Robert Half trades at $30.62 per share and has stayed right on track with the overall market, gaining 12% over the last six months. At the same time, the S&P 500 has returned 7.5%.

Is there a buying opportunity in Robert Half, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Do We Think Robert Half Will Underperform?

We don’t have much confidence in Robert Half. Here are three reasons why RHI doesn’t excite us, plus one stock we’d rather own.

1. Long-Term Revenue Growth Disappoints

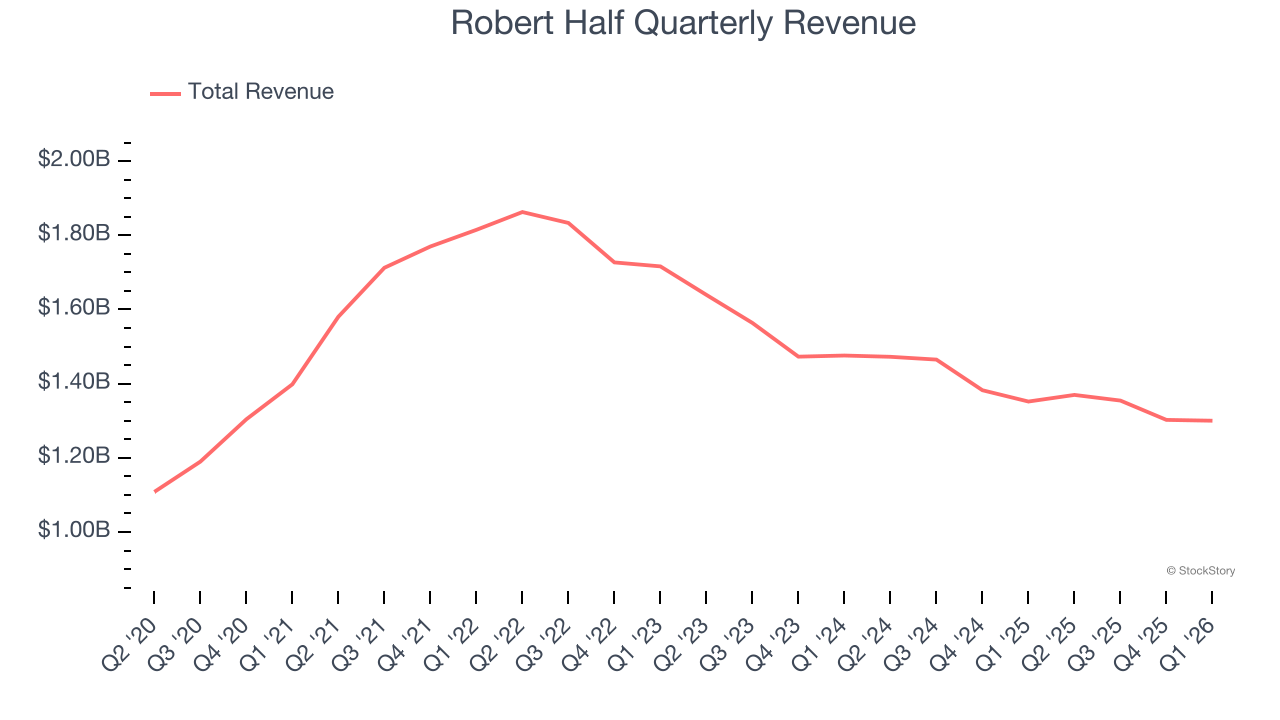

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Robert Half’s sales grew at a sluggish 1.3% compounded annual growth rate over the last five years. This fell short of our benchmarks.

2. EPS Trending Down

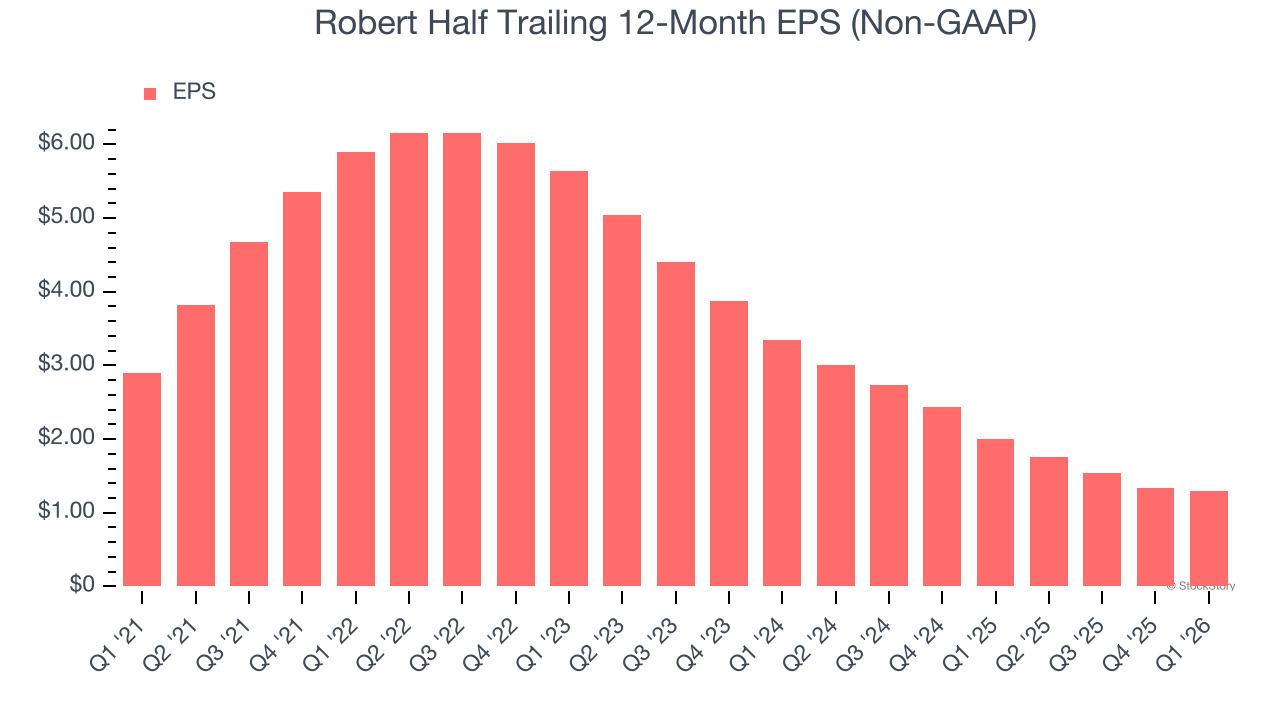

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Robert Half, its EPS declined by 14.8% annually over the last five years while its revenue grew by 1.3%. This tells us the company became less profitable on a per-share basis as it expanded.

3. New Investments Fail to Bear Fruit as ROIC Declines

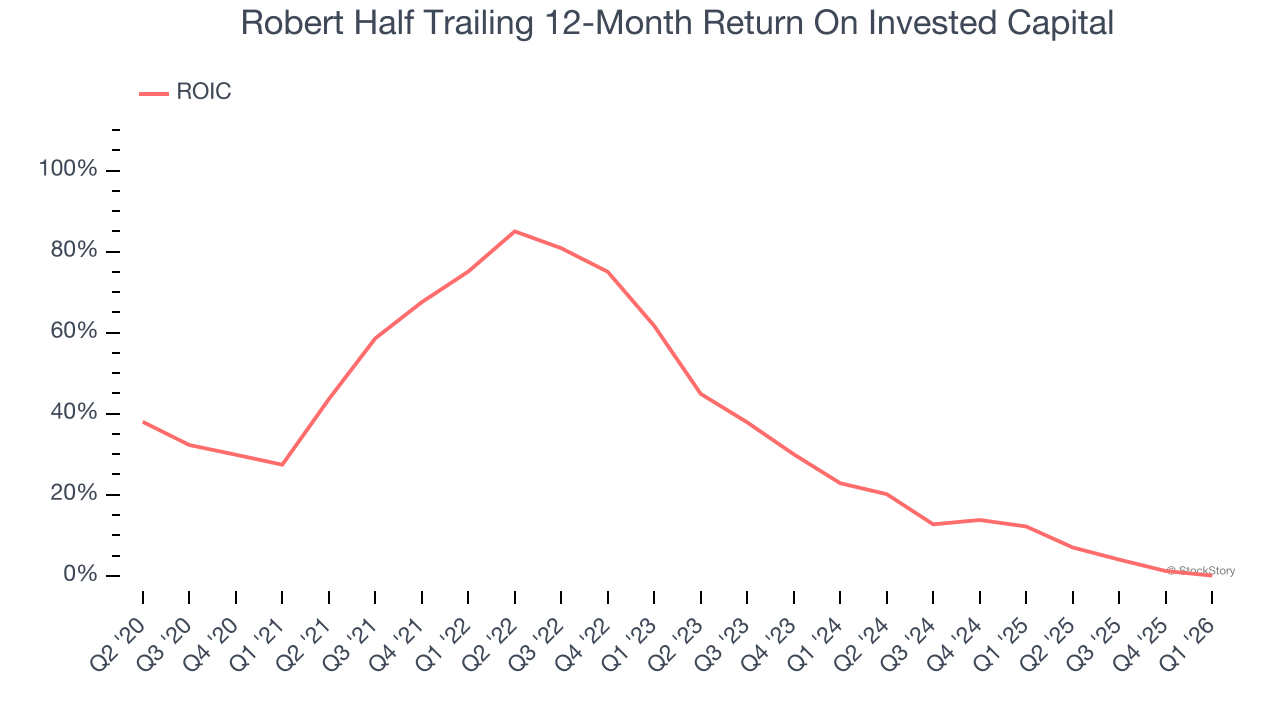

We like to invest in businesses with high returns, but the trend in a company’s ROIC can also be an early indicator of future business quality.

Unfortunately, Robert Half’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

Robert Half falls short of our quality standards. That said, the stock currently trades at 19.8× forward P/E (or $30.62 per share). At this valuation, there’s a lot of good news priced in - you can find more timely opportunities elsewhere. We’d suggest looking at the Amazon and PayPal of Latin America.

Stocks We Would Buy Instead of Robert Half

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.