As the Q1 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the consumer discretionary - toys and electronics industry, including Mattel (NASDAQ: MAT) and its peers.

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare. Toys and electronic entertainment companies design and sell physical toys, board games, video game hardware, and related digital content, relying on intellectual property, licensed characters, and innovation to drive sales. Tailwinds include evergreen demand from children's demographics, growing adult-collector segments, and digital extensions that create new revenue streams from established franchises. Headwinds are considerable: demand is intensely seasonal (concentrated around holidays) making inventory planning risky. Children's attention is increasingly captured by screen-based entertainment and social media, reducing traditional toy engagement. Hit dependency on blockbuster franchises creates revenue volatility, while tariff exposure on imported goods and rising input costs compress margins.

The 4 consumer discretionary - toys and electronics stocks we track reported a satisfactory Q1. As a group, revenues beat analysts’ consensus estimates by 1.9% while next quarter’s revenue guidance was 13.9% below.

While some consumer discretionary - toys and electronics stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 1.5% since the latest earnings results.

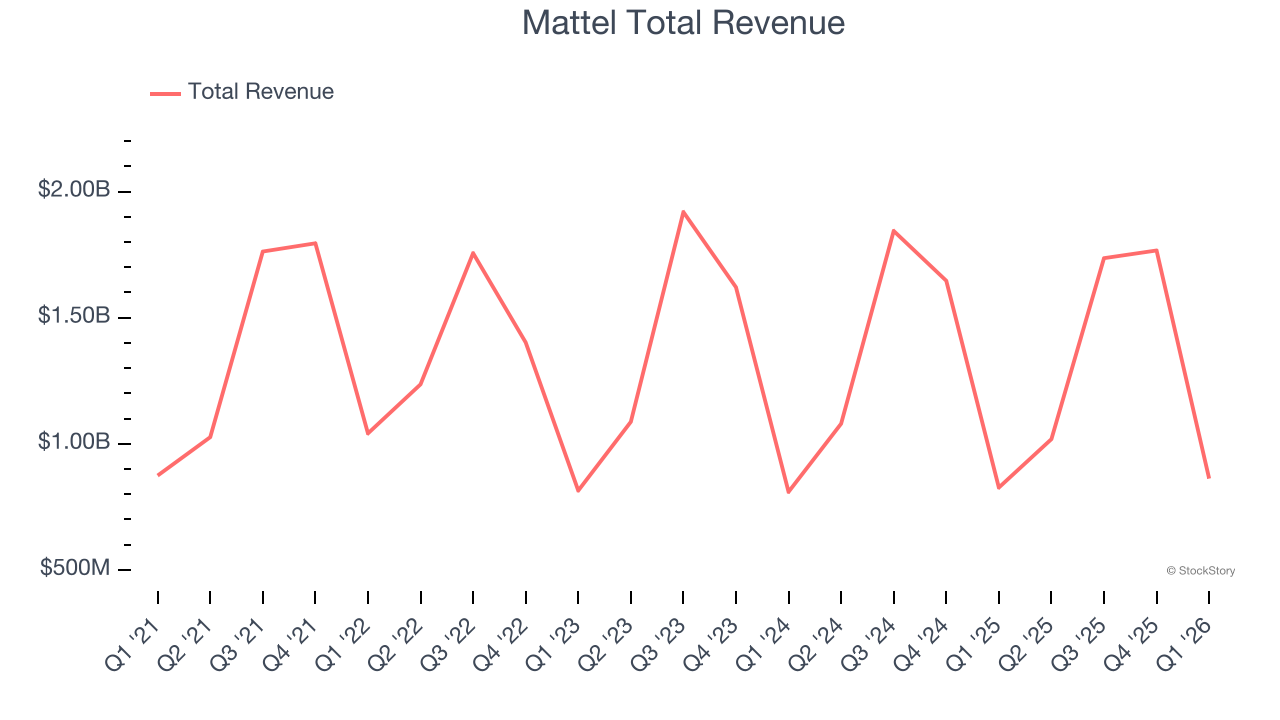

Mattel (NASDAQ: MAT)

Known for the creation of iconic toys such as Barbie and Hotwheels, Mattel (NASDAQ: MAT) is a global children's entertainment company specializing in the design and production of consumer products.

Mattel reported revenues of $862.2 million, up 4.3% year on year. This print exceeded analysts’ expectations by 6.6%. Overall, it was a strong quarter for the company with full-year EPS guidance exceeding analysts’ expectations and a decent beat of analysts’ adjusted operating income estimates.

Ynon Kreiz, Chairman and CEO of Mattel, said: “We are off to a good start to the year, with Net Sales growth and positive consumer demand for our products in the first quarter. We continued to make progress on our strategy to grow our IP driven play and family entertainment business and are seeing top-line acceleration in the second quarter to date. Our digital strategy is progressing, including the integration of Mattel163 mobile games studio and the upcoming launch of two self-published mobile games, and we look forward to the global theatrical release of the Masters of the Universe movie on June 5th.”

Mattel scored the biggest analyst estimate beat of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 6.6% since reporting and currently trades at $13.90.

Is now the time to buy Mattel? Access our full analysis of the earnings results here, it’s free.

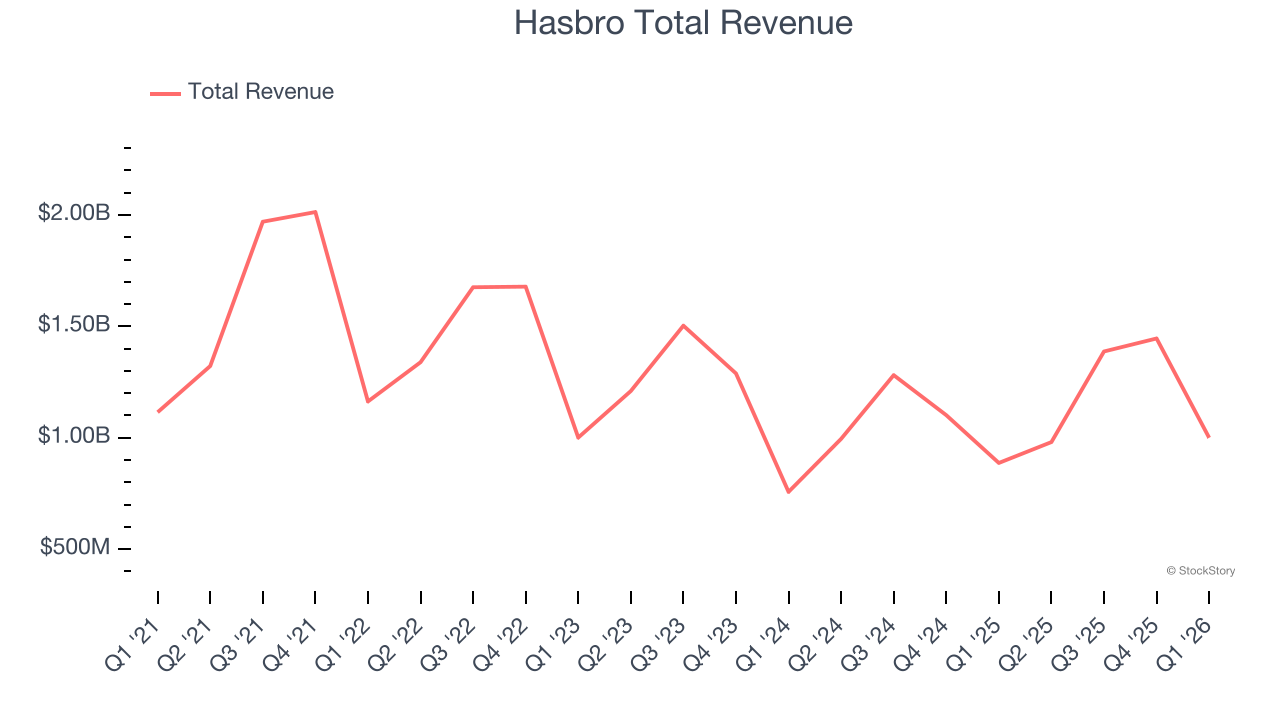

Best Q1: Hasbro (NASDAQ: HAS)

Credited with the creation of toys such as Mr. Potato Head and the Rubik’s Cube, Hasbro (NASDAQ: HAS) is a global entertainment company offering a diverse range of toys, games, and multimedia experiences for children and families.

Hasbro reported revenues of $1 billion, up 12.7% year on year, outperforming analysts’ expectations by 3.8%. The business had a very strong quarter with a beat of analysts’ EPS and adjusted operating income estimates.

Hasbro achieved the fastest revenue growth among its peers. Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 13.4% since reporting. It currently trades at $84.18.

Is now the time to buy Hasbro? Access our full analysis of the earnings results here, it’s free.

Slowest Q1: Bark (NYSE: BARK)

Making a name for itself with the BarkBox, Bark (NYSE: BARK) specializes in subscription-based, personalized pet products.

Bark reported revenues of $86.57 million, down 25% year on year, falling short of analysts’ expectations by 9.1%. It was a slower quarter as it posted revenue guidance for next quarter missing analysts’ expectations and a significant miss of analysts’ adjusted operating income estimates.

Bark delivered the weakest performance against analyst estimates, weakest guidance update, and slowest revenue growth in the group. As expected, the stock is down 7.9% since the results and currently trades at $9.10.

Read our full analysis of Bark’s results here.

Funko (NASDAQ: FNKO)

Boasting partnerships with media franchises like Marvel and One Piece, Funko (NASDAQ: FNKO) is a company specializing in creating and distributing licensed pop culture collectibles.

Funko reported revenues of $200.9 million, up 5.3% year on year. This number beat analysts’ expectations by 6.4%. Overall, it was a strong quarter as it also produced a beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

Funko pulled off the highest guidance raise among its peers. The stock is up 21.7% since reporting and currently trades at $5.43.

Read our full, actionable report on Funko here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.