SoFi Technologies just got a harsh reality check from Wall Street. The stock sank more than 15% on April 29, even though the company turned in a strong first-quarter report with record adjusted net revenue of $1.1 billion, up 41% from a year ago, and net income of $167 million, more than double last year.

The selloff came down to one particular point. SoFi’s management stuck with its full-year 2026 guidance instead of raising it, and investors were clearly expecting more. That choice flipped the switch from excitement to doubt and sparked the sharp move lower.

This feels bigger than a single earnings reaction. The market looks like it is re-pricing what it is willing to pay for SoFi as the business shifts from a hyper-growth story to a more steady, bank-like operator. Is SoFi’s latest slump a sign that the fintech dream is finally cracking or the moment when a maturing, still-growing franchise quietly becomes too cheap to ignore?

SoFi’s Numbers Look Strong

SoFi Technologies (SOFI) runs a fully digital financial platform that offers lending, deposits, investing, and payments services to consumers and enterprise partners across the United States. Based in San Francisco, shares are down 39% year-to-date (YTD) but 27.6% higher over the past 12 months.

The business is worth $19.8 billion and trades at a trailing price-to-earnings of 48.32 times, compared with a sector median of 12.45 times, and a trailing price-to-sales ratio of 4.98 times versus about 3.09 times for peers. Those numbers show investors had been paying up for future growth.

The latest numbers help explain why that premium is now under debate. SoFi reported GAAP net revenue of $1.1 billion, up 43% from $771.8 million, with adjusted net revenue also at $1.1 billion after rising 41% from $770.7 million. That performance produced earnings per share of $0.12 for the quarter ending March 2026.

Their net interest income came in at $693.0 million, up 39%, driven by a 41% increase in average interest-earning assets and a 48-basis-point drop in funding costs, even though average asset yields fell by 63 basis points. This improvement in the spread pushed net interest margin to 5.94%, a 22-basis-point increase from the prior quarter and a level many traditional banks would be happy with.

The Financial Services segment also pulled its weight. SoFi generated $428.5 million in segment net revenue, up 41%, and non-interest income climbed 55% to $200.8 million as deposits grew and users engaged with more products.

Their Loan Platform Business added $140.8 million in adjusted net revenue, with $138.3 million tied to $3.0 billion of personal loans either originated for or referred to third parties. A 54% jump in interchange revenue, backed by nearly $25 billion in annualized spending across SoFi Money and credit cards, helped lift contribution profit to $195.6 million, even though contribution margin dipped 3 points to 46% as the company kept investing for growth.

SoFi’s Real-World Moves

SoFi’s recent moves show a company quietly building out its backbone. It is now one of the first institutions to let members both send and receive instant payments through the FedNow Service, using its Galileo platform to move money in seconds between SoFi accounts and other U.S. banks at any time, including nights and weekends. That feature pushes SoFi deeper into real-time payment rails that many traditional banks are still slow to adopt.

The business has been just as busy on the capital-light lending side. SoFi recently expanded its Loan Platform Business with new agreements that together commit more than $3.6 billion in personal loan volume across three institutional partners, including a major global bank, a top-five global asset manager, and a financial services and insurance group. This unit pre-qualifies borrowers and either originates or refers loans to those partners, matching consumer demand with outside capital.

The build-out of business banking adds another layer to the story. SoFi has rolled out a “big business banking” platform built to handle both fiat and crypto on a single regulated stack, giving companies one place to hold funds, move money, and settle transactions around the clock in traditional currencies and digital assets.

Insider behavior sends its own message. Chief Executive Officer Anthony Noto recently bought 28,900 shares at an average price of $17.32, a roughly $500,548 purchase that lifted his direct holdings to 11,704,352 shares, about a 0.25% increase.

Taken together, these moves tell a story that feels much more like a growing, infrastructure-heavy franchise.

What the Street Is Really Pricing In

Wall Street may be rethinking the fintech story, but it still expects SoFi’s earnings to keep growing. For the quarter ending June 2026, the average earnings per share (EPS) estimate is $0.13, up from $0.08 a year earlier, which works out to a solid 62.50% jump in profit.

SoFi’s own outlook is also far from weak. For the second quarter of 2026, management is calling for about 30% adjusted net revenue growth, an adjusted EBITDA margin around 30%, and an adjusted net income margin in the 12% - 13% range.

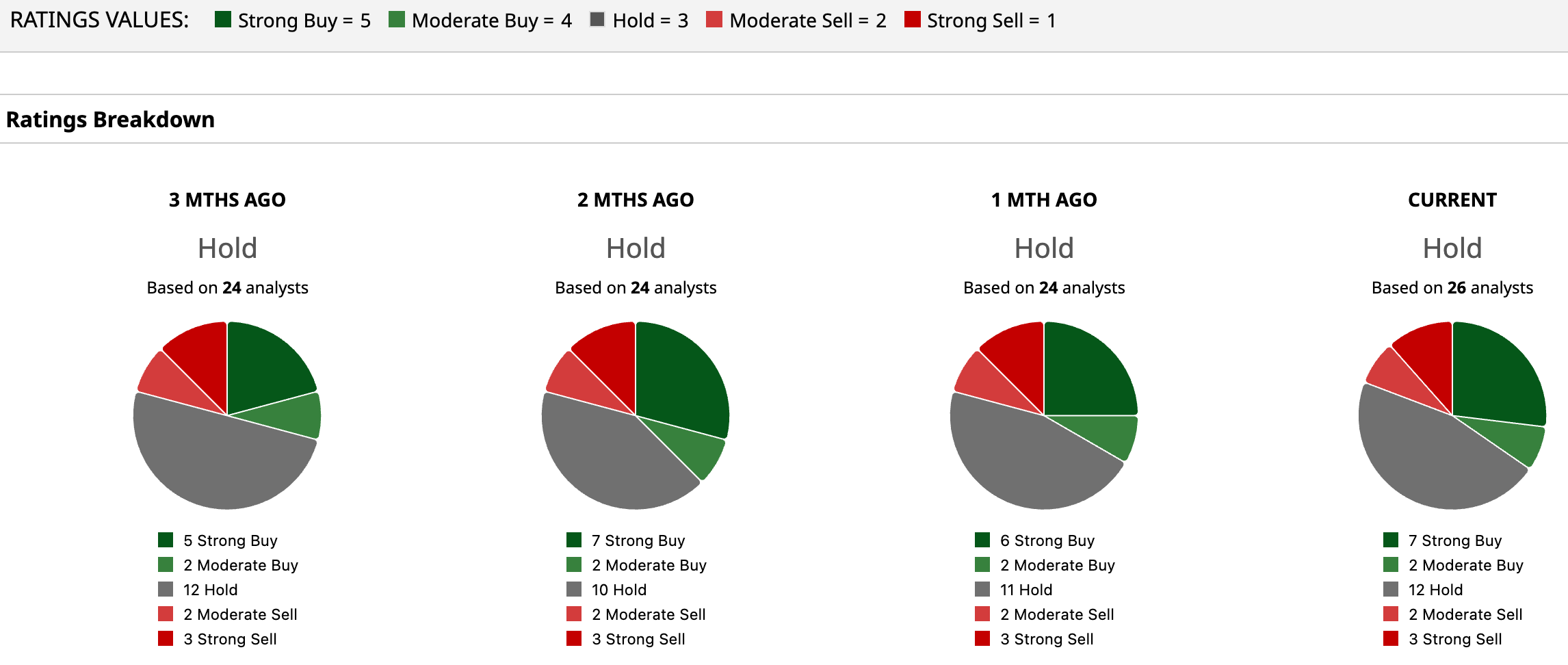

The way analysts are responding lines up with that middle-ground story. The consensus from 26 analysts is a “Hold.” Their average price target of $24.02, points to a 49% potential upside if SoFi simply delivers on the growth it has already laid out.

Conclusion

SoFi’s selloff looks less like a broken business and more like the market cooling off on how much it wants to pay for its growth story. The numbers and guidance still point to steady progress, which makes a slow move higher with choppy reactions around earnings more likely than a total breakdown or a sudden moonshot. In the long run, the stock is likely to track the actual results more than the short‑term mood swings.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- A $20 Billion Reason to Buy Dividend-Paying Visa Stock Now

- SanDisk Stock Just Hit New Record Highs With Wall Street

- GLP-1 Sales Continue to Lift Eli Lilly. Does That Make LLY Stock a Buy?

- Western Digital Stock Has More Than Doubled YTD, but Bank of America Still Thinks You Should Buy Ahead of Earnings