Trust Intel (INTC) CEO Lip-Bu Tan to look out for the companies he is associated with. After forging a partnership with his erstwhile company, Cadence (CDNS), soon after taking over the reins of the beleaguered chip player in March 2025, the Tan-led Intel will now invest in another company with which its CEO has a connection.

What is SambaNova And Why Is Intel Investing In It?

Intel will be partnering with and investing in AI startup SambaNova. The latter is looking to raise about $350 million in Series E financing, and Intel will be a part of this round.

Based out of the tech hub of Silicon Valley, SambaNova describes itself as a "full-stack AI" company. Unlike many competitors who only sell chips, they provide the hardware, the software, and the pre-trained AI models as an integrated system. Their signature technology is a new type of processor architecture designed specifically for “dataflow” computing. Unlike traditional GPUs, which are designed for graphics, the RDU is built from the ground up to move massive amounts of data through AI neural networks with minimal bottlenecks.

Notably, Tan was an early investor in the company, which was founded in 2017, and has served as the chairman of its board. Currently, he serves as the executive chairman of the startup.

Considering this, Tan must have seen value in bringing SambaNova to the Intel fold. What is that value, and can it sustain Intel's newfound momentum?

For starters, the most visible reason can be the SN50 chip from the company. SambaNova's newest flagship chip (announced February 2026) is marketed as an alternative to Nvidia’s (NVDA) B200. It is specifically optimized for "agentic AI"—AI systems that can reason and perform multi-step tasks, claiming up to 5x faster performance and 3x lower total cost of ownership for enterprise inference compared to standard GPU setups.

Additionally, under a new partnership, Intel is integrating its Xeon processors and networking hardware with SambaNova’s RDU accelerators. This allows Intel to offer a complete "GPU alternative" package to big clients like SoftBank (SFTBY), which was named as the first major customer for this joint Intel-SambaNova infrastructure in Japan.

Strategically, Intel's investment in SambaNova is aimed at capturing the huge and rapidly growing agentic AI market. While Intel's Gaudi line focuses on training, SambaNova’s RDU architecture offers a purpose-built engine for this market. The value lies in SambaNova’s ability to map entire trillion-parameter models onto its three-tier memory architecture, drastically reducing the data movement bottlenecks inherent in traditional silicon. By securing this partnership, Intel gains immediate access to a full-stack solution, integrating chips, software, and a ready-to-deploy AI cloud that would have otherwise taken years of internal R&D to replicate.

Moreover, with this alliance with SambaNova, Intel can now offer enterprises the ability to diversify their chip needs beyond the usual players, offering them a heterogeneous data center model. This involves pairing its ubiquitous Xeon CPUs with SambaNova’s specialized accelerators. It creates a legitimate alternative to GPUs for enterprise customers who are increasingly wary of Nvidia’s supply constraints and high power requirements, allowing Intel to recapture high-value data center floor space that was previously slipping toward Broadcom (AVGO) and Nvidia.

However, while this deal for shareholders shows them that Intel is operating tactically by targeting niche but soon-to-be-mainstream markets and looking to gain an early advantage in the same, some issues remain. For instance, from a technical standpoint, the "dataflow" architecture requires a departure from the established CUDA ecosystem, posing a steep adoption curve for developers. There is also the risk of cannibalization or confusion within Intel’s own AI portfolio, as customers must now choose between Gaudi, Falcon Shores, and SambaNova-based systems.

Financials: Not All Is Lost

Intel has had a torrid decade, or rather, decades, might I say. Over the last 10 years, the company's revenues and earnings have clocked negative CAGRs of -0.46% and -45.59%, respectively. INTC stock may be up about 61% in that period, but most of it has been after the government picked up a stake of about 10% in the company.

Yet, are the financials showing signs of improvement? Somewhat, as over the past nine quarters, the company's earnings have topped Street expectations on six occasions. Moreover, the most recent quarter saw the company reporting a beat on both the revenue and earnings front.

Revenues went down by 4% on a year-over-year (YoY) basis to $13.7 billion. While the largest segment of client computing dragged revenues down by declining by 7% from the previous year to $8.2 billion. However, this can pick up in the subsequent quarters with the launch of the company's first AI PC platform built on the Intel 18A process technology—the Intel Core Ultra Series 3 processor. On the AI front, revenues were up 9% on a YoY basis to $4.7 billion. The once much vaunted Foundry business also saw yearly growth in revenues of 4%, to $4.5 billion.

Conversely, earnings went up by 15% in the same period to $0.15 per share, surpassing the consensus estimate of $0.08. This was the second consecutive quarter of earnings beat from the company.

Coming to cash flows, 2025 saw Intel reporting net cash from operating activities of $9.7 billion, up from $8.3 billion in the year-ago period. Overall, the company closed the quarter with a cash balance of $14.3 billion, much ahead of its short-term debt levels of $2.5 billion.

In terms of valuation, the metrics are giving mixed signals. While the forward P/E of 90.32 is considerably above the sector median of 22.06, its forward P/S of 4.05 (vs. the sector median of 2.99) and forward P/CF of 15.35 (vs. the sector median of 16.56) are trading at reasonable levels.

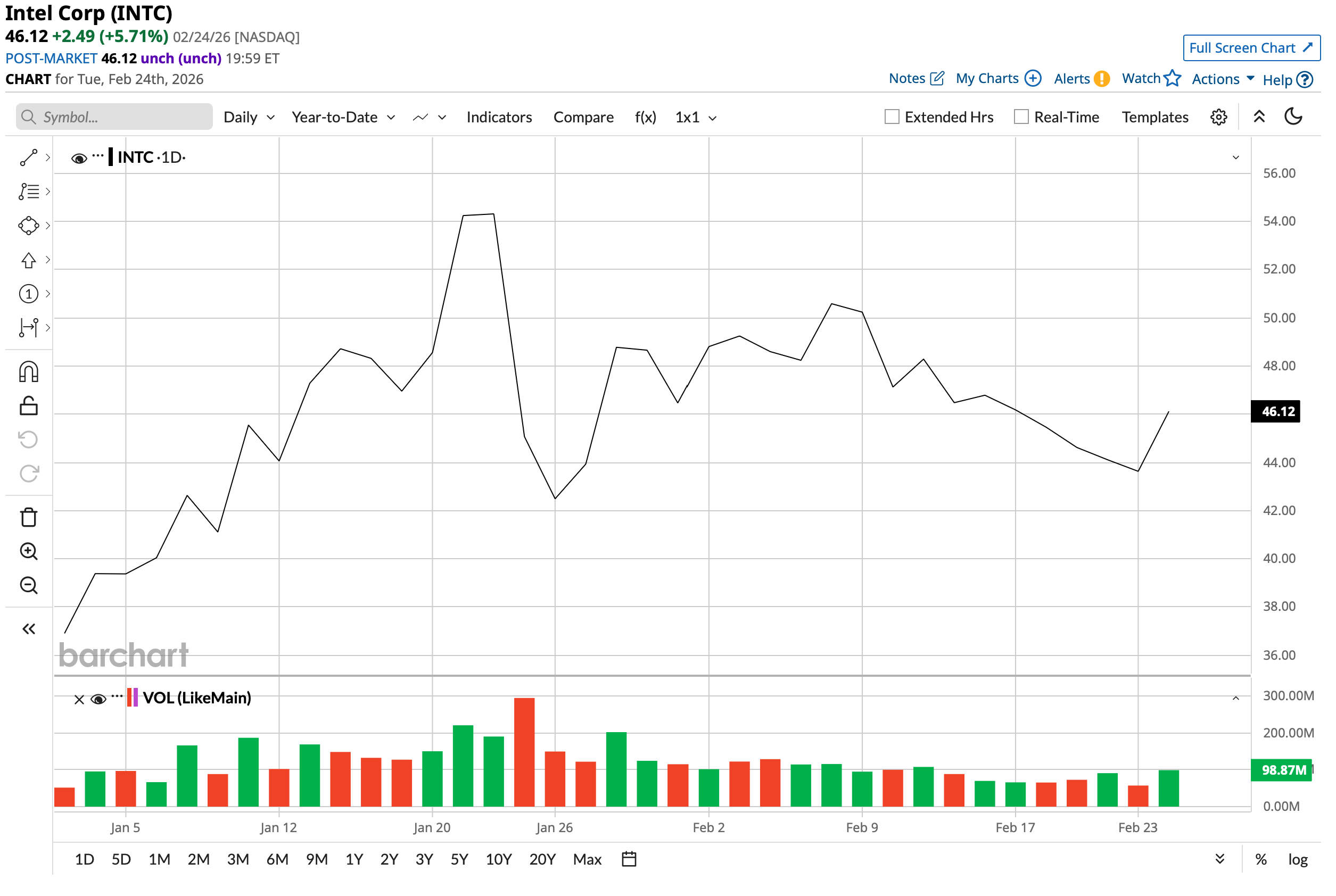

With a market cap of about $218 billion, the INTC stock is up 24% on a year-to-date (YTD) basis.

Analyst Opinion of INTC Stock

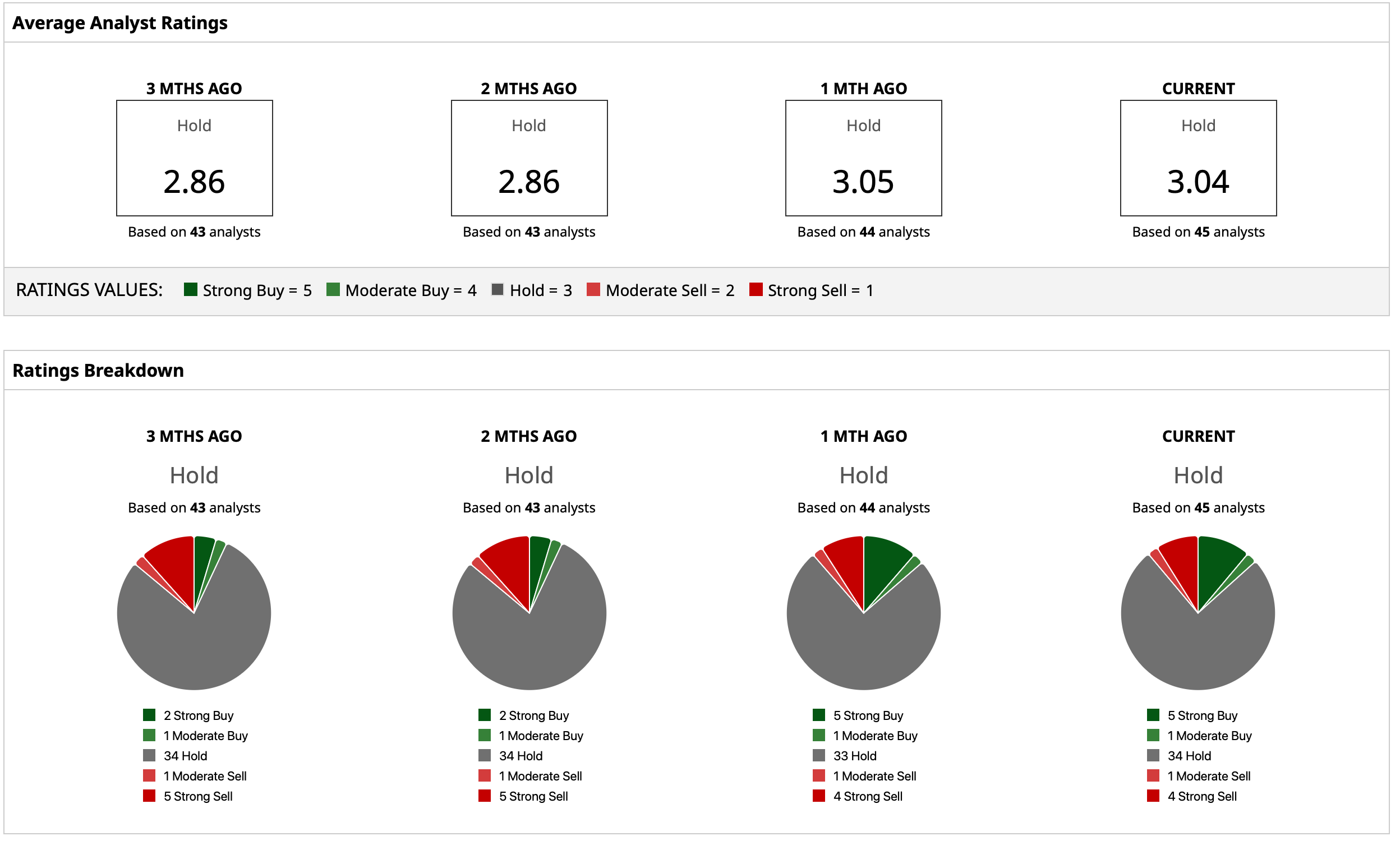

Considering all this, analysts need more convincing of Intel's prowess, as the Street has attributed only a rating of “Hold” for the stock. The mean target price may have already been surpassed. However, the high target price of $66 denotes an upside potential of about 43% from current levels. Out of 45 analysts covering the stock, five have a “Strong Buy” rating, one has a “Moderate Buy” rating, 34 have a “Hold” rating, one has a “Moderate Sell” rating, and four have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.