Gold (GCM26) has been on a relentless climb over the past year, capturing investor attention as a trusted hedge against inflation, geopolitical strain, and currency volatility. With prices pushing past the $4,500-per-ounce mark in recent months, miners have quietly enjoyed a surge in profitability, translating elevated spot prices into stronger realized margins. The early months of 2026, in turn, have reflected that strength, with the sector delivering results that stand out in an otherwise uncertain market backdrop.

And now Barrick Mining Corporation (B) seems ready to seize that moment with a calculated move. The company is preparing to take its North American gold business public, carving out a new entity called North American Barrick and is set for listings in New York and Toronto. At the heart of this spin-off lies a portfolio that already delivers scale and stability, anchored by Nevada Gold Mines (a joint venture between Barrick Mining and Newmont (NEM), Pueblo Viejo, and the promising Fourmile discovery, which management believes could rank among the most significant finds of this century.

This is a strategic reset. By placing seasoned leadership at the helm while retaining control, Barrick Mining aims to unlock value without relinquishing its crown jewels. Yet, as discussions continue with partner Newmont Corporation and market conditions remain fluid, does this move signal a golden opportunity for investors, or a moment to tread carefully?

About Barrick Mining Stock

Barrick Mining Corporation has grown into one of the world’s leading mining players, building its footprint across some of the richest mineral regions globally. Founded in 1983 and based in Toronto, the company operates across multiple continents with a focus on high-quality, long-life assets.

While gold remains its core strength, Barrick Mining has steadily expanded into copper, aligning with evolving global demand. Its strategy revolves around disciplined growth, operational efficiency, and strong partnerships. Over time, Barrick has positioned itself not just as a producer, but as a company focused on sustaining value through cycles in an ever-changing commodities landscape. Its market cap currently stands at $64.4 billion.

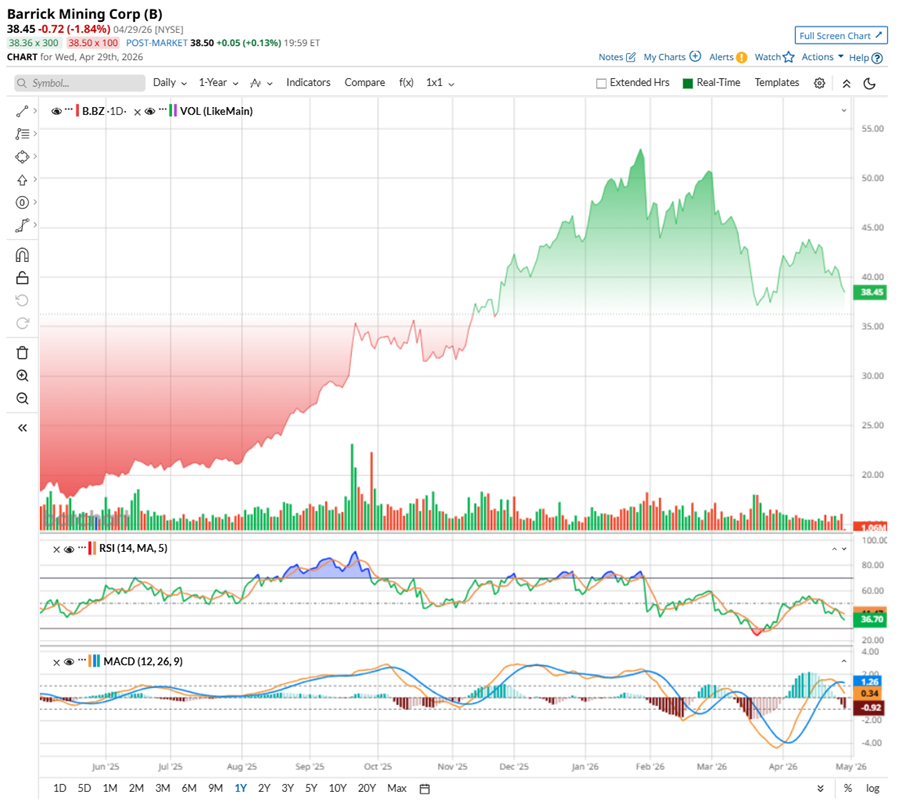

The past year has been quite a ride for the shares of Barrick Mining, one that tells two very different stories depending on where we look. Stretch it out over 52 weeks, and the picture looks impressive. The stock has surged 105.28%, riding the wave of rising gold prices and stronger profitability across the sector. Even in the last six months, it managed to hold on to an 18.22% gain, reflecting that underlying momentum.

But zooming into 2026, the stock has slipped into the red, down 10.25% on a year-to-date (YTD) basis, and more strikingly, 28.3% below its January peak of $54.69. That pullback has not come out of nowhere. It mirrors the recent volatility in gold prices themselves, because for Barrick Mining, the connection is direct. When yellow metal cools, so do its earnings and cash flows expectations, and the stock tends to follow.

Technically, the signals are not offering much comfort right now. Trading volumes have leaned bearish, with more selling pressure showing up in recent sessions. The 14-day RSI, though off its earlier oversold levels, is still sitting at 40 and drifting lower, hinting that momentum remains weak. Add to that a bearish MACD crossover, with the histogram turning negative, and the chart suggests that the stock is still searching for stability rather than gearing up for a quick rebound.

From a valuation standpoint, B is not stretched. The stock is priced at about 11.04 times forward adjusted earnings, cheaper than the sector median and its own historical average.

What really keeps investors around, though, is the dividends story. Barrick Mining has paid dividends for 30 consecutive years and most recently paid a $0.42 per-share quarterly payout in March. That adds up to $1.68 annually, or a hefty 4.3% annualized yield, far outpacing the SPDR S&P 500 ETF’s (SPY) 1.04% yield.

A Snapshot of Barrick Mining's Q4 Report

Barrick Mining rolled out its Q4 and full-year 2025 results in February, and the numbers felt a bit counterintuitive at first glance, but compelling once we followed the thread. Gold production came in at 871,000 ounces for the quarter, down nearly 19% year-over-year (YOY). Yet, thanks to a sharp rise in gold prices, the company turned that lower output into a much stronger financial showing.

Revenue surged to $6 billion, marking a 64.5% jump from a year ago, while adjusted earnings landed at $1.04 per share, comfortably ahead of Wall Street’s expectations. The real driver was Gold prices. Barrick Mining realized an average of $4,177 per ounce during the quarter, up over 57%, effectively doing the heavy lifting where volumes softened.

Operationally, there were bright spots. Nevada Gold Mines held steady, with Carlin posting a 25% production jump from the previous quarter. Pueblo Viejo, meanwhile, pushed throughput to record levels, helping offset some recovery challenges elsewhere. Copper quietly added support too, with production rising 13% sequentially to 62,000 tons.

What stood out just as much was the balance sheet. Cash climbed to roughly $6.7 billion, up 65% YOY, while debt edged slightly lower to $4.7 billion. Strong operating cash flow of $2.73 billion translated into $1.62 billion in free cash flow, giving Barrick Mining room to maneuver. Asset sales, including Hemlo and Tongon, brought in $2.6 billion over the year, further strengthening liquidity.

Looking ahead, Barrick Mining is guiding for 2.9 to 3.25 million ounces of gold production in 2026, alongside a new dividend policy targeting 50% of free cash flow - a signal that the company intends to keep shareholders firmly in the picture as the cycle unfolds.

Barrick Mining is set to release its results for fiscal Q1 2026 on Monday, May 11, before the market opens.

Analysts project EPS for the quarter to rise 111.4% YOY to $0.74. Looking ahead to fiscal 2026, the bottom line is expected to surge 46.7% annually to $3.55 per share and then grow by another 18.3% annually to $4.20 per share in fiscal 2027.

What Do Analysts Expect for Barrick Mining Stock?

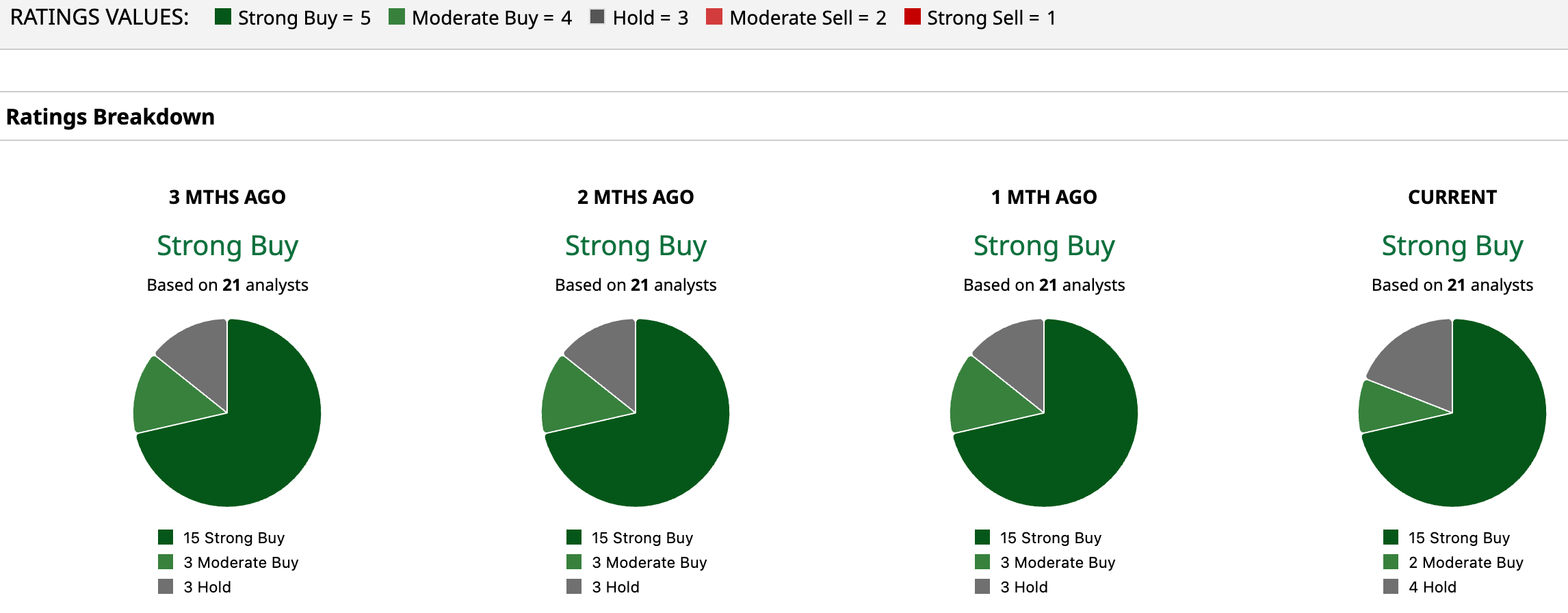

Analysts covering B stock are optimistic about the mining stock, with an overall “Strong Buy” rating. Of the 21 analysts, 15 are upbeat, giving a “Strong Buy” rating, two suggest a “Moderate Buy,” and the remaining four analysts are playing it safe with a “Hold.”

B’s average Street target of $56.53 indicates the stock has an upside potential of 44.58% from the current levels. Still, the most bullish target of $69.35 leaves room for about 77.37% more upside from here.

Conclusion

The planned IPO of Barrick Mining’s North American business – potentially valuing those assets above $60 billion – is not just about raising cash. It is about giving its best mines a cleaner stage. By separating Nevada Gold Mines, Pueblo Viejo, and the Fourmile project into a standalone entity, the company is effectively grouping its more stable, lower-risk assets in one place, while leaving operations in regions like Mali and Pakistan within the parent, where complexity and risk tend to be higher.

Of course, the path is not entirely smooth. Ongoing discussions with Newmont Corporation, past operational friction, and a softer stock performance suggest investors are still watching execution closely. But there is a solid cushion underneath.

Strong cash flows, a growing cash pile, and a disciplined dividend policy make it clear that shareholder returns remain central to Barrick Mining Corporation’s strategy.

Backed by what appears to be one of its strongest balance sheets in years, the planned spin-off of its North American gold assets could help unlock a clearer, more transparent valuation if timelines hold. Even so, while any pullback in the stock market may start to look like a long-term opportunity, the ride from here could still come with its fair share of volatility.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- A $20 Billion Reason to Buy Dividend-Paying Visa Stock Now

- SanDisk Stock Just Hit New Record Highs With Wall Street

- GLP-1 Sales Continue to Lift Eli Lilly. Does That Make LLY Stock a Buy?

- Western Digital Stock Has More Than Doubled YTD, but Bank of America Still Thinks You Should Buy Ahead of Earnings