What a time it’s been for Bill.com. In the past six months alone, the company’s stock price has increased by a massive 78.2%, reaching $92.51 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy BILL? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

Why Do Investors Watch BILL Stock?

Started by René Lacerte in 2006 after selling his previous payroll and accounting software company PayCycle to Intuit, Bill.com (NYSE: BILL) is a software as a service platform that aims to make payments and billing processes easier for small and medium-sized businesses.

Three Positive Attributes:

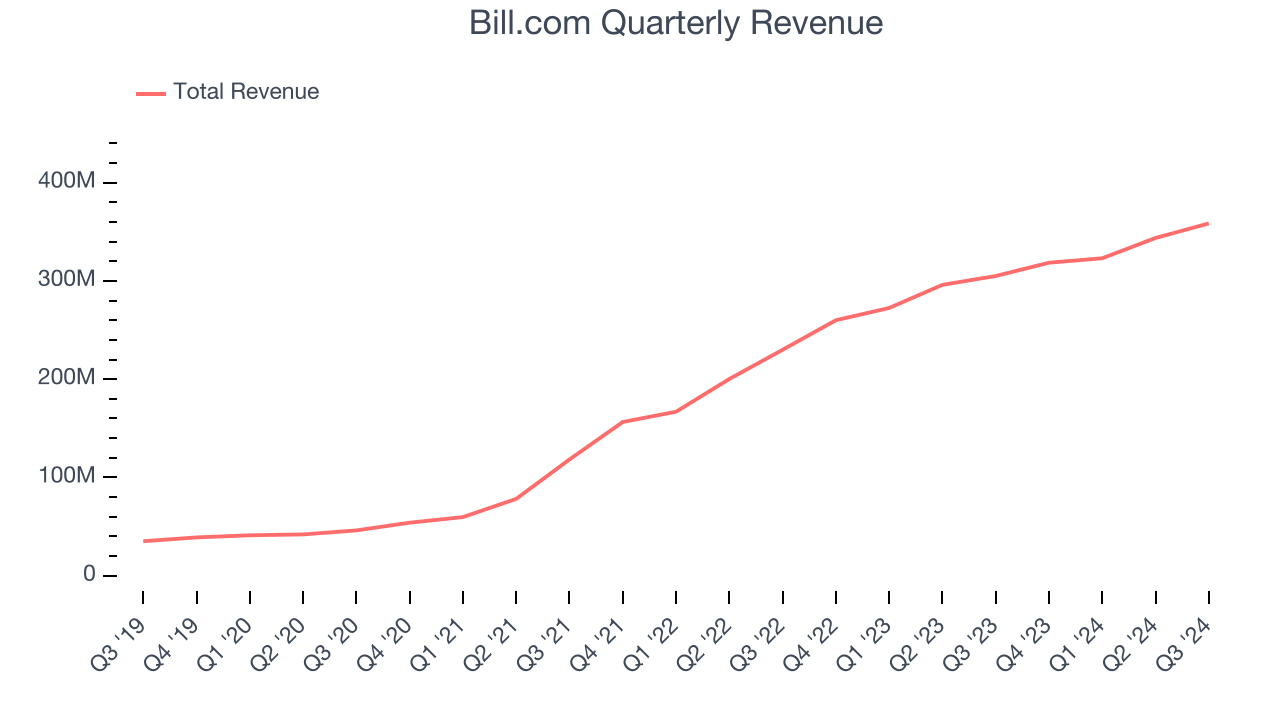

1. Skyrocketing Revenue Shows Strong Momentum

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years. Over the last three years, Bill.com grew its sales at an incredible 63% compounded annual growth rate. Its growth surpassed the average software company and shows its offerings resonate with customers.

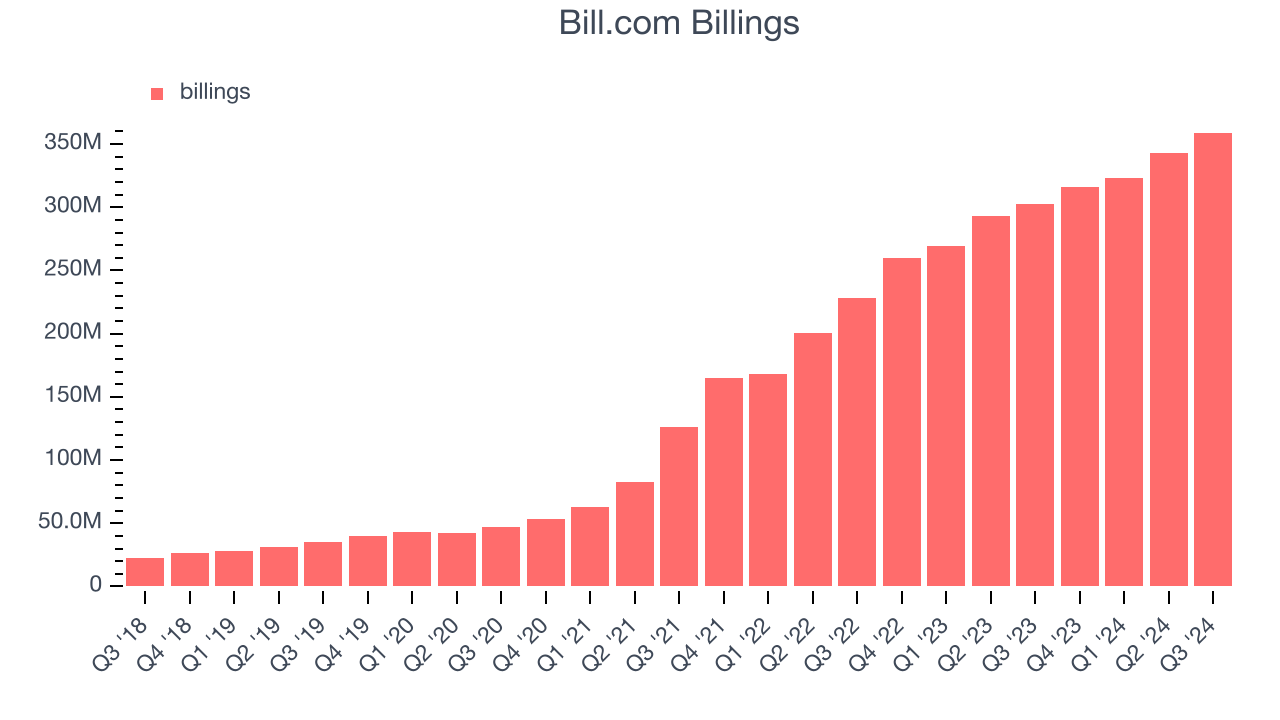

2. Billings Surge, Boosting Cash On Hand

In addition to revenue, billings is a non-GAAP metric that sheds additional light on Bill.com’s business quality. Billings is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Bill.com’s billings punched in at $359.1 million in the latest quarter, and over the last four quarters, its growth averaged 19.3% year-on-year increases. This performance was impressive, indicating robust customer demand. The high level of cash collected from customers also enhances liquidity and provides a solid foundation for future investments and growth.

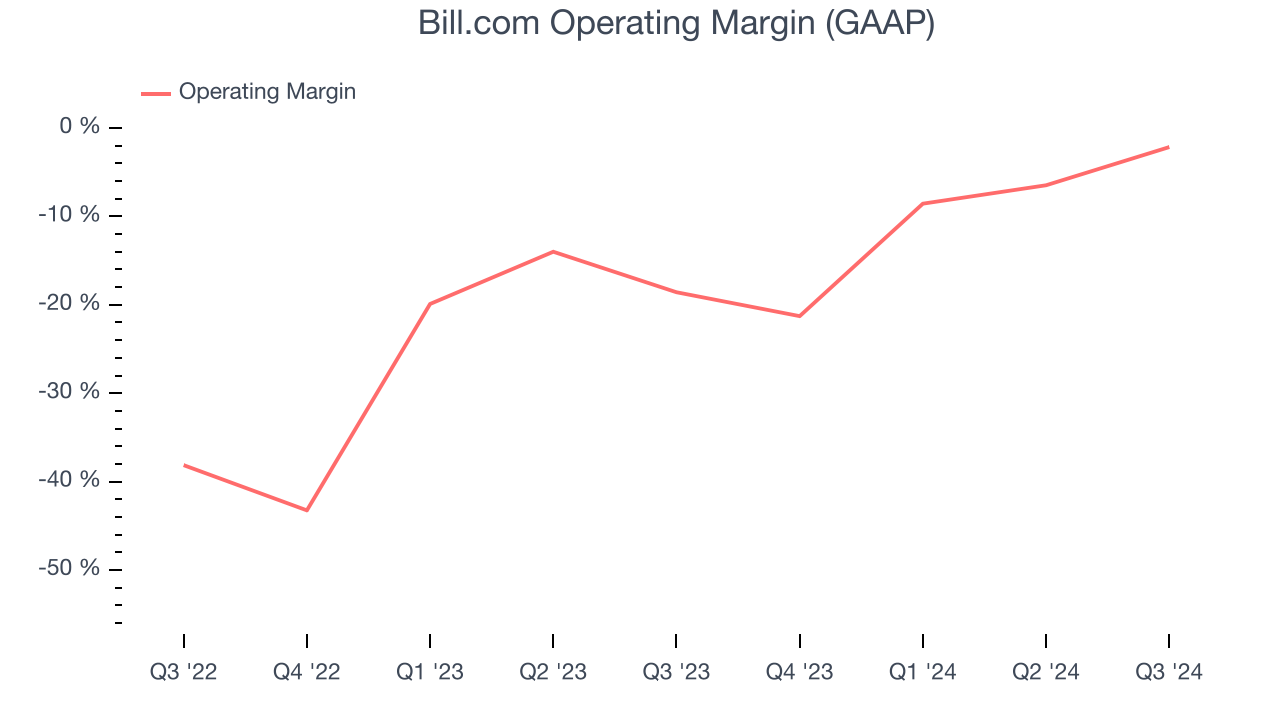

3. Operating Margin Rising, Profits Up

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after developing, marketing, and selling its products. We note that many software businesses adjust for stock-based compensation (SBC) in their reporting, but we prioritize GAAP figures because SBC is a real expense used to attract and retain engineering and sales talent.

Over the last year, Bill.com’s expanding sales gave it operating leverage, and its annual margin rose by 14 percentage points. Its operating margin for the trailing 12 months was negative 9.3%, and it must keep making strides to one day reach sustainable profitability.

Final Judgment

There are definitely things to like about Bill.com, and after the recent rally, the stock trades at 6.7x forward price-to-sales (or $92.51 per share). Is now the time to buy despite the apparent froth? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Bill.com

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.