FOX’s stock price has taken a beating over the past six months, shedding 26.5% of its value and falling to $54.23 per share. This might have investors contemplating their next move.

Is there a buying opportunity in FOX, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think FOX Will Underperform?

Even though the stock has become cheaper, we’re sitting this one out for now. Here are three reasons we avoid FOXA, plus one stock we’d rather own.

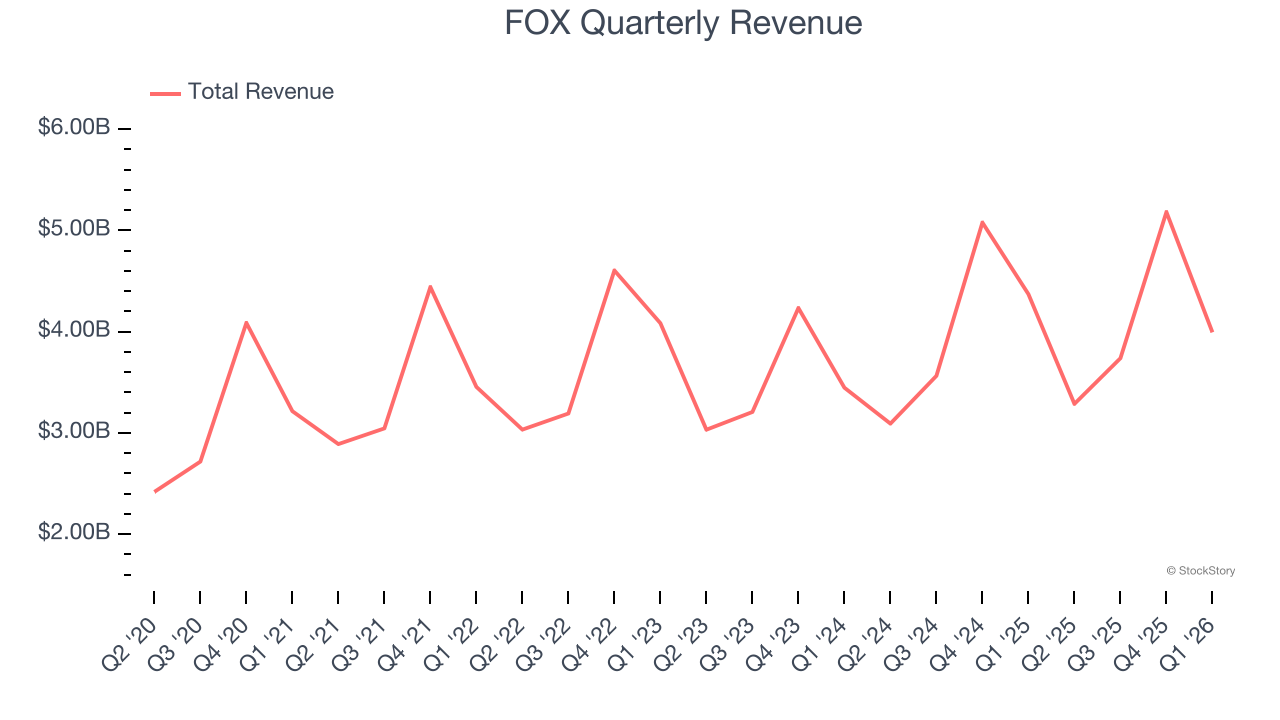

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, FOX’s 5.4% annualized revenue growth over the last five years was weak. This fell short of our benchmark for the consumer discretionary sector.

2. Cash Flow Margin Set to Decline

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Over the next year, analysts predict FOX’s cash conversion will fall. Their consensus estimates imply its free cash flow margin of 13.2% for the last 12 months will decrease to 16.9%.

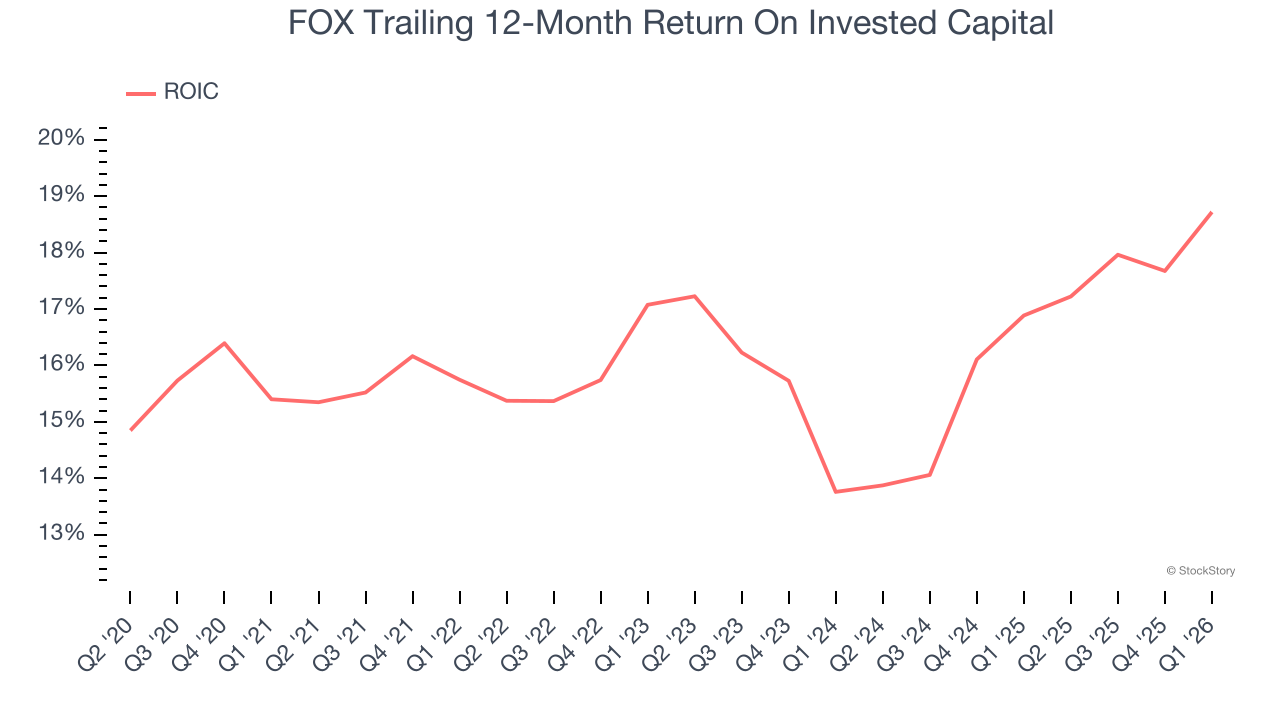

3. New Investments Bear Fruit as ROIC Jumps

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Over the last few years, FOX’s ROIC averaged 1.4 percentage point increases each year. This is a good sign, and we hope the company can continue improving.

Final Judgment

FOX doesn’t pass our quality test. After the recent drawdown, the stock trades at 9.2× forward P/E (or $54.23 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now. Let us point you toward the Amazon and PayPal of Latin America.

Stocks We Would Buy Instead of FOX

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.