Video sharing platform Rumble (NASDAQGM:RUM) missed Wall Street’s revenue expectations in Q1 CY2026, but sales rose 7.4% year on year to $25.46 million. Its GAAP loss of $0.12 per share was 33.3% below analysts’ consensus estimates.

Is now the time to buy Rumble? Find out by accessing our full research report, it’s free.

Rumble (RUM) Q1 CY2026 Highlights:

- Revenue: $25.46 million vs analyst estimates of $25.98 million (7.4% year-on-year growth, 2% miss)

- EPS (GAAP): -$0.12 vs analyst expectations of -$0.09 (33.3% miss)

- Adjusted EBITDA: -$20.97 million (-82.4% margin, 7.6% year-on-year growth)

- Operating Margin: -154%, down from -146% in the same quarter last year

- Free Cash Flow was -$17.72 million compared to -$14.63 million in the same quarter last year

- Market Capitalization: $2.82 billion

Company Overview

Founded in 2013 as a champion for content creator rights and free expression, Rumble (NASDAQ: RUM) is a video sharing platform that positions itself as a free speech alternative to mainstream platforms, offering creators more favorable revenue-sharing opportunities.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

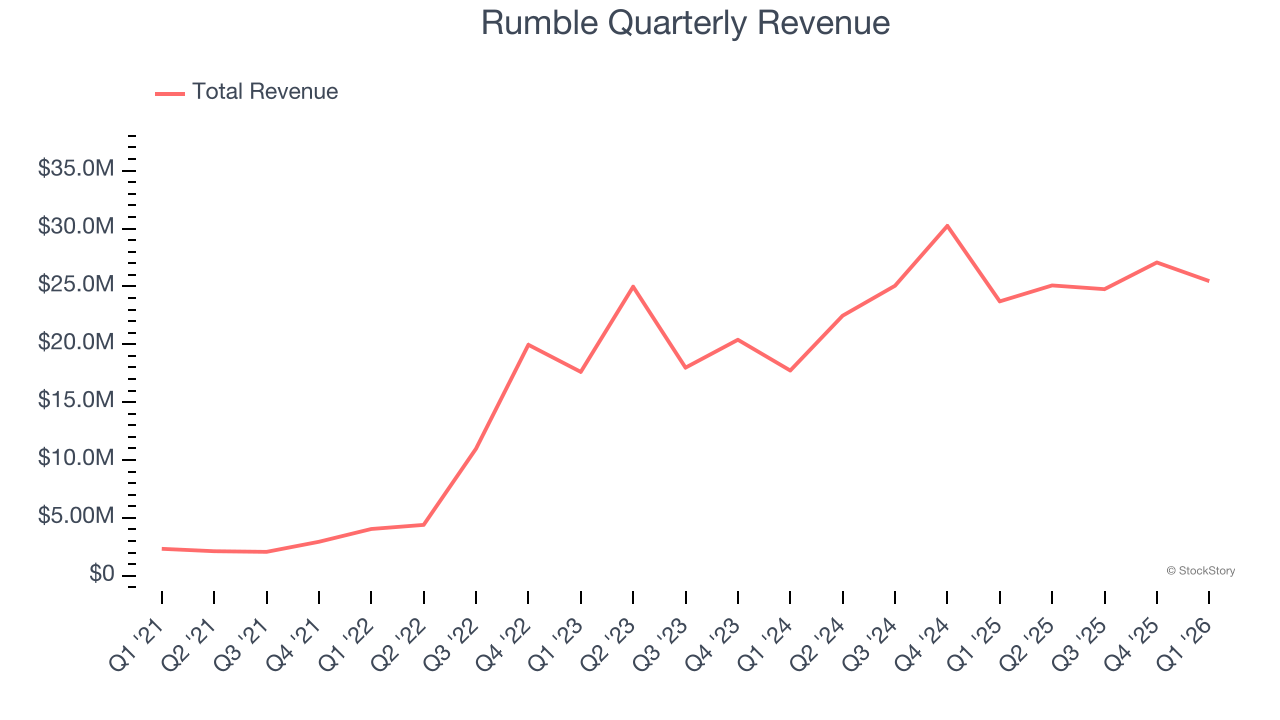

With $102.4 million in revenue over the past 12 months, Rumble is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

As you can see below, Rumble’s 70% annualized revenue growth over the last five years was incredible. This shows it had high demand, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Rumble’s annualized revenue growth of 12.4% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

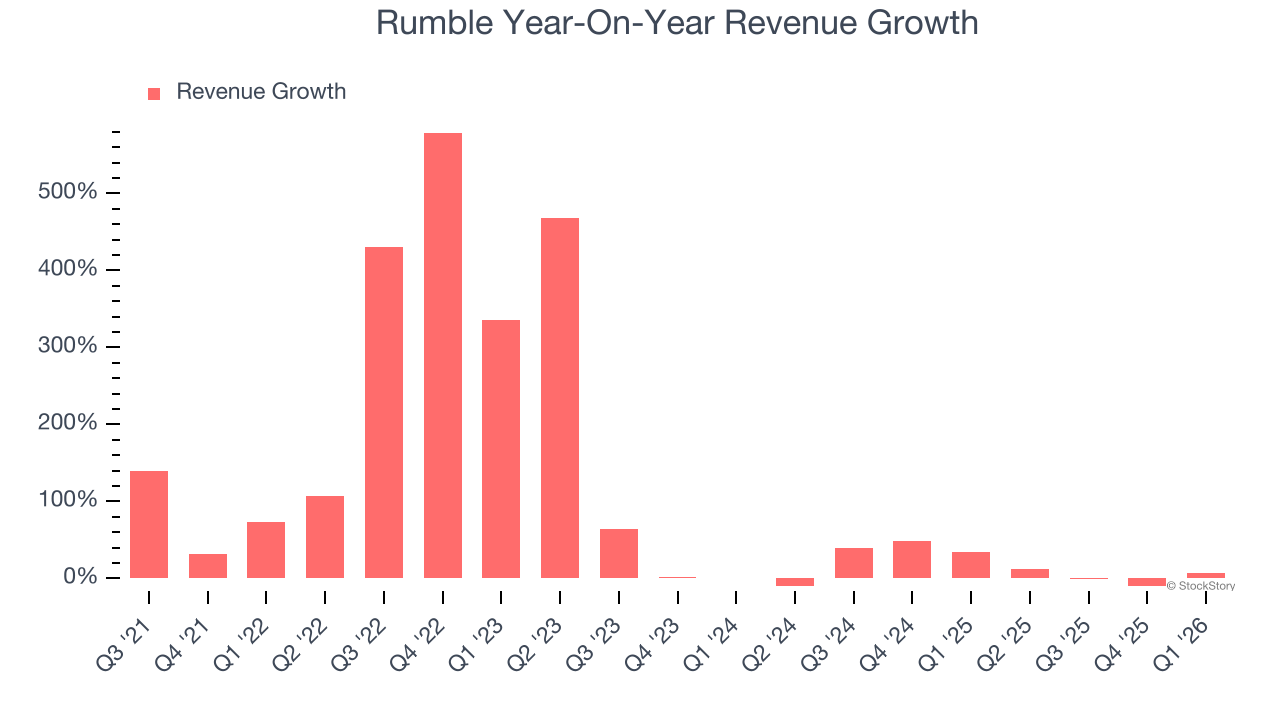

This quarter, Rumble’s revenue grew by 7.4% year on year to $25.46 million, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 466% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and indicates its newer products and services will fuel better top-line performance.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Adjusted Operating Margin

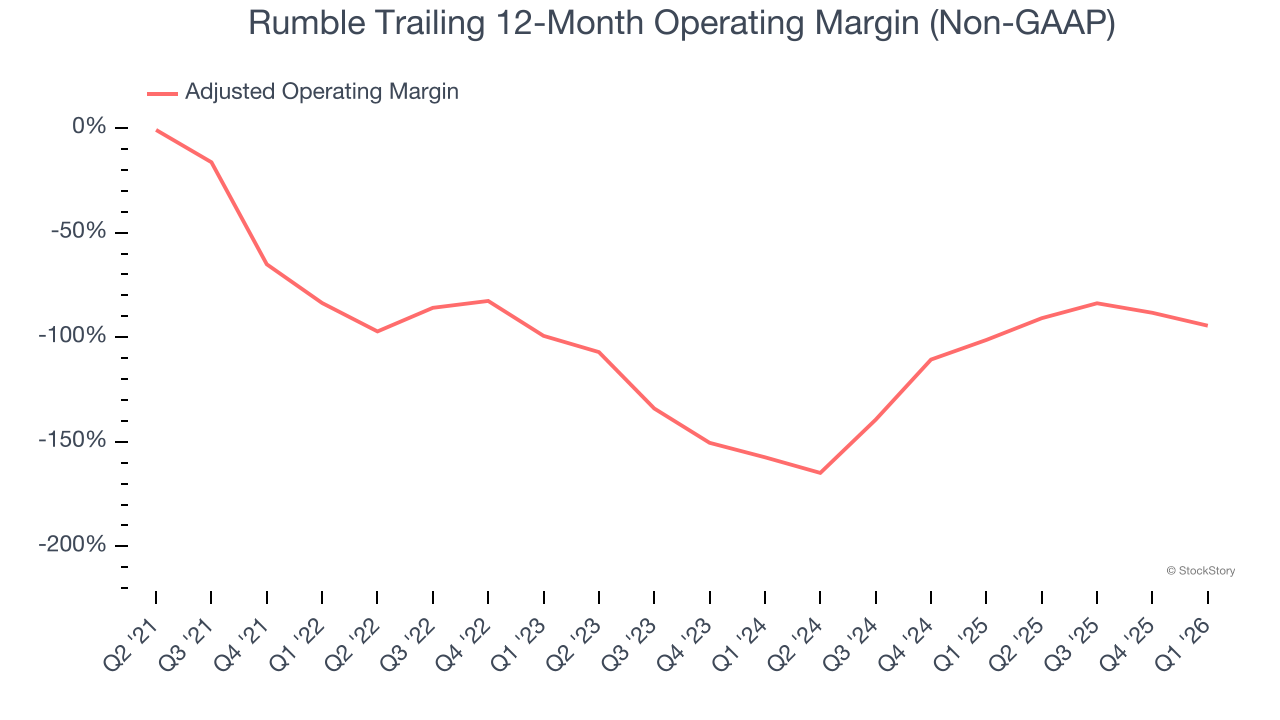

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

Rumble’s high expenses have contributed to an average adjusted operating margin of negative 111% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, Rumble’s adjusted operating margin decreased by 10.8 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Rumble’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

Rumble’s adjusted operating margin was negative 133% this quarter.

Earnings Per Share

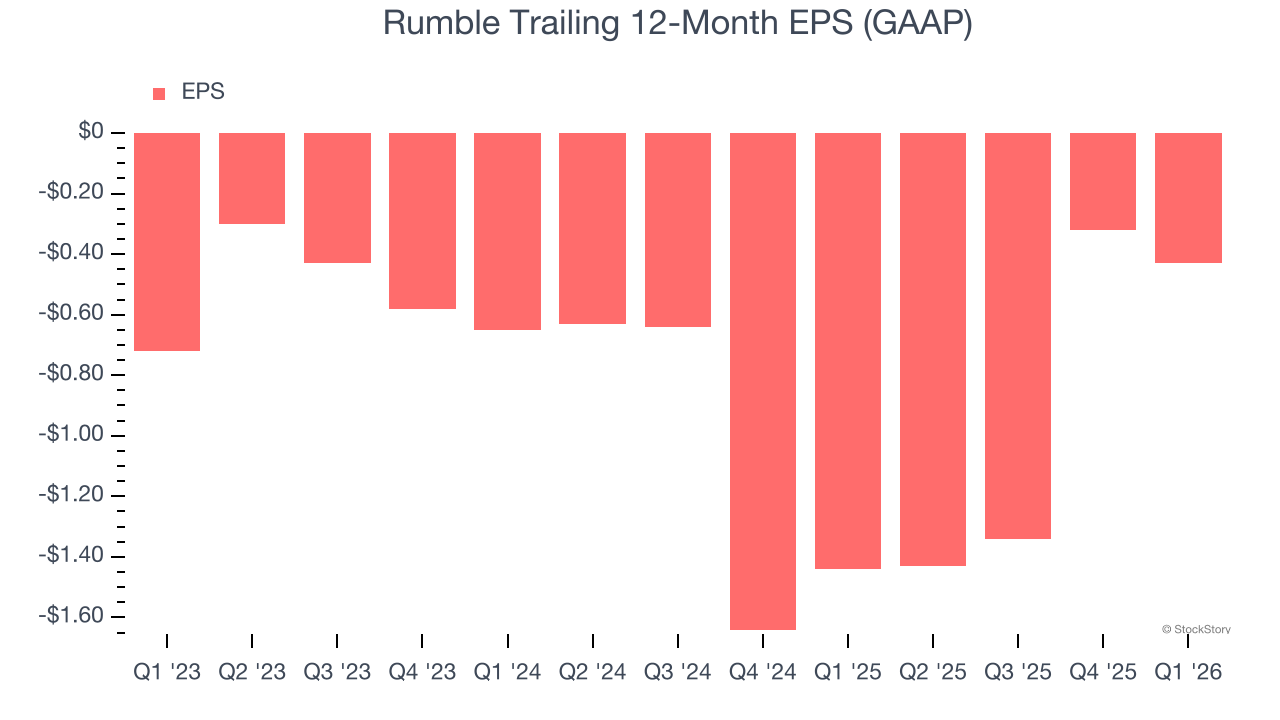

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although Rumble’s full-year earnings are still negative, it reduced its losses and improved its EPS by 32.3% annually over the last three years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Rumble, its two-year annual EPS growth of 18.7% was lower than its three-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q1, Rumble reported EPS of negative $0.12, down from negative $0.01 in the same quarter last year. This print missed analysts’ estimates. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Rumble’s Q1 Results

We struggled to find many positives in these results. Its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 8.9% to $7.50 immediately following the results.

The latest quarter from Rumble’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).