Valued at a market cap of $28.9 billion, GE HealthCare Technologies Inc. (GEHC) is a Chicago, Illinois-based company that develops, manufactures, and markets products, services, and complementary digital solutions used in the diagnosis, treatment, and monitoring of patients.

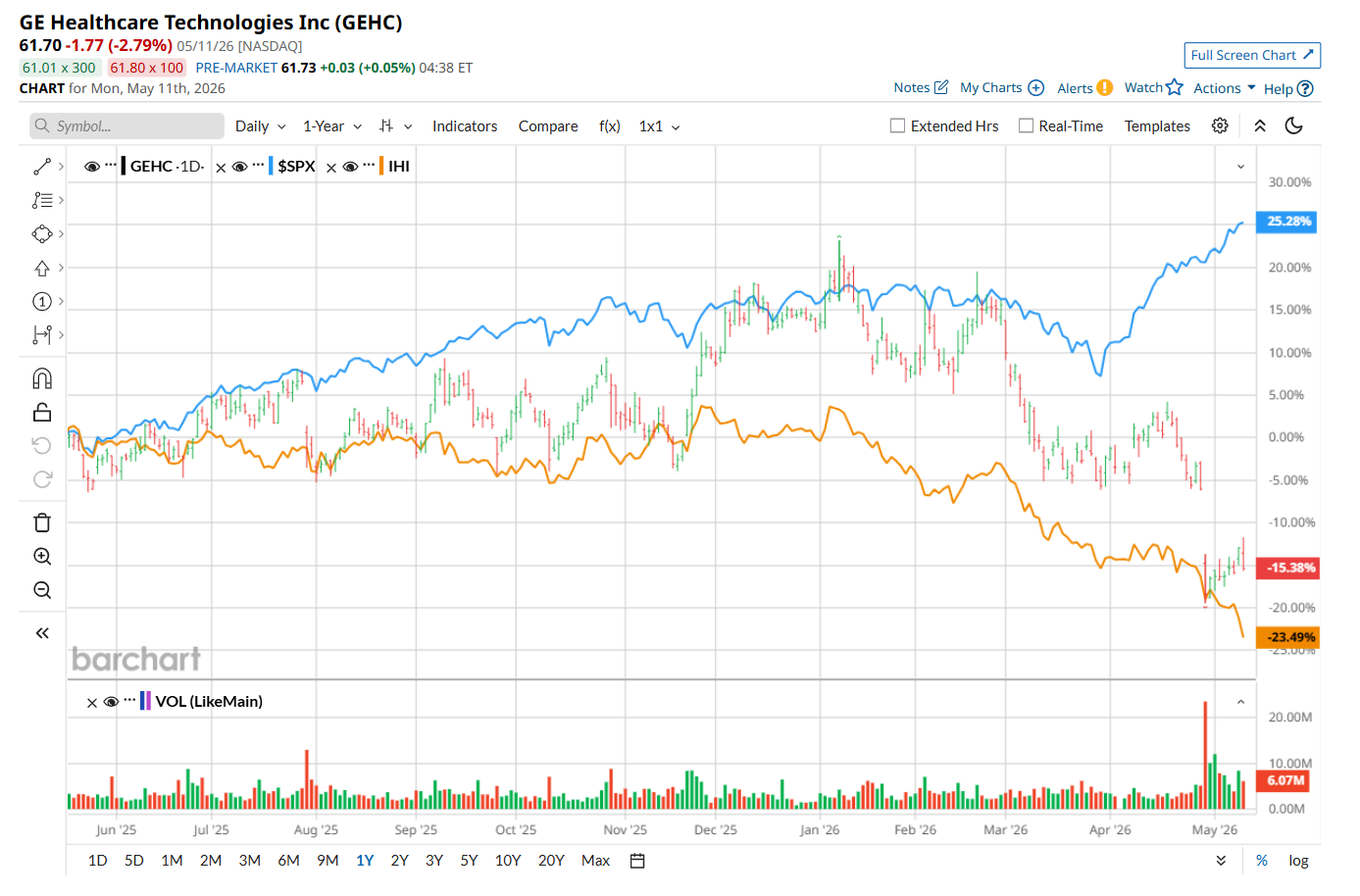

This healthcare company has notably underperformed the broader market over the past 52 weeks. Shares of GEHC have declined 11.7% over this time frame, while the broader S&P 500 Index ($SPX) has soared 31%. Moreover, on a YTD basis, the stock is down 24.8%, compared to SPX’s 8.3% rise.

Nonetheless, narrowing the focus, GEHC has outpaced the iShares U.S. Medical Devices ETF’s (IHI) 21.7% drop over the past 52 weeks. However, it has lagged IHI’s 23.5% YTD loss.

On Apr. 29, shares of GEHC plunged 13.2% after its mixed Q1 earnings release. The company reported revenue of $5.1 billion, up 7.4% year-over-year and 1.6% above consensus estimates, driven by strong commercial execution across Pharmaceutical Diagnostics, including Flyrcado, Advanced Visualization Solutions, and Imaging. However, first-quarter profitability was pressured by a supplier issue in the PDx segment, which management noted has since been resolved.

The company also highlighted significant increases in memory chips, oil, and freight costs during the quarter, which it expects will continue to weigh on results through the remainder of 2026. In response to these inflationary pressures, GEHC lowered its profit outlook, weighing on investor sentiment. Meanwhile, its adjusted EPS declined 2% year-over-year and missed analyst expectations by 7.5%.

For the current fiscal year, ending in December, analysts expect GEHC’s EPS to grow 6.5% year over year to $4.89. The company's earnings surprise history is mixed. It topped the consensus estimates in three of the last four quarters, while missing on another occasion.

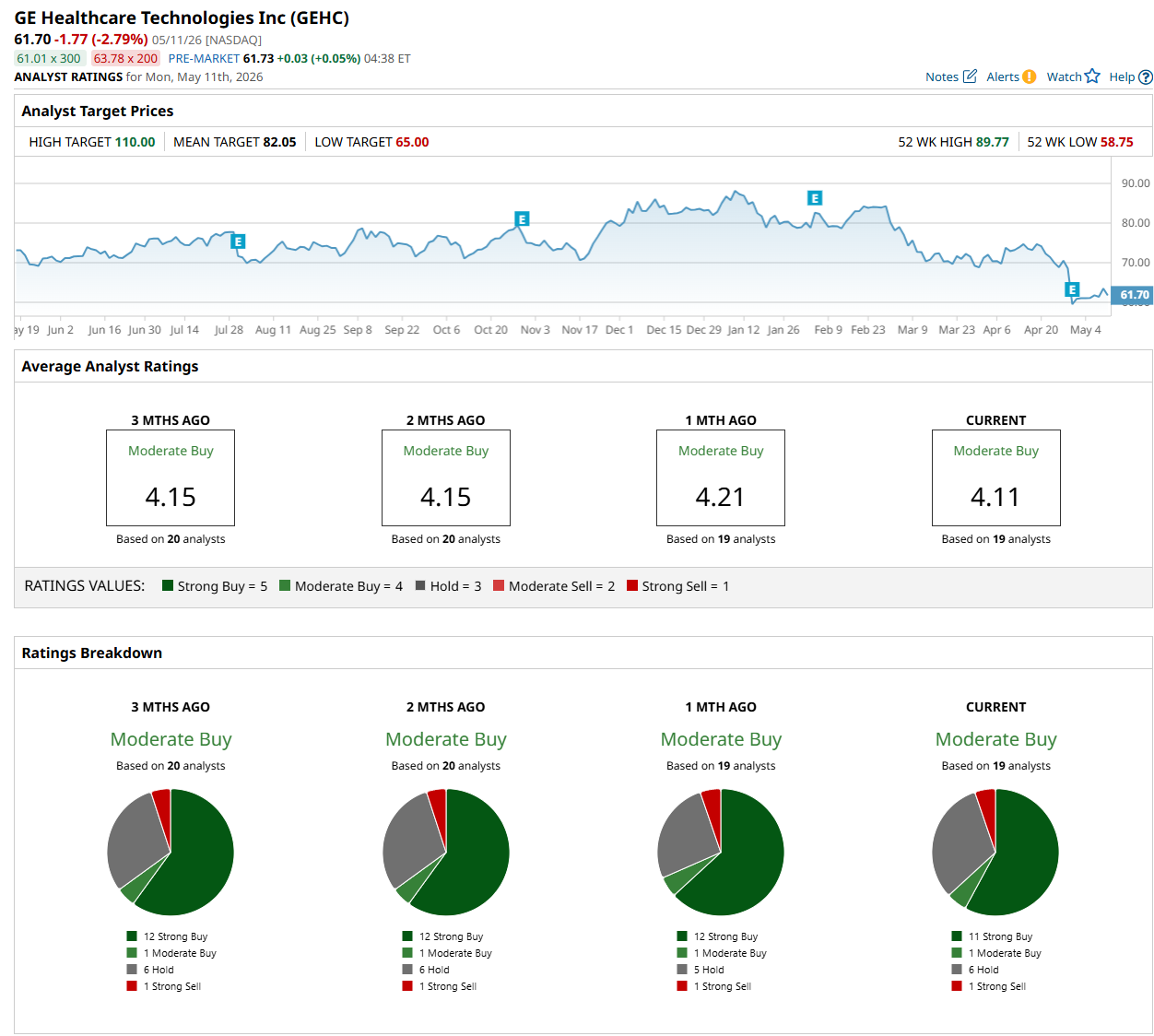

Among the 19 analysts covering the stock, the consensus rating is a "Moderate Buy,” which is based on 11 “Strong Buy,” one "Moderate Buy,” six “Hold,” and one "Strong Sell” rating.

The configuration is less bullish than a month ago, with 12 analysts suggesting a “Strong Buy” rating.

On Apr. 30, Oppenheimer analyst Suraj Kalia maintained an “Outperform” rating on GEHC but lowered its price target to $85, indicating a 37.8% potential upside from the current levels.

The mean price target of $82.05 suggests a 33% premium to its current price levels, while its Street-high price target of $110 implies a 78.3% potential upside.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart