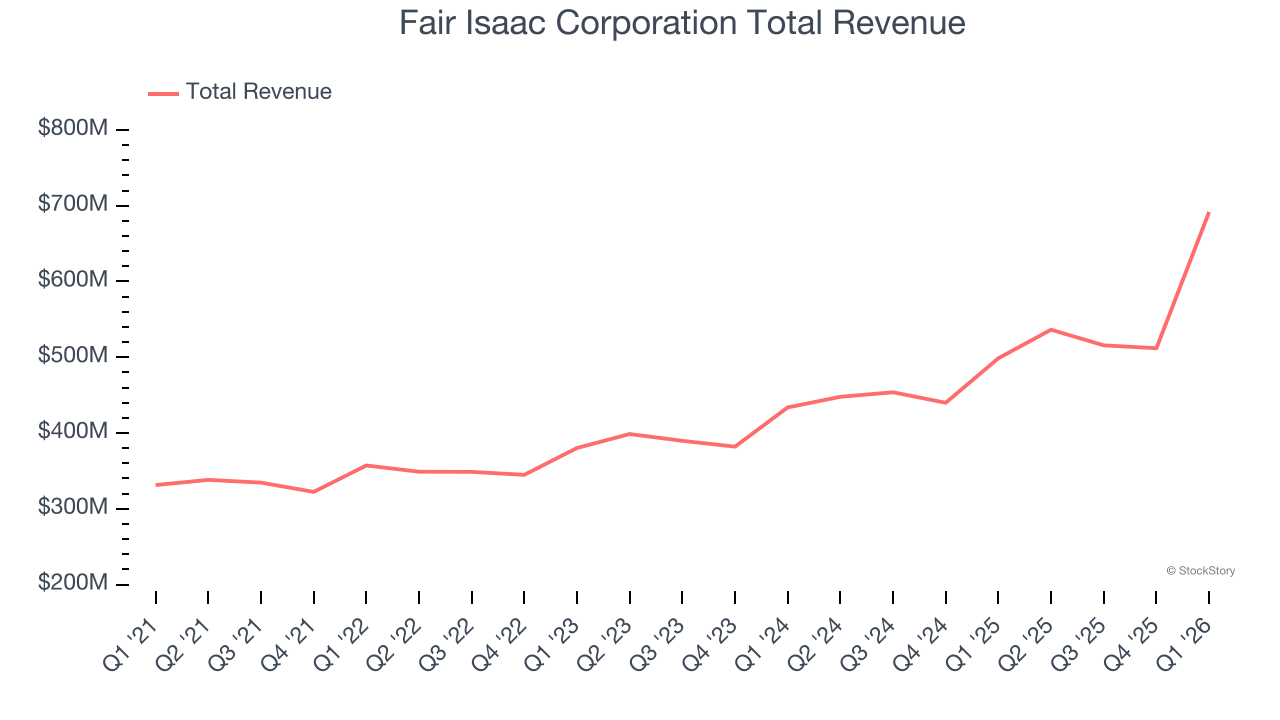

Fair Isaac Corporation reported revenues of $691.7 million, up 38.7% year on year, outperforming analysts’ expectations by 9.1%. The business had a very strong quarter with a solid beat of analysts’ ARR estimates and an impressive beat of analysts’ revenue estimates.

Fair Isaac Corporation scored the biggest analyst estimates beat and fastest revenue growth among its peers. The market seems happy with the results as the stock is up 8.7% since reporting. It currently trades at $1,099.

Is now the time to buy Fair Isaac Corporation? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: TransUnion (NYSE: TRU)

One of the three major credit bureaus in the United States alongside Equifax and Experian, TransUnion (NYSE: TRU) is a global information and insights company that provides credit reports, fraud prevention tools, and data analytics to help businesses make decisions and consumers manage their financial health.

TransUnion reported revenues of $1.25 billion, up 13.7% year on year, exceeding analysts’ expectations by 2.7%. Still, it was a mixed quarter as it posted a miss of analysts’ full-year EPS guidance estimates.

As expected, the stock is down 6.9% since the results and currently trades at $66.28.

Read our full analysis of TransUnion’s results here.

SS&C (NASDAQ: SSNC)

Founded in 1986 as a bridge between technology and financial services, SS&C Technologies (NASDAQ: SSNC) provides software and software-enabled services that help financial firms and healthcare organizations automate complex business processes.

SS&C reported revenues of $1.65 billion, up 8.8% year on year. This result surpassed analysts’ expectations by 1.1%. It was a satisfactory quarter as it also logged a narrow beat of analysts’ billings estimates.

The stock is down 7.8% since reporting and currently trades at $64.57.

Read our full, actionable report on SS&C here, it’s free.

Verisk (NASDAQ: VRSK)

Processing over 2.8 billion insurance transaction records annually through one of the world's largest private databases, Verisk Analytics (NASDAQ: VRSK) provides data, analytics, and technology solutions that help insurance companies assess risk, detect fraud, and make better business decisions.

Verisk reported revenues of $782.6 million, up 3.9% year on year. This print topped analysts’ expectations by 1.3%. Aside from that, it was a satisfactory quarter as it also logged a beat of analysts’ EPS estimates but full-year EPS guidance in line with analysts’ estimates.

Verisk had the slowest revenue growth among its peers. The stock is down 8.4% since reporting and currently trades at $161.78.

Read our full, actionable report on Verisk here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.