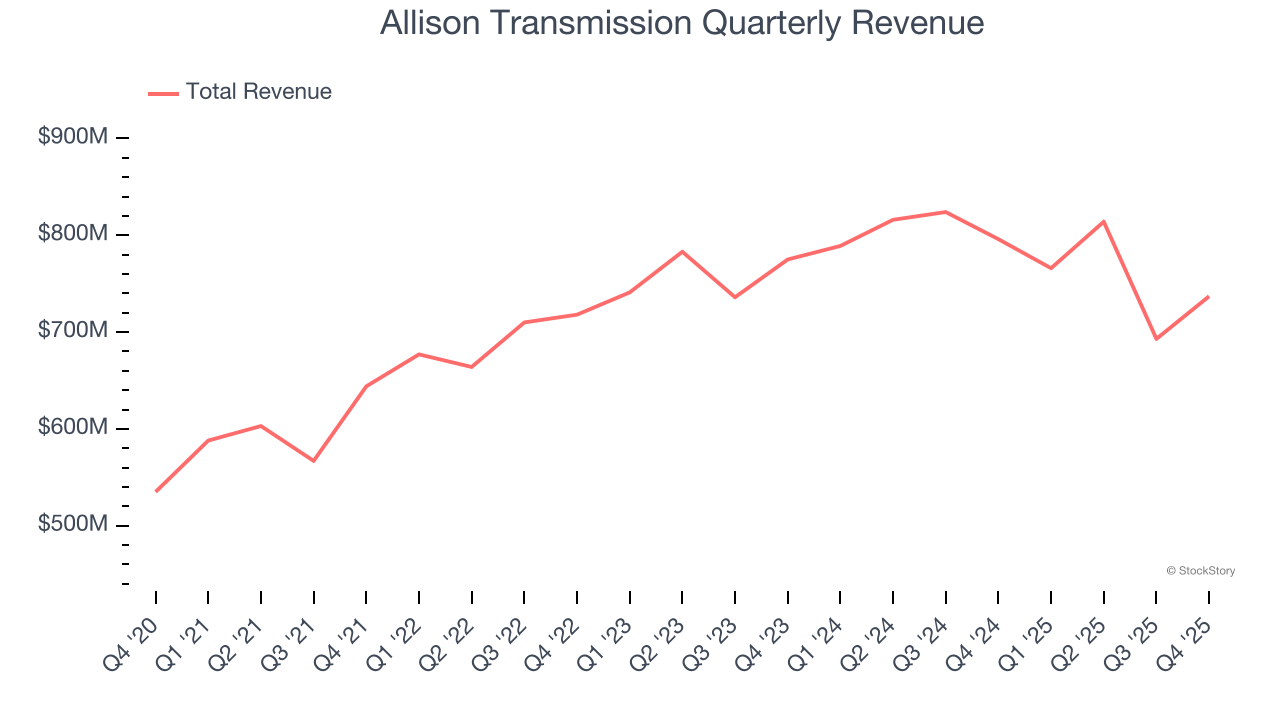

Transmission provider Allison Transmission (NYSE: ALSN) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, but sales fell by 7.4% year on year to $737 million. The company’s full-year revenue guidance of $5.75 billion at the midpoint came in 4% above analysts’ estimates. Its GAAP profit of $1.18 per share was 21.1% below analysts’ consensus estimates.

Is now the time to buy Allison Transmission? Find out by accessing our full research report, it’s free.

Allison Transmission (ALSN) Q4 CY2025 Highlights:

- Revenue: $737 million vs analyst estimates of $726.8 million (7.4% year-on-year decline, 1.4% beat)

- EPS (GAAP): $1.18 vs analyst expectations of $1.50 (21.1% miss)

- Adjusted EBITDA: $265 million vs analyst estimates of $247.2 million (36% margin, 7.2% beat)

- EBITDA guidance for the upcoming financial year 2026 is $1.44 billion at the midpoint, below analyst estimates of $1.53 billion

- Operating Margin: 23.2%, down from 29.5% in the same quarter last year

- Free Cash Flow Margin: 22.9%, up from 17.1% in the same quarter last year

- Market Capitalization: $9.89 billion

David S. Graziosi, Chair, President and Chief Executive Officer of Allison commented, "Although 2025 presented meaningful macroeconomic challenges, we remained disciplined and focused on the factors within our control. With a prioritization of cost management and execution aligned with end markets demand conditions, our full year results demonstrate the resilient earnings power of our business in difficult and uncertain operating environments. For the full year, we achieved an Adjusted EBITDA margin of 37.5 percent and generated Adjusted free cash flow of $661 million."

Company Overview

Helping build race cars at one point, Allison Transmission (NYSE: ALSN) offers transmissions to original equipment manufacturers and fleet operators.

Revenue Growth

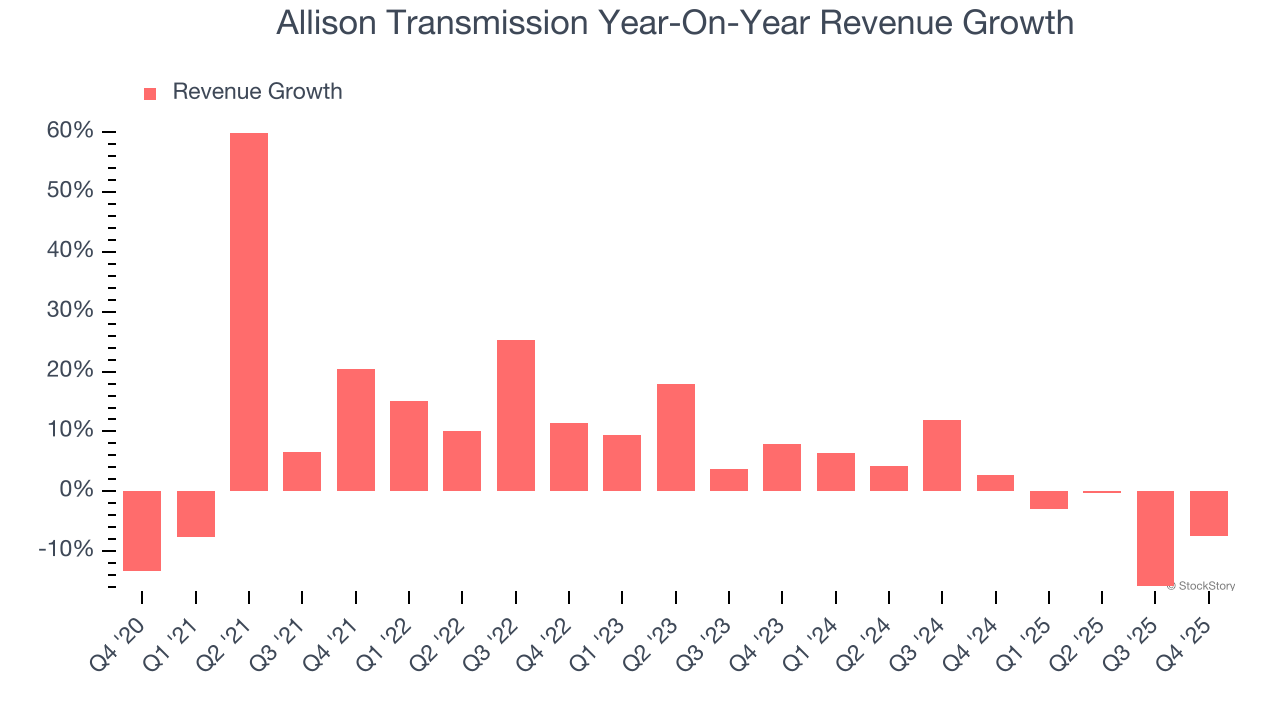

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Allison Transmission grew its sales at a decent 7.7% compounded annual growth rate. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Allison Transmission’s recent performance shows its demand has slowed as its revenue was flat over the last two years. We also note many other Heavy Transportation Equipment businesses have faced declining sales because of cyclical headwinds. While Allison Transmission’s growth wasn’t the best, it did do better than its peers.

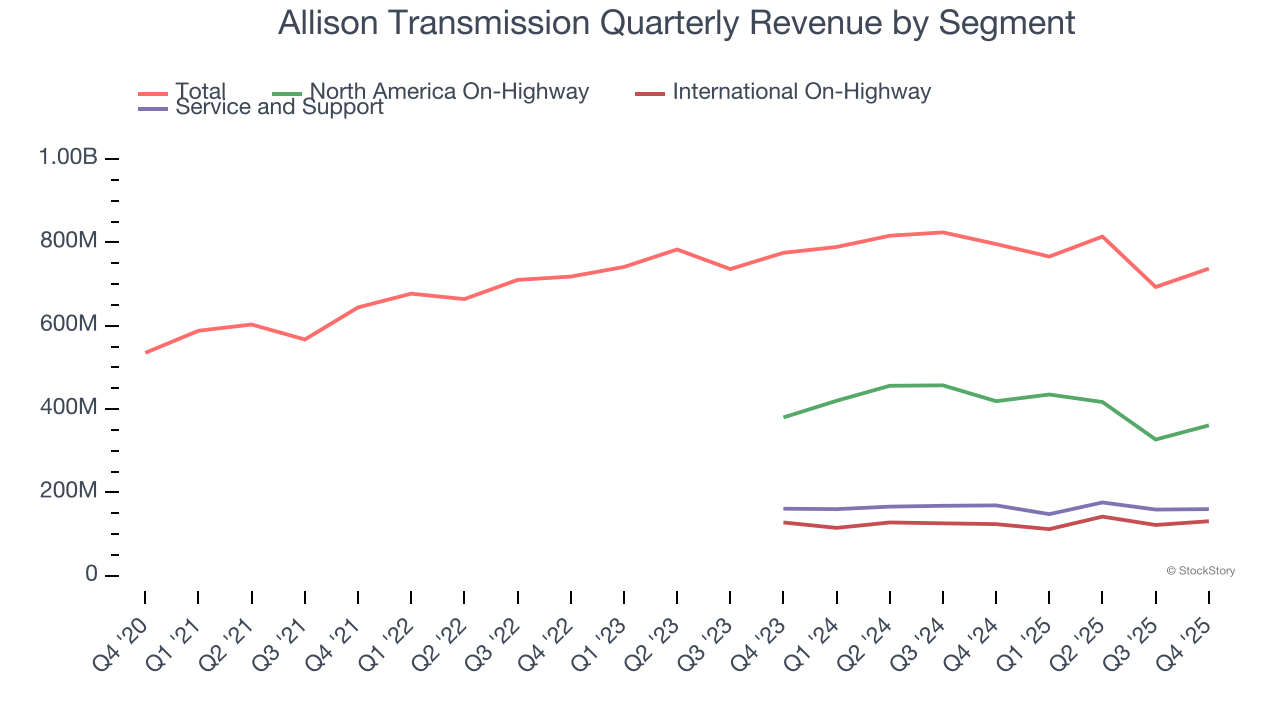

Allison Transmission also breaks out the revenue for its three most important segments: North America On-Highway, International On-Highway, and Service and Support, which are 49%, 17.8%, and 21.7% of revenue. Over the last two years, Allison Transmission’s International On-Highway revenue (propulsion solutions) averaged 1.5% year-on-year growth while its North America On-Highway (propulsion solutions) and Service and Support (parts and equipment) revenues averaged 7.4% and 1.4% declines.

This quarter, Allison Transmission’s revenue fell by 7.4% year on year to $737 million but beat Wall Street’s estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to grow 79.1% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and suggests its newer products and services will fuel better top-line performance.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Operating Margin

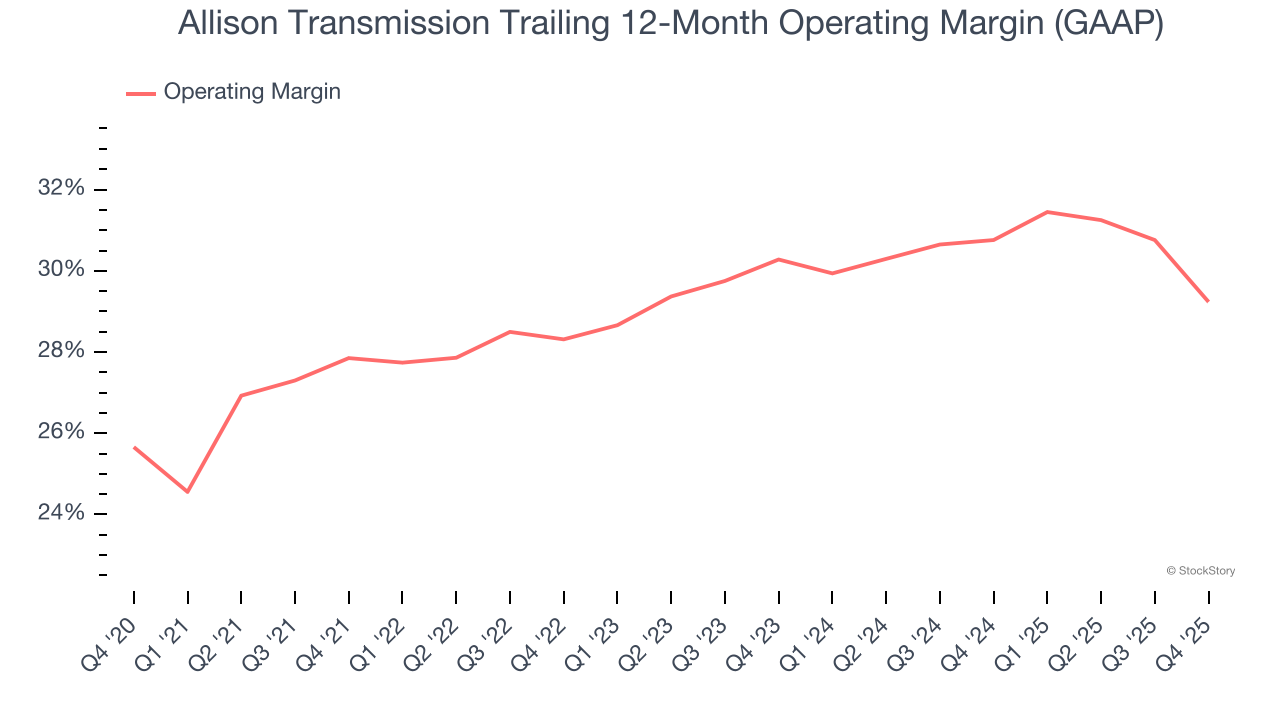

Allison Transmission has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 29.4%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Allison Transmission’s operating margin rose by 1.4 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Allison Transmission generated an operating margin profit margin of 23.2%, down 6.3 percentage points year on year. Conversely, its gross margin actually rose, so we can assume its recent inefficiencies were driven by increased operating expenses like marketing, R&D, and administrative overhead.

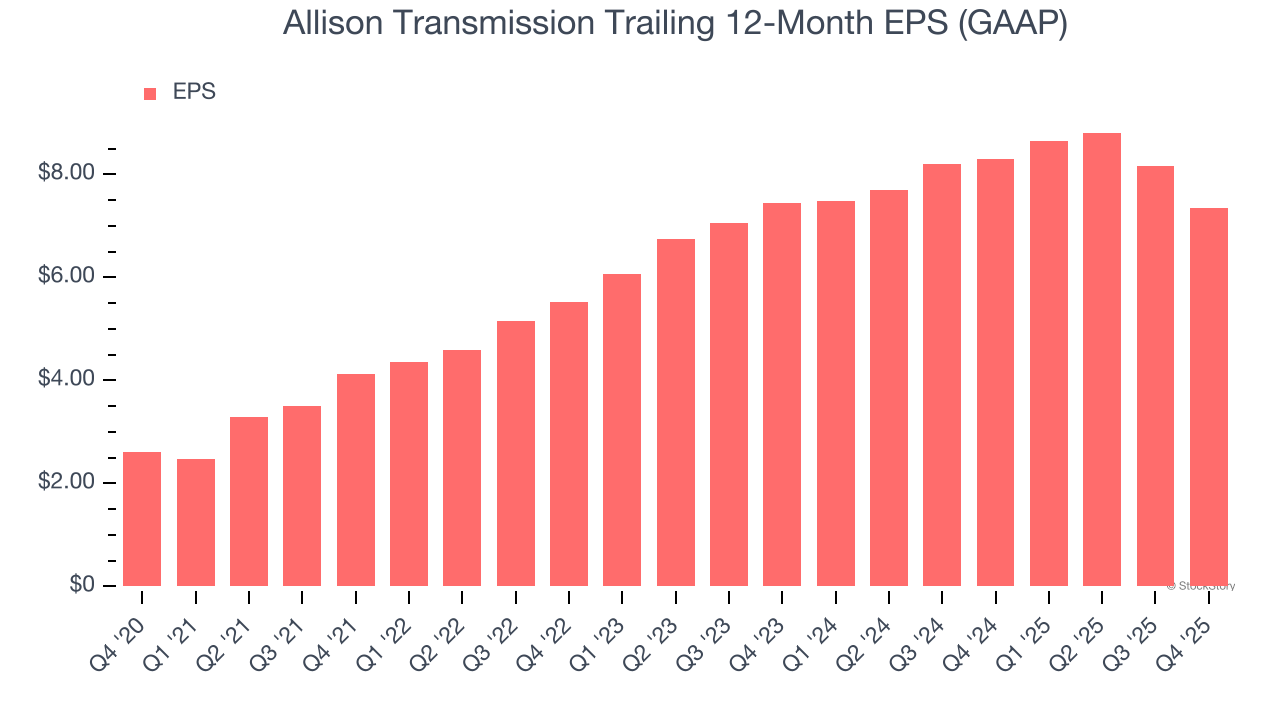

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Allison Transmission’s EPS grew at an astounding 23% compounded annual growth rate over the last five years, higher than its 7.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

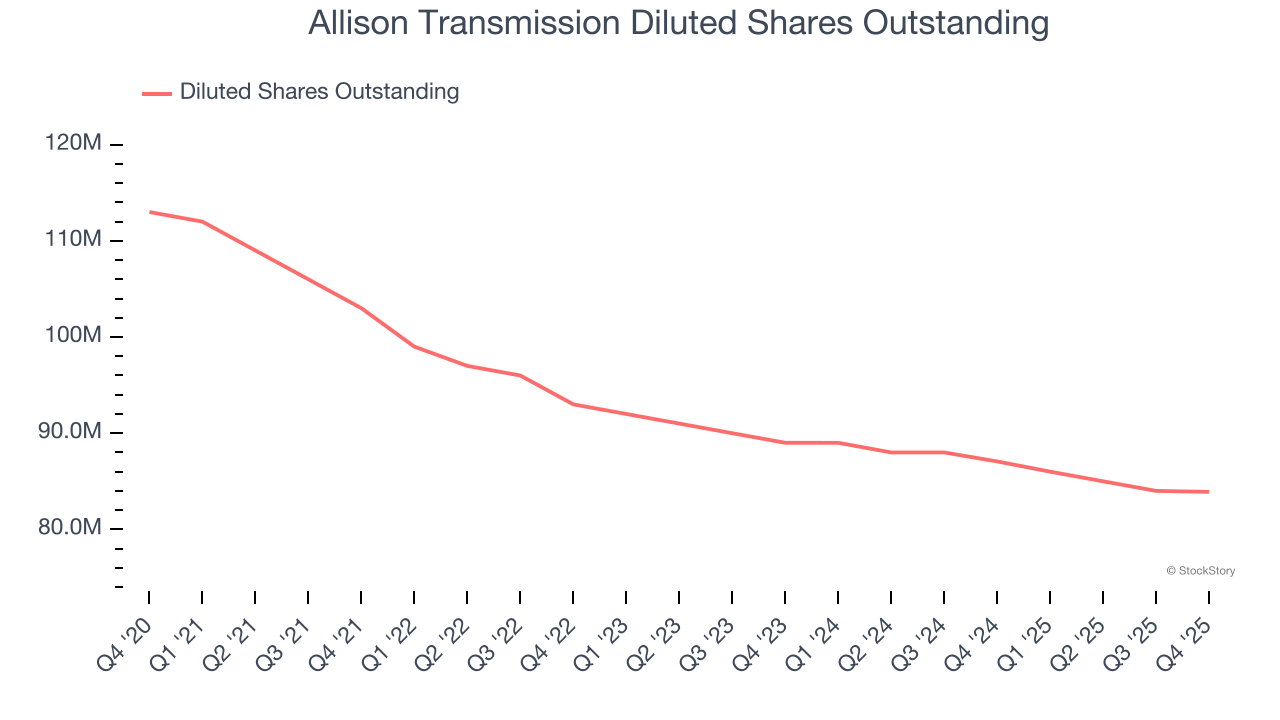

We can take a deeper look into Allison Transmission’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Allison Transmission’s operating margin declined this quarter but expanded by 1.4 percentage points over the last five years. Its share count also shrank by 25.8%, and these factors together are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Allison Transmission, EPS didn’t budge over the last two years, a regression from its five-year trend. Given the merits in other parts of its business, we’re hopeful it can revert to earnings growth in the coming years.

In Q4, Allison Transmission reported EPS of $1.18, down from $2.01 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Allison Transmission’s full-year EPS of $7.34 to grow 31.9%.

Key Takeaways from Allison Transmission’s Q4 Results

We were impressed by Allison Transmission’s optimistic full-year revenue guidance, which blew past analysts’ expectations. We were also glad its EBITDA outperformed Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed and its EPS fell short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock traded up 1.8% to $118.98 immediately following the results.

So do we think Allison Transmission is an attractive buy at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).