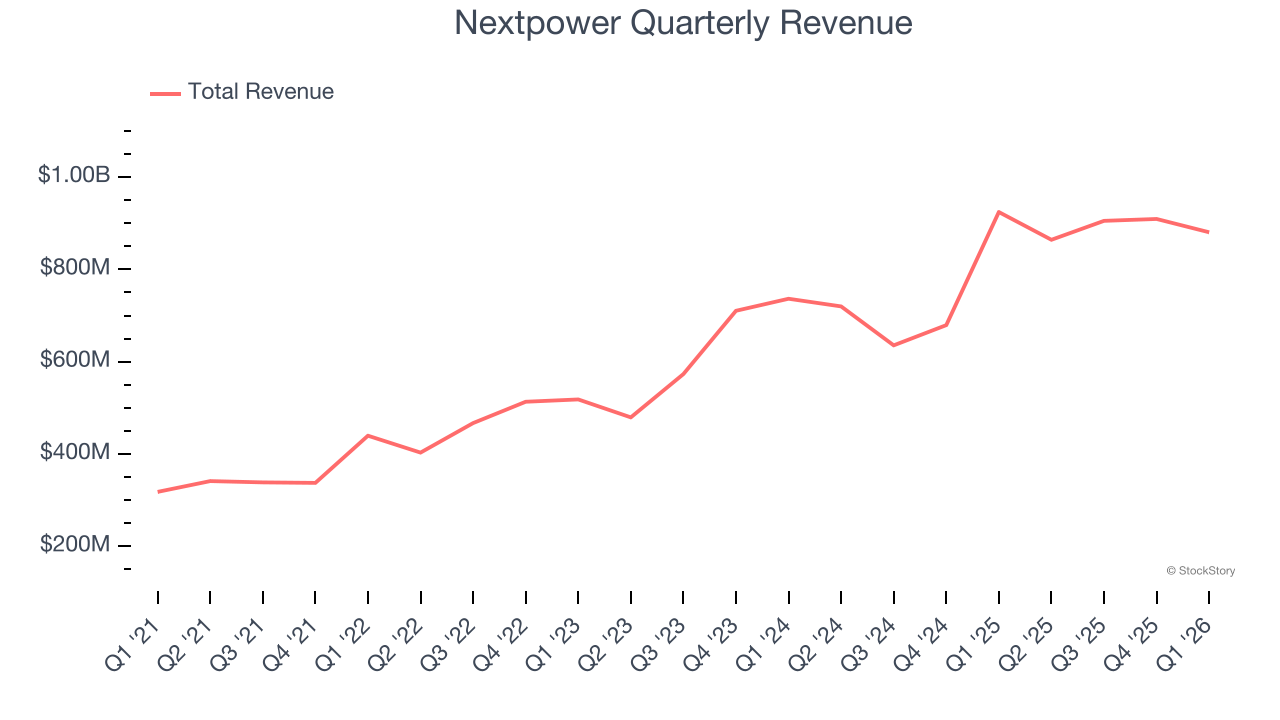

Solar tracker company Nextpower (NASDAQ: NXT) reported Q1 CY2026 results topping the market’s revenue expectations, but sales fell by 4.7% year on year to $880.5 million. The company’s full-year revenue guidance of $3.95 billion at the midpoint came in 0.6% above analysts’ estimates. Its non-GAAP profit of $1.05 per share was 13.5% above analysts’ consensus estimates.

Is now the time to buy Nextpower? Find out by accessing our full research report, it’s free.

Nextpower (NXT) Q1 CY2026 Highlights:

- Revenue: $880.5 million vs analyst estimates of $827 million (4.7% year-on-year decline, 6.5% beat)

- Adjusted EPS: $1.05 vs analyst estimates of $0.93 (13.5% beat)

- Adjusted EBITDA: $201.8 million vs analyst estimates of $182.1 million (22.9% margin, 10.8% beat)

- Adjusted EPS guidance for the upcoming financial year 2027 is $4.40 at the midpoint, missing analyst estimates by 8.2%

- EBITDA guidance for the upcoming financial year 2027 is $862.5 million at the midpoint, below analyst estimates of $941.9 million

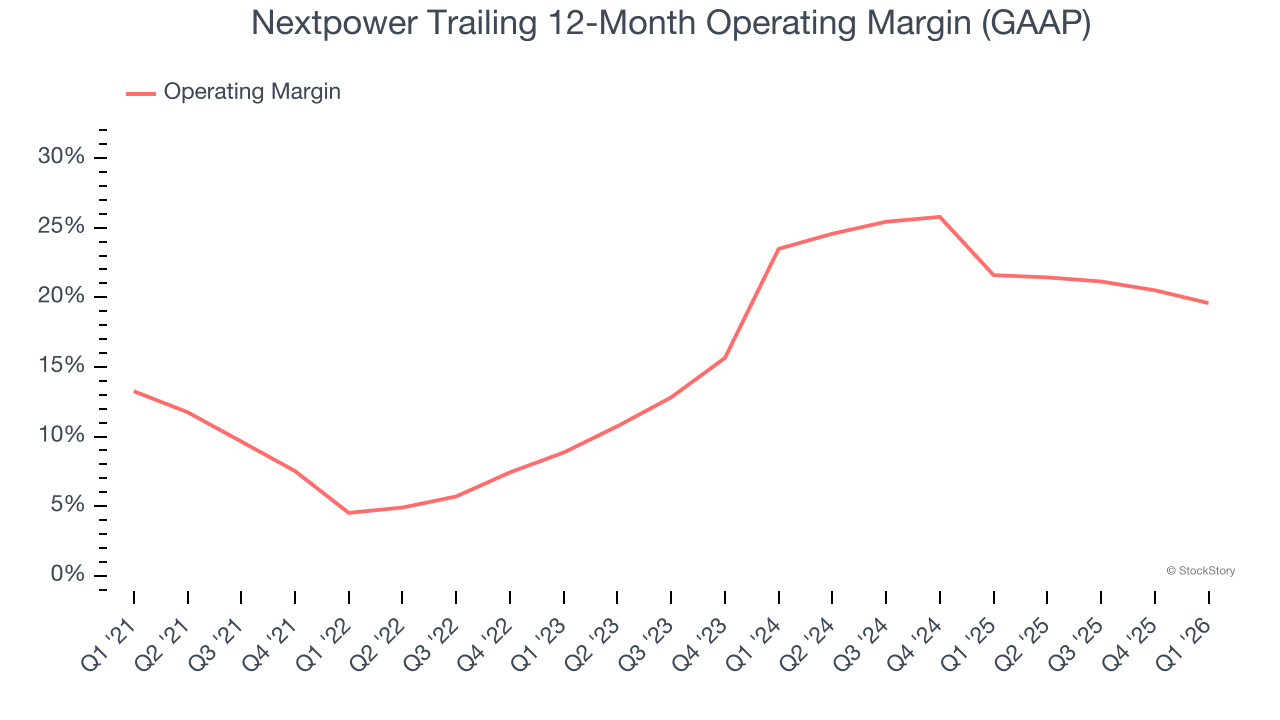

- Operating Margin: 17.4%, down from 21.1% in the same quarter last year

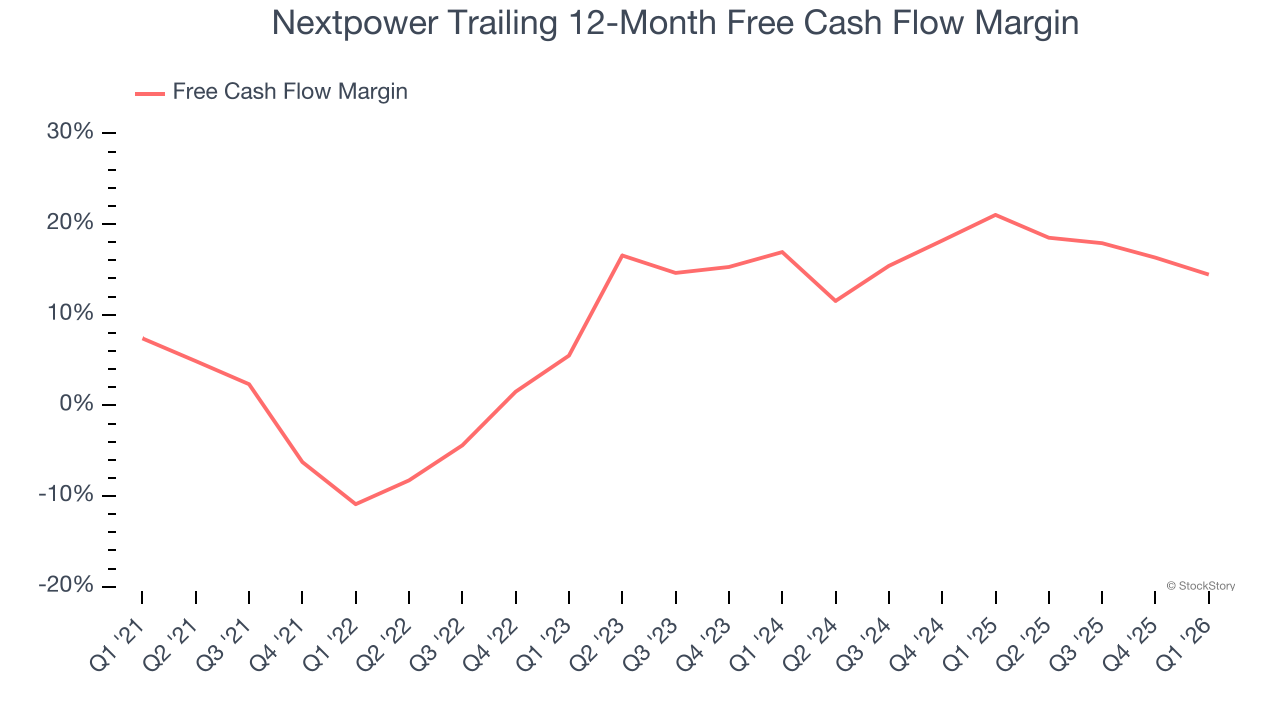

- Free Cash Flow Margin: 17.4%, down from 24.6% in the same quarter last year

- Market Capitalization: $18.75 billion

Company Overview

With its technology playing a key role in the massive 1.2 gigawatt Noor Abu Dhabi solar farm project, Nextpower (NASDAQ: NXT) is a provider of solar tracker systems that help solar panels follow the sun.

Revenue Growth

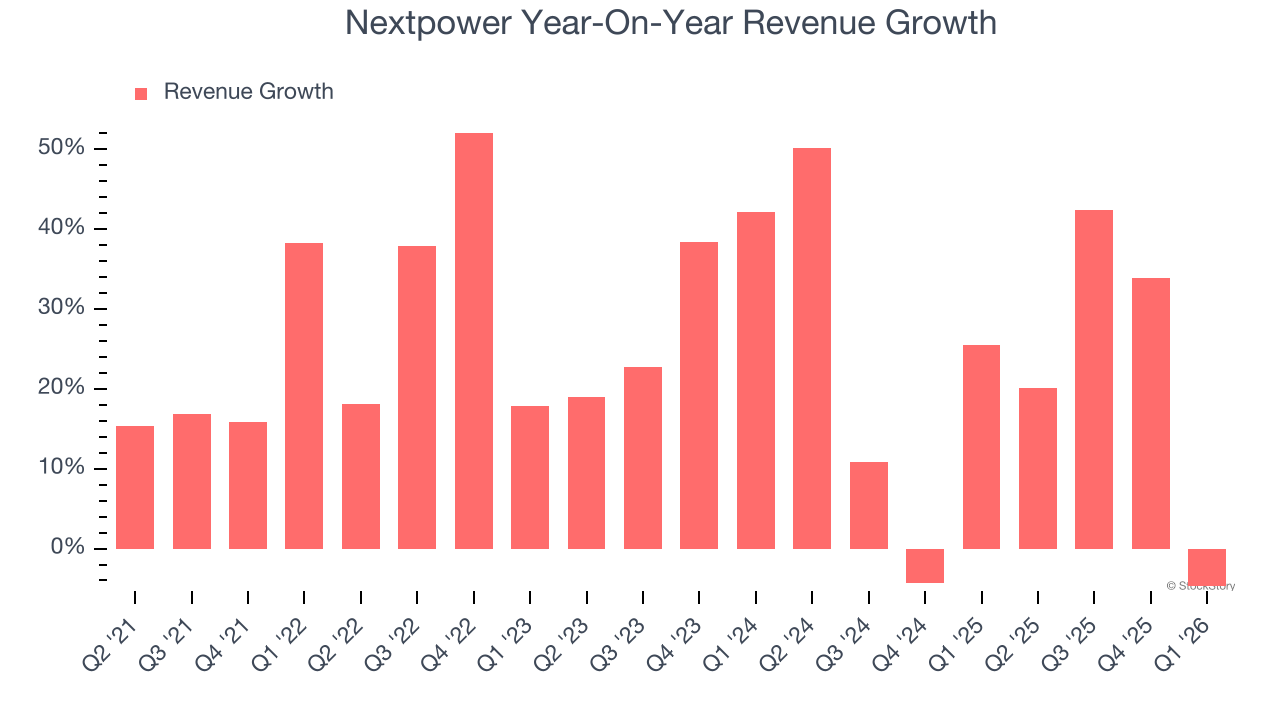

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Nextpower’s 24.4% annualized revenue growth over the last five years was incredible. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Nextpower’s annualized revenue growth of 19.3% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Nextpower’s revenue fell by 4.7% year on year to $880.5 million but beat Wall Street’s estimates by 6.5%.

Looking ahead, sell-side analysts expect revenue to grow 9.5% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is healthy and indicates the market is baking in success for its products and services.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Nextpower has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 17.4%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Nextpower’s operating margin rose by 15.1 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, Nextpower generated an operating margin profit margin of 17.4%, down 3.7 percentage points year on year. Since Nextpower’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Nextpower has shown robust cash profitability, enabling it to comfortably ride out cyclical downturns while investing in plenty of new offerings and returning capital to investors. The company’s free cash flow margin averaged 12.2% over the last five years, quite impressive for an industrials business.

Taking a step back, we can see that Nextpower’s margin expanded by 25.3 percentage points during that time. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Nextpower’s free cash flow clocked in at $153.6 million in Q1, equivalent to a 17.4% margin. The company’s cash profitability regressed as it was 7.1 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because capital expenditures can be seasonal and companies often stockpile inventory in anticipation of higher demand, leading to short-term swings. Long-term trends trump temporary fluctuations.

Key Takeaways from Nextpower’s Q1 Results

We were impressed by how significantly Nextpower blew past analysts’ EBITDA expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year EBITDA guidance missed. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 15.5% to $145.03 immediately after reporting.

Nextpower may have had a good quarter, but does that mean you should invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).