SanDisk (SNDK) has turned into one of 2026’s most unbelievable artificial intelligence (AI) stories. The stock has exploded roughly 462% year-to-date and nearly 4,000% over the past year as investors poured into AI infrastructure plays. Yet, despite the explosive rally and one of the strongest quarters the company has ever reported, some Wall Street firms, including RBC Capital, Barclays (BCS), JPMorgan (JPM) and Wells Fargo (WFC), haven't upgrade the stock to a “Buy.”

With these four analysts cautious, the question now is can SanDisk sustain this run?

AI Demand Is Completely Reshaping SanDisk’s Business

Valued at $229.1 billion, SanDisk makes NAND flash memory and storage products used in devices like smartphones, PCs, data centers, gaming systems, and AI servers. SanDisk’s third quarter of fiscal 2026 gave bulls plenty of reasons to stay optimistic. The numbers were strong, with revenue rising 251% year over year (YOY) to $5.95 billion. The company credited the increase to pricing changes and a shift toward higher-value customers. Data center revenue surged to $1.47 billion, up 233% sequentially, as AI workloads increasingly require high-performance NAND flash storage.

Adjusted gross margin exploded to 78.4%, far above the company’s own guidance range of 65% to 67%. The most eye-catching number was the jump in adjusted earnings per share (EPS) to $23.41, up 278% sequentially and better than a loss of $0.30 in the prior-year quarter. SanDisk believes that AI models are rapidly evolving from billions of parameters to trillions, and that applications are becoming more complicated as a result of reasoning systems and autonomous AI agents. This trend is increasing the need for low-latency, high-capacity flash storage which the company provides.

CEO David Goeckeler said this demand is a “structural and durable shift,” arguing that AI infrastructure requirements are permanently changing the storage industry. The most probable reason behind SanDisk’s explosive rally is its turn to multiyear supply partnerships. The company has signed five agreements so far with some contracts extending as long as five years. These agreements lock customers into long-term NAND supply commitments while giving SanDisk a more predictable revenue base.

According to management, these agreements now account for more than one-third of the company's planned bit supply in fiscal 2027, with the company still negotiating additional deals. Despite continued heavy investments, the company generated adjusted free cash flow of $2.95 billion, and ended the quarter with $3.7 billion in cash and cash equivalents. Management guided that momentum could continue accelerating, with revenue ranging between $7.75 billion and $8.25 billion in the fourth quarter. The company also projects adjusted gross margin between 79% and 81%, and adjusted EPS between $30 and $33, implying profitability could improve even further.

Why Some Analysts Are Still a “Hold”

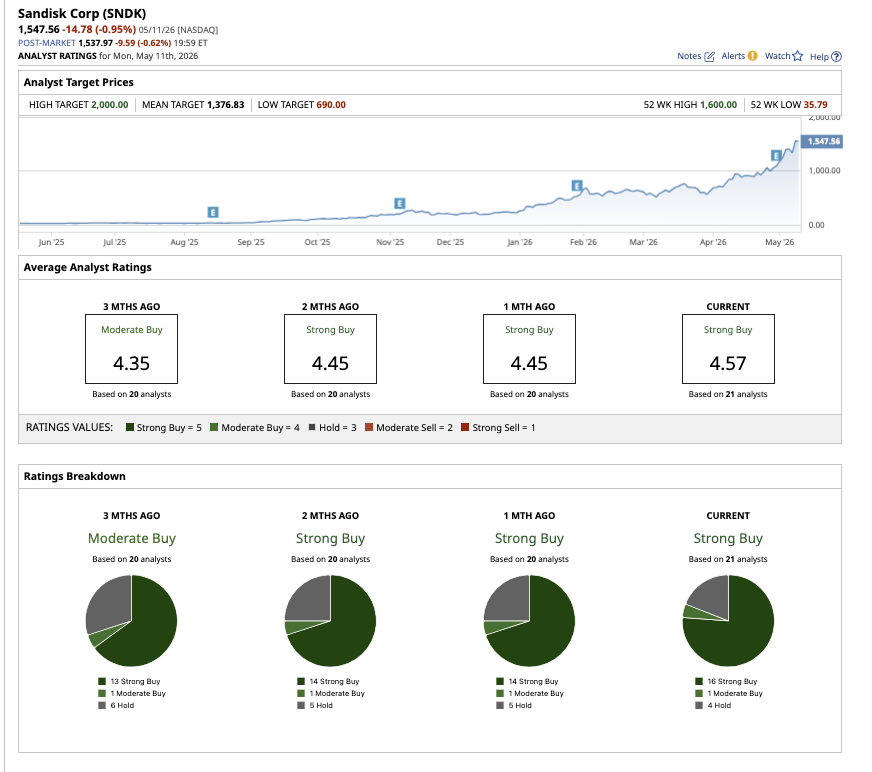

Overall, Wall Street has a consensus “Strong Buy” rating on SanDisk stock, with 16 out of the 21 analysts covering the stock strongly bullish about it. The stock has crossed its mean target price but the Street-high estimate of $2,000 indicates the stock could gain as much as 29% from recent levels. However, despite the numbers, not everyone on Wall Street is convinced the rally can continue.

Analysts at RBC Capital, Barclays, JPMorgan and Wells Fargo increased the price target for the stock but maintained a “Hold” rating. These analysts remain cautious because the memory industry has a long history of boom-and-bust cycles. NAND pricing can soar when supply is limited, but margins can collapse just as quickly if supply exceeds demand. Analysts are also questioning that given the industry’s cyclical history whether SanDisk’s current margins above 78% are truly sustainable over the long term.

Furthermore, investors may now be pricing SanDisk as a company benefiting from a multiyear AI infrastructure supercycle rather than a traditional storage manufacturer. That historical volatility is probably why these analysts haven't upgraded the stock to a “Buy.” However, SanDisk stock looks reasonably valued after its explosive run. The stock is trading at 9x forward 2027 earnings which are expected to increase by 162.3%.

Is SanDisk Still A Buy?

SanDisk’s historic run and the memory industry’s unpredictable history may explain why Wall Street remains sharply divided. After a 462% YTD surge and an almost 4,000% gain over the past year, expectations are now extremely high. The biggest risk for investors now is whether SanDisk can continue outperforming the extraordinary expectations already built into the stock price.

For long-term, aggressive investors who believe AI infrastructure demand is only getting started, SanDisk may still look attractive despite the huge rally.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- SNDK Stock Alert: SanDisk Falls Amid Broader Chip Pullback

- Ahead of Cisco Earnings, Here Is What Barchart Options Data Shows for CSCO Stock

- Nelson Peltz Reportedly Wants to Take Wendy's Private. What That Means for WEN Stock.

- Plug Power Stock Pops on Earnings. The Hydrogen Company Improved Its Margins 71%.