Bristol-Myers Squibb has had an impressive run over the past six months as its shares have beaten the S&P 500 by 5.7%. The stock now trades at $55.77, marking a 13.6% gain. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy Bristol-Myers Squibb, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Bristol-Myers Squibb Not Exciting?

We’re glad investors have benefited from the price increase, but we're cautious about Bristol-Myers Squibb. Here are three reasons why BMY doesn't excite us and a stock we'd rather own.

1. Long-Term Revenue Growth Disappoints

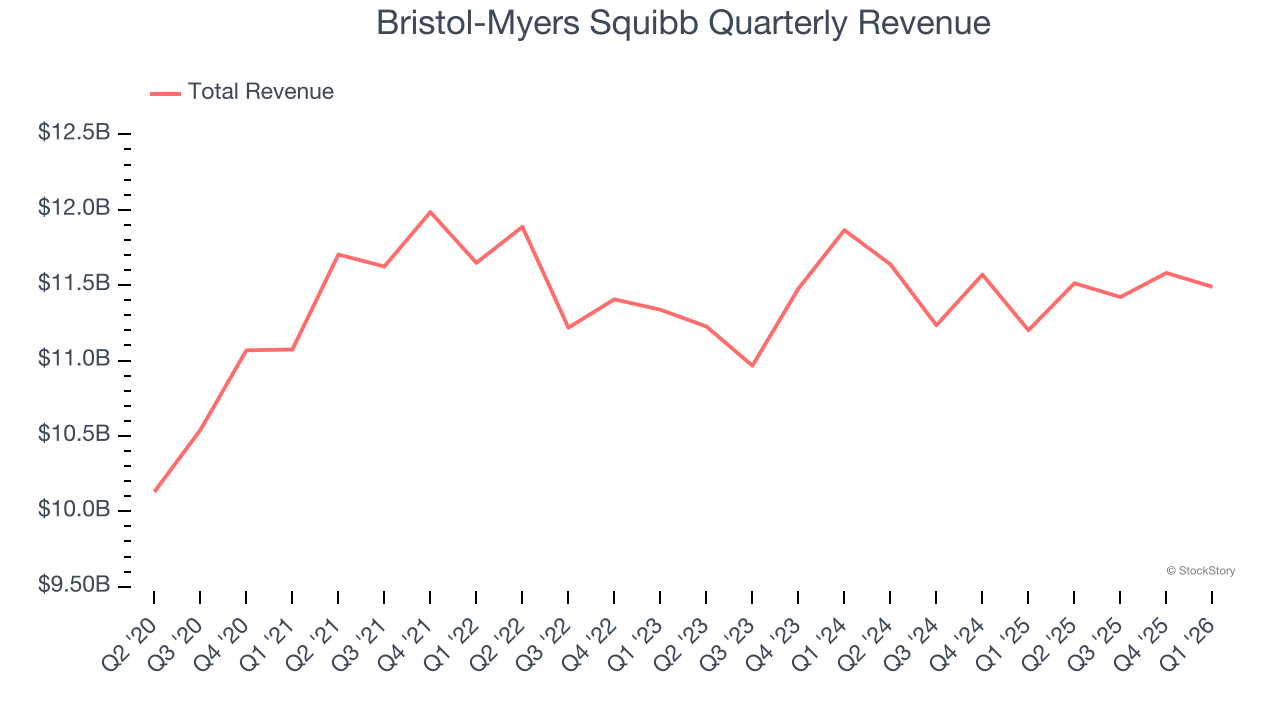

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Bristol-Myers Squibb’s sales grew at a tepid 1.4% compounded annual growth rate over the last five years. This was below our standards.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Bristol-Myers Squibb’s revenue to drop by 4%, a decrease from its 1.4% annualized growth for the past five years. This projection is underwhelming and suggests its products and services will face some demand challenges.

3. EPS Trending Down

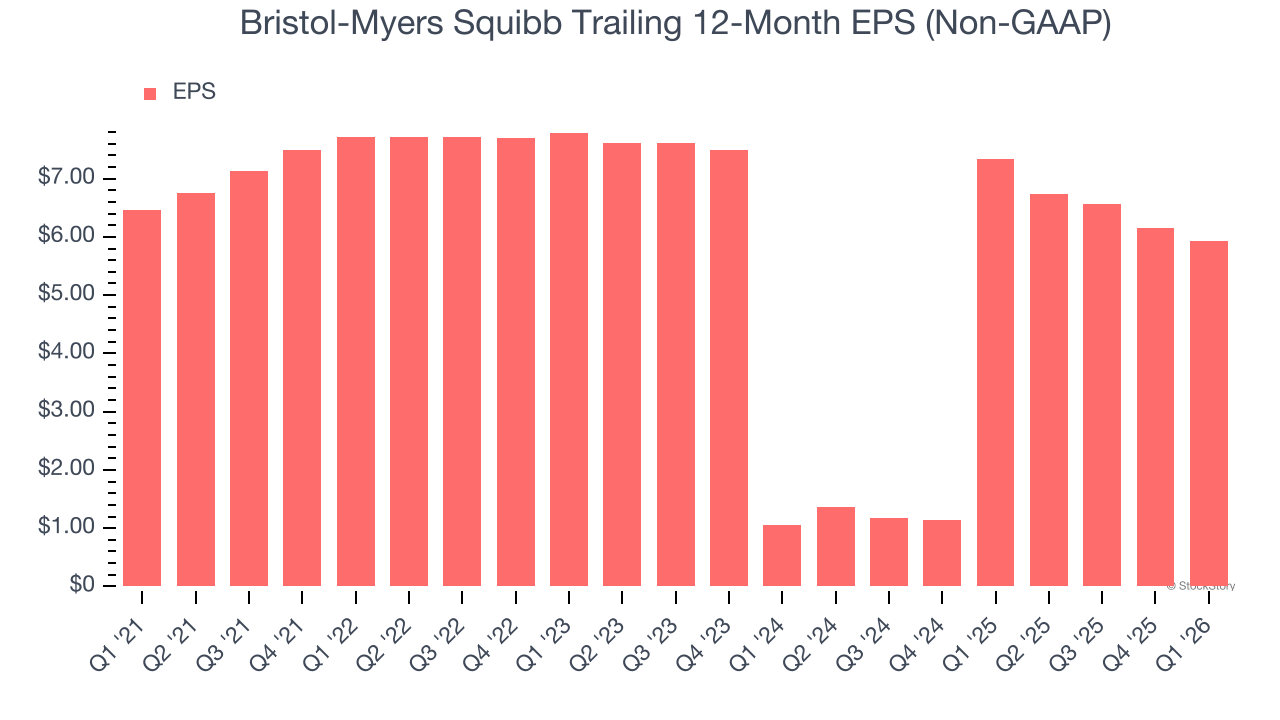

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Bristol-Myers Squibb, its EPS declined by 1.7% annually over the last five years while its revenue grew by 1.4%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Bristol-Myers Squibb’s business quality ultimately falls short of our standards. With its shares outperforming the market lately, the stock trades at 9.2× forward P/E (or $55.77 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

Stocks We Would Buy Instead of Bristol-Myers Squibb

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.