The telecom space is going through a big shift, with 5G, Open RAN, and AI data center demand all pushing network spending higher. Global 5G connections hit 2.8 billion in Q3 2025, with 162 million added in that quarter alone, while the Open RAN market is now worth about $6.5 billion. At the same time, copper wiring is hitting its physical limits inside AI data centers, which is making optical networking more important as data traffic keeps rising.

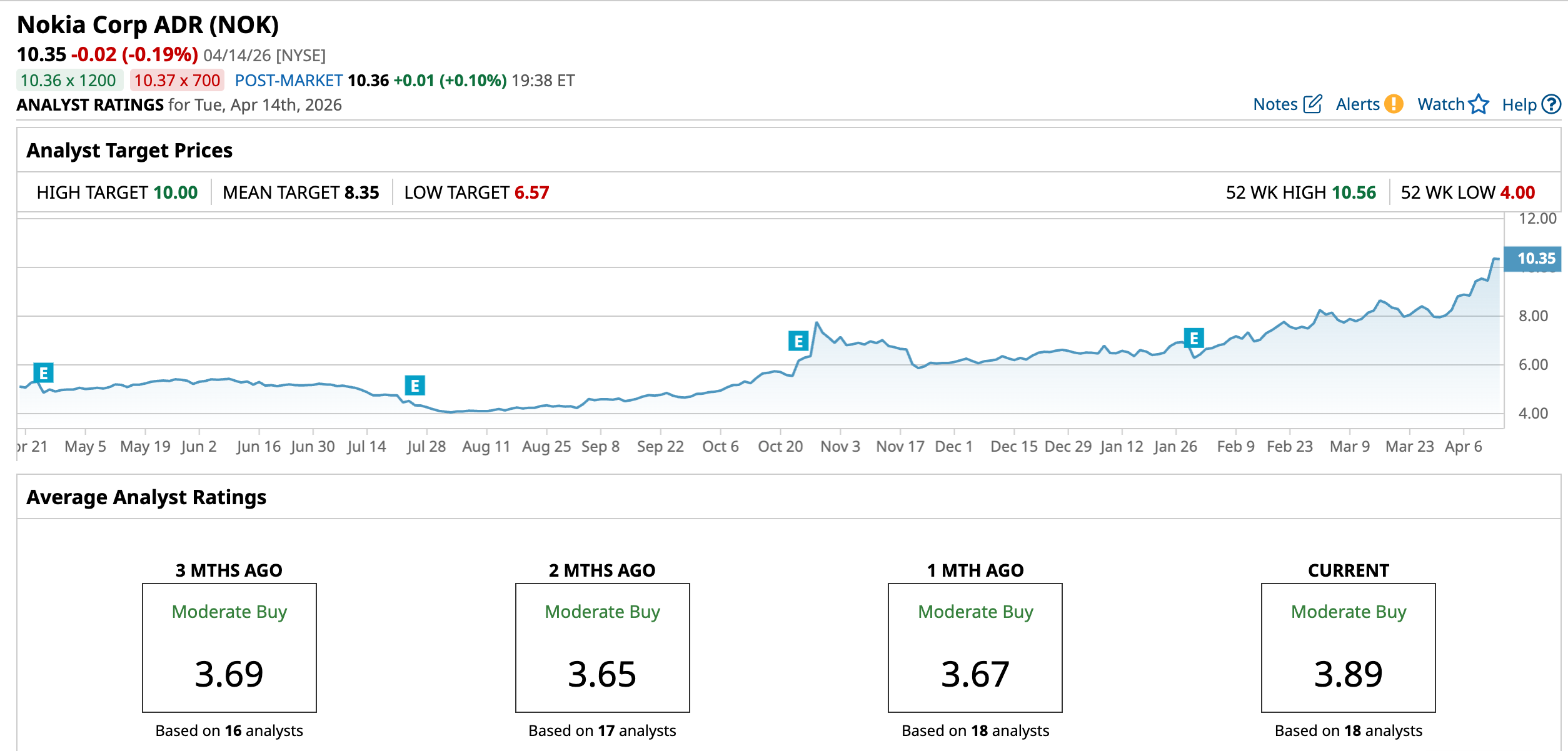

Nokia (NOK) is right in the middle of that story. On April 13, the stock surged to a new 52-week high of $10.48, extending its rebound after Bank of America analyst Oliver Wong upgraded the stock from “Neutral” to “Buy” and called Nokia’s $2.3 billion Infinera deal a major turning point for its optical networking business.

Also, Wong said Nokia’s optical networks segment could grow at a 17% CAGR through 2028, and argued the market is still not fully pricing in the company’s $1 billion Nvidia (NVDA) AI-RAN partnership.

Still, the easy upside may not be as obvious now. Nokia is trading at 24.5 times price-to-earnings, the stock is up about 71% from its 2026 low, and momentum has already pushed it into overbought territory. So the real question is simple: is this the start of a bigger rerating, or are investors showing up after most of the run has already happened?

The Numbers Behind the Rally

Nokia is now mainly a networks and infrastructure company, not a phone maker. It makes its money from mobile networks, fixed and IP networks, cloud and network services, and patent licensing.

Over the last 12 months, the stock is up 107.83%, and it’s gained 59.97% so far this year, which helps explain why it now trades at a forward P/E of 24.51 times versus about 22.46 times for the sector.

There’s also a small income angle. Nokia’s dividend yield is 1.14%, based on an annual dividend of 0.11, with the most recent payout of $0.024 on February 3. The forward payout ratio sits at 29.71%, it pays quarterly, and it has just one year of dividend growth under its belt.

Q4 2025 was steady rather than spectacular. Net sales came in at €6.125 billion ($6.7 billion), up 2% year-over-year (YOY), or €6.130 billion ($6.7 billion) on a comparable basis, with 3% growth in constant currency. Reported gross margin was 44.9%, down 120 basis points, but on a comparable basis it improved to 48.1%, up 90 basis points.

Reported operating profit dropped 37% to €540 million ($592 million), for an 8.8% margin, while comparable operating profit slipped just 3% to €1.058 billion ($1.16 billion), with a 17.3% margin. Reported diluted EPS was €0.10 ($0.11) and comparable EPS was €0.16 ($0.18), down 33% and 11%, respectively. Even so, free cash flow was positive at €226 million ($248 million), and Nokia ended the quarter with €3.378 billion ($3.70 billion) in net cash and interest-bearing investments and €6.791 billion ($7.43 billion) in total cash and investments.

What Is Driving Nokia’s Next Leg of Growth?

Nokia’s next growth phase is largely tied to its push into AI-RAN and next-generation network equipment. Nvidia is putting $1 billion behind that effort, with the two companies teaming up to support the shift from 5G to 6G. That partnership includes Nvidia’s new Arc Aerial RAN Computer, which is built for future telecom workloads, while Nokia is using that platform to roll out new AI-RAN products. T-Mobile U.S. (TMUS) is already working with both companies on bringing this technology into its 6G development, and Dell (DELL) PowerEdge servers are part of the setup.

Nokia has moved the Nvidia relationship further with new customer integrations and successful tests of its anyRAN software on Nvidia’s GPU-based AI-RAN platform with T-Mobile, Indosat, and SoftBank Group (SFTBY). Interest is also picking up from BT (BTGOF), Elisa (ELMUY), NTT DOCOMO, and Vodafone Group (VOD), with support from Dell Technologies, Quanta (PWR), Red Hat, and SuperMicro (SMCI), as Nokia tries to put itself at the center of building and running wireless networks in the next few years.

On the optical side, Nokia is going after the growing need for faster and more efficient network capacity. It has launched a new group of optical products designed for AI-driven networks, and the company says they can cut total ownership costs by as much as 70%. The lineup includes 1.6T, 2.4T, and 3.2T pluggables and transponders for everything from campus and metro networks to long-haul and subsea links. These products are expected to start sampling in mid-2027, with wider availability in the second half of 2027.

What Wall Street Sees From Here

Nokia’s next test comes on April 23, when it reports earnings before the market opens. Wall Street expects EPS of $0.06 for the March quarter, up from $0.03 a year ago, and $0.08 for the June quarter, up from $0.05. For the full year, analysts see earnings reaching $0.40 in 2026 up from $0.33. In other words, the Street is still expecting solid growth from here.

That helps explain why Morgan Stanley has stayed bullish on the stock. Even before Bank of America’s Oliver Wong helped spark Monday’s rally, Morgan Stanley analyst Terence Tsui had already named Nokia one of the firm’s Top Picks for 2026.

He upgraded the stock to “Overweight” in mid-January and later raised his target twice, most recently to €8.50 ($9.32) in March, which was the highest on the Street at the time. His case was based on strong demand tied to AI and cloud infrastructure, a better revenue mix, and solid results from peers across the sector.

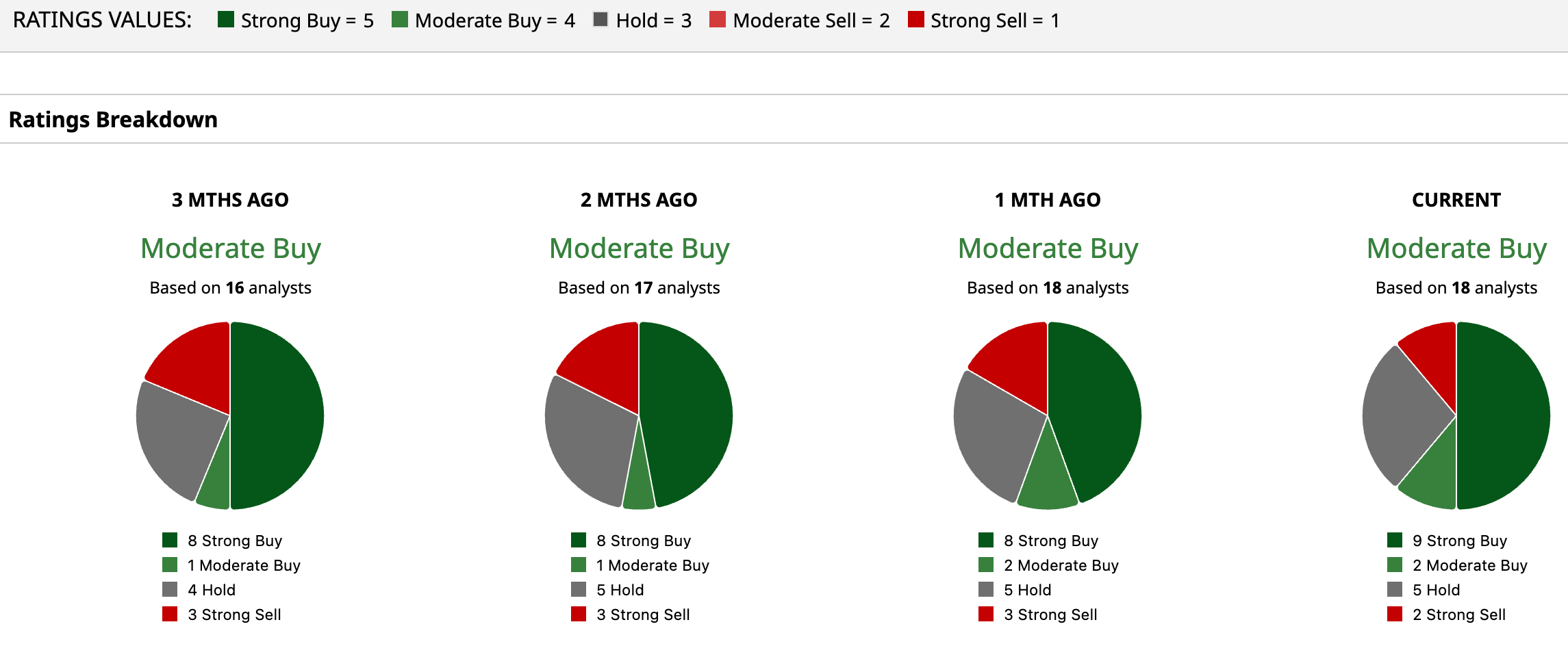

Stepping back, of 18 analysts surveyed, nine rate it a “Strong Buy,” two rate it a “Moderate Buy”, five are a “Hold," and the remaining two are bearish with a “Strong Sell.” The current stock price has surpassed the average price target of $8.35. The issue is that the stock is already trading at $10.35, which puts it about 19% above the mean target.

Conclusion

At this point, Nokia looks more like a “Hold” than a fresh buy at 52‑week highs. The AI‑RAN and optical tailwinds are real, the Nvidia deal and Infinera acquisition give it genuine leverage to the AI and 6G buildout, and earnings are finally inflecting higher. But with the stock up over 100% in a year, trading at a rich multiple, and sitting roughly 25% above the Street’s average target, a lot of that story is already in the price. From here, the risk‑reward skews toward a cooling‑off or sideways drift unless Nokia keeps beating and raising consistently.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Tesla Is Still a ‘Leader in Physical AI’ and You Should Buy TSLA Stock Now, Says UBS

- Turbine Season for Tech: John Rowland on the Next Era of AI Data Center Investments

- IonQ's DARPA Contract Win Makes It the Quantum Computing Stock to Own in 2026

- Lucid Keep Hitting New Lows: Should You Buy LCID Stock or Give Up?