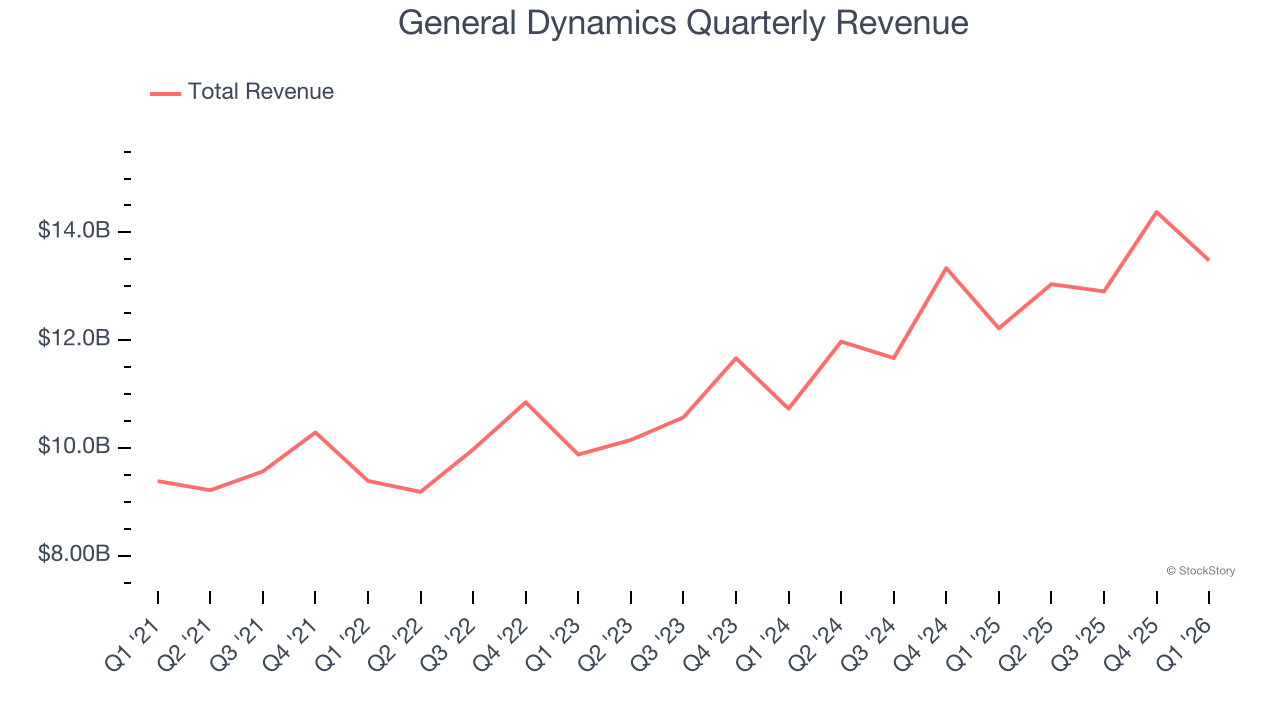

Aerospace and defense company General Dynamics (NYSE: GD) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 10.3% year on year to $13.48 billion. Its GAAP profit of $4.10 per share was 11% above analysts’ consensus estimates.

Is now the time to buy General Dynamics? Find out by accessing our full research report, it’s free.

General Dynamics (GD) Q1 CY2026 Highlights:

- Revenue: $13.48 billion vs analyst estimates of $12.73 billion (10.3% year-on-year growth, 5.9% beat)

- EPS (GAAP): $4.10 vs analyst estimates of $3.69 (11% beat)

- Adjusted EBITDA: $1.59 billion vs analyst estimates of $1.52 billion (11.8% margin, 4.6% beat)

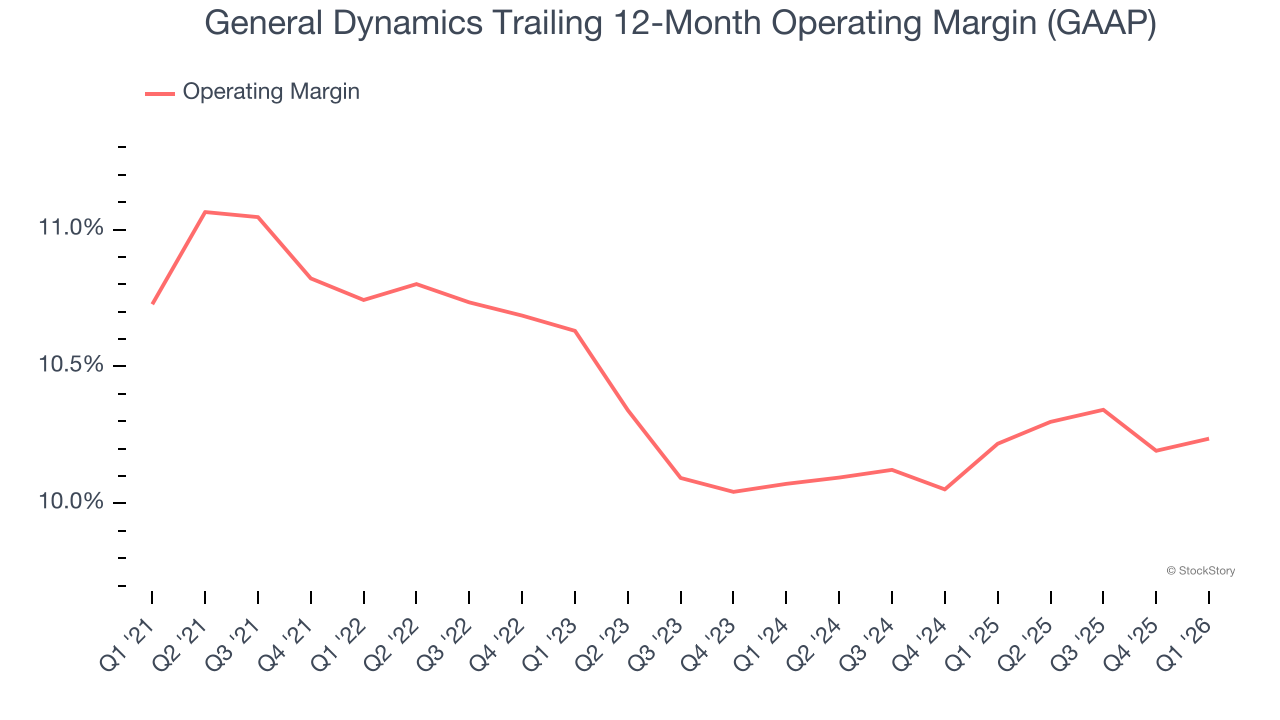

- Operating Margin: 10.5%, in line with the same quarter last year

- Free Cash Flow was $1.95 billion, up from -$290 million in the same quarter last year

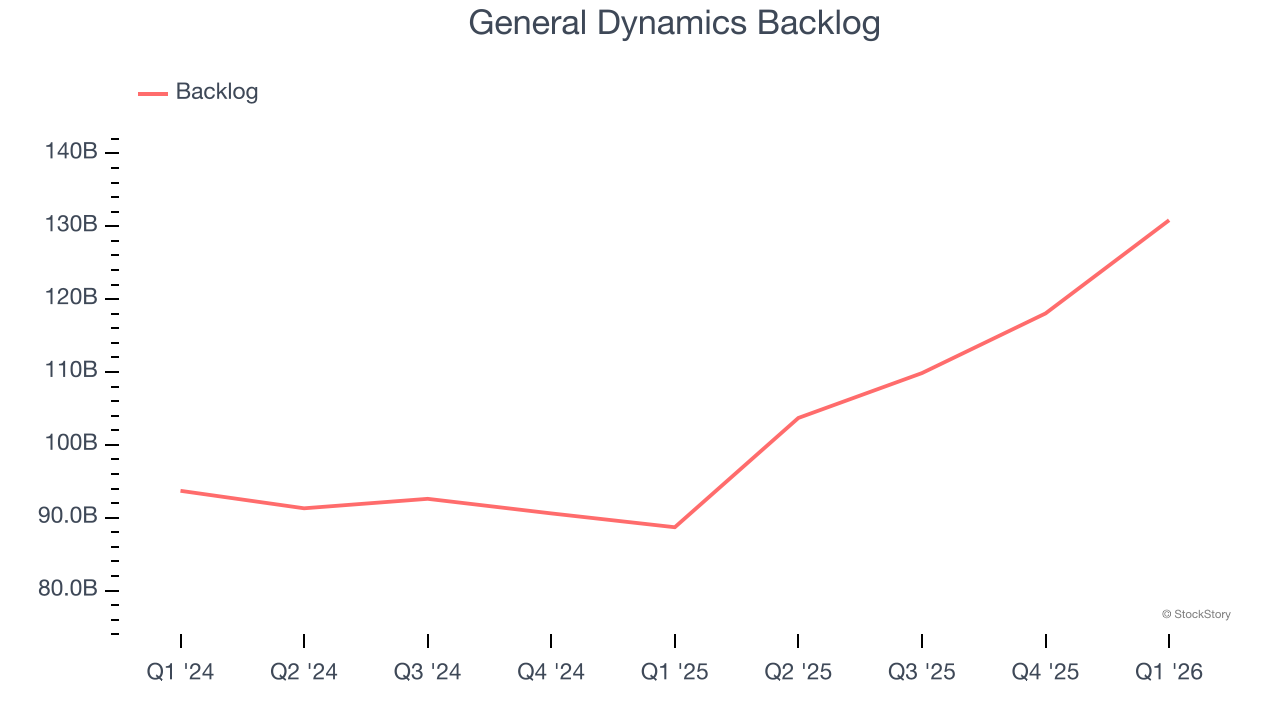

- Backlog: $130.8 billion at quarter end, up 47.5% year on year

- Market Capitalization: $84.83 billion

"Our businesses had a very good start to the year, delivering strong operating results and excellent cash conversion," said Phebe Novakovic, chairman and chief executive officer.

Company Overview

Creator of the famous M1 Abrahms tank, General Dynamics (NYSE: GD) develops aerospace, marine systems, combat systems, and information technology products.

Revenue Growth

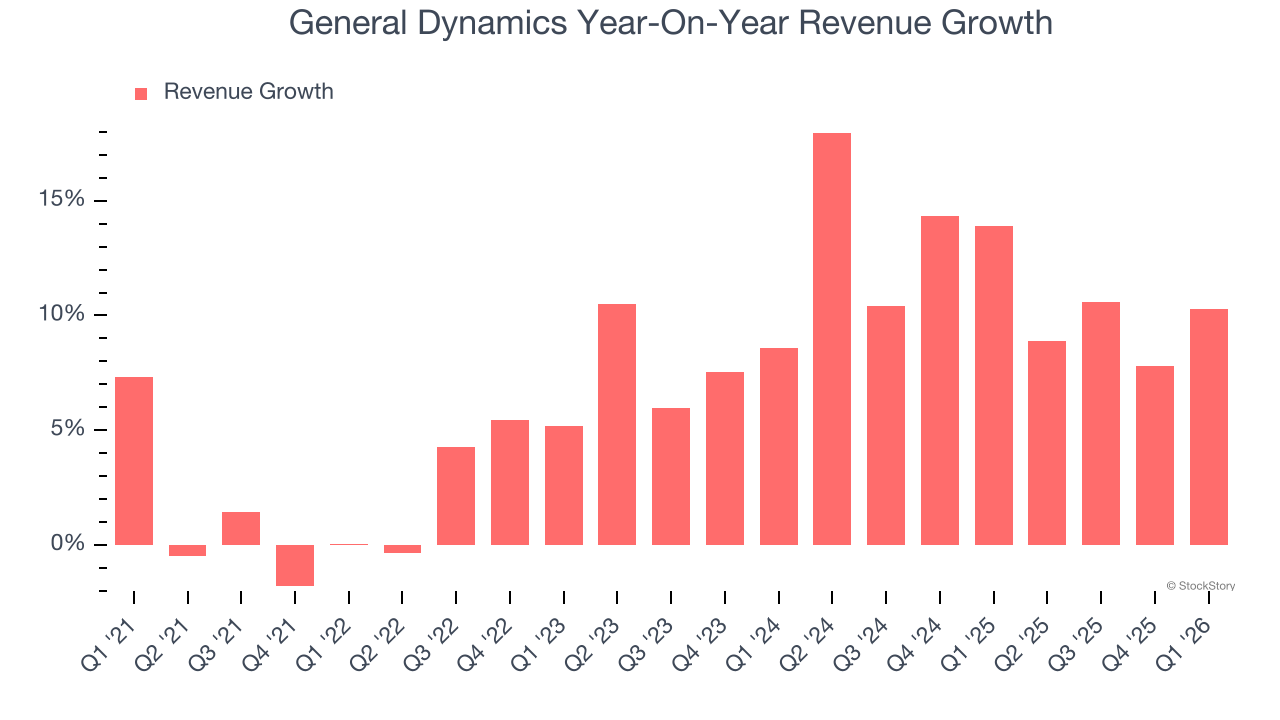

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, General Dynamics grew its sales at a mediocre 6.9% compounded annual growth rate. This was below our standard for the industrials sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. General Dynamics’s annualized revenue growth of 11.7% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

General Dynamics also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. General Dynamics’s backlog reached $130.8 billion in the latest quarter and averaged 20.9% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for General Dynamics’s products and services but raises concerns about capacity constraints.

This quarter, General Dynamics reported year-on-year revenue growth of 10.3%, and its $13.48 billion of revenue exceeded Wall Street’s estimates by 5.9%.

Looking ahead, sell-side analysts expect revenue to grow 3% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

General Dynamics’s operating margin has generally stayed the same over the last 12 months, averaging 10.4% over the last five years. This profitability was solid for an industrials business and shows it’s an efficient company that manages its expenses well.

Looking at the trend in its profitability, General Dynamics’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q1, General Dynamics generated an operating margin profit margin of 10.5%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

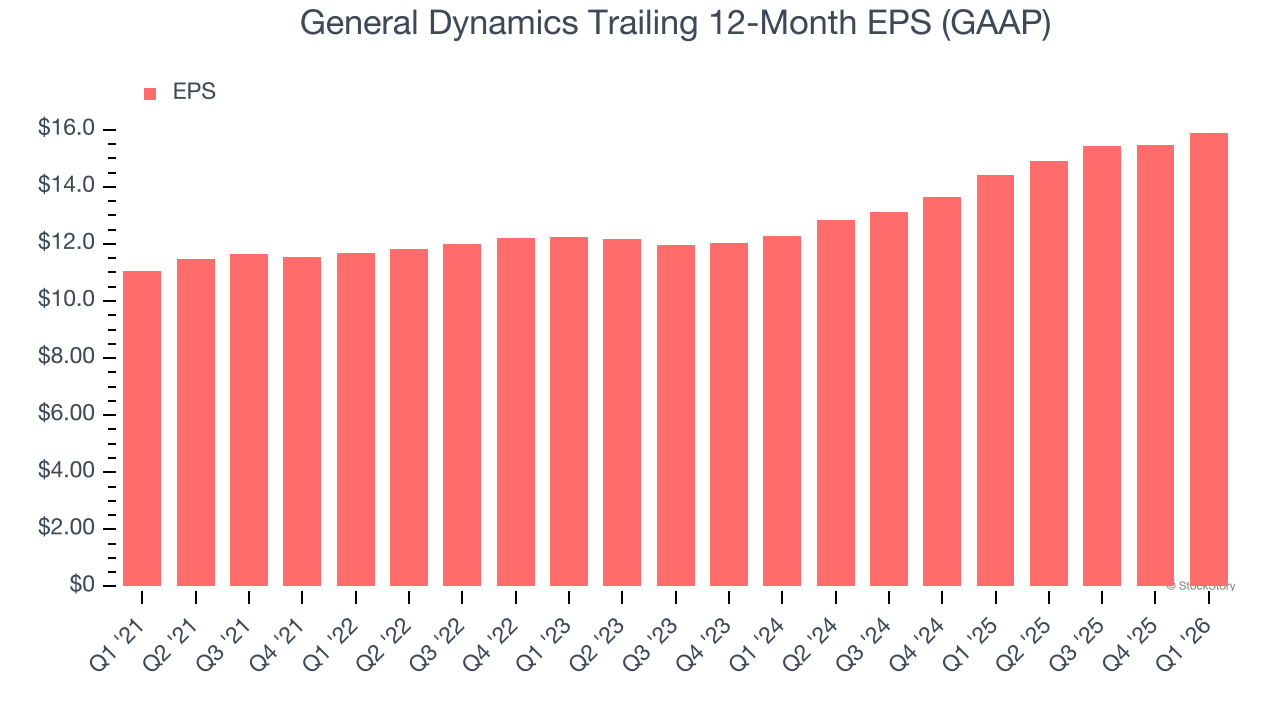

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

General Dynamics’s unimpressive 7.5% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

General Dynamics’s two-year annual EPS growth of 13.8% was great and topped its 11.7% two-year revenue growth.

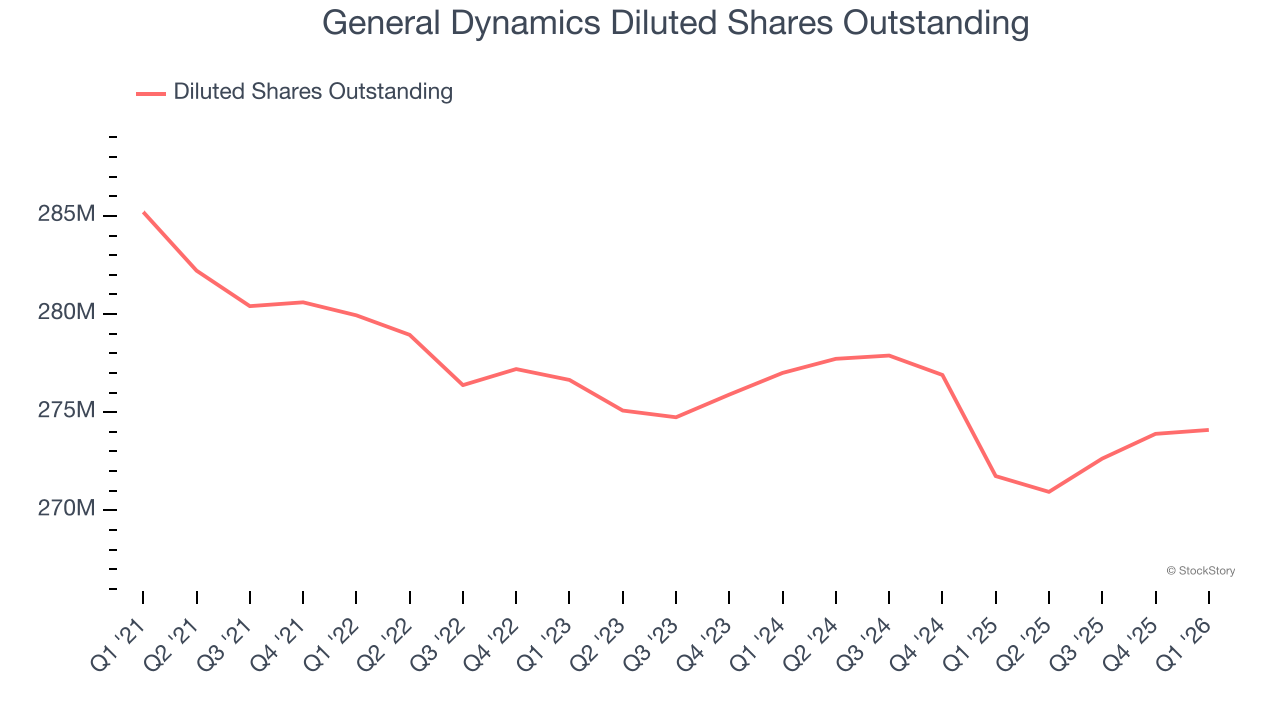

We can take a deeper look into General Dynamics’s earnings quality to better understand the drivers of its performance. A two-year view shows that General Dynamics has repurchased its stock, shrinking its share count by 1%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q1, General Dynamics reported EPS of $4.10, up from $3.66 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects General Dynamics’s full-year EPS of $15.90 to grow 4.9%.

Key Takeaways from General Dynamics’s Q1 Results

We were impressed by how significantly General Dynamics blew past analysts’ adjusted operating income expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 1.3% to $317.91 immediately after reporting.

Indeed, General Dynamics had a rock-solid quarterly earnings result, but is this stock a good investment here? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).