Customer engagement platform Twilio (NYSE: TWLO) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 20% year on year to $1.41 billion. Guidance for next quarter’s revenue was optimistic at $1.43 billion at the midpoint, 2.6% above analysts’ estimates. Its non-GAAP profit of $1.50 per share was 18% above analysts’ consensus estimates.

Is now the time to buy Twilio? Find out by accessing our full research report, it’s free.

Twilio (TWLO) Q1 CY2026 Highlights:

- Revenue: $1.41 billion vs analyst estimates of $1.34 billion (20% year-on-year growth, 4.7% beat)

- Adjusted EPS: $1.50 vs analyst estimates of $1.27 (18% beat)

- Adjusted Operating Income: $278.9 million vs analyst estimates of $245.7 million (19.8% margin, 13.5% beat)

- Revenue Guidance for Q2 CY2026 is $1.43 billion at the midpoint, above analyst estimates of $1.39 billion

- Adjusted EPS guidance for Q2 CY2026 is $1.30 at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: 7.7%, up from 2% in the same quarter last year

- Free Cash Flow Margin: 9.4%, down from 18.7% in the previous quarter

- Net Revenue Retention Rate: 114%, up from 108% in the previous quarter

- Market Capitalization: $21.35 billion

Company Overview

Known for the clever "Twilio Magic" demo that had developers creating functioning communications apps in minutes, Twilio (NYSE: TWLO) provides a platform that enables businesses to communicate with their customers through voice, messaging, email, and other digital channels.

Revenue Growth

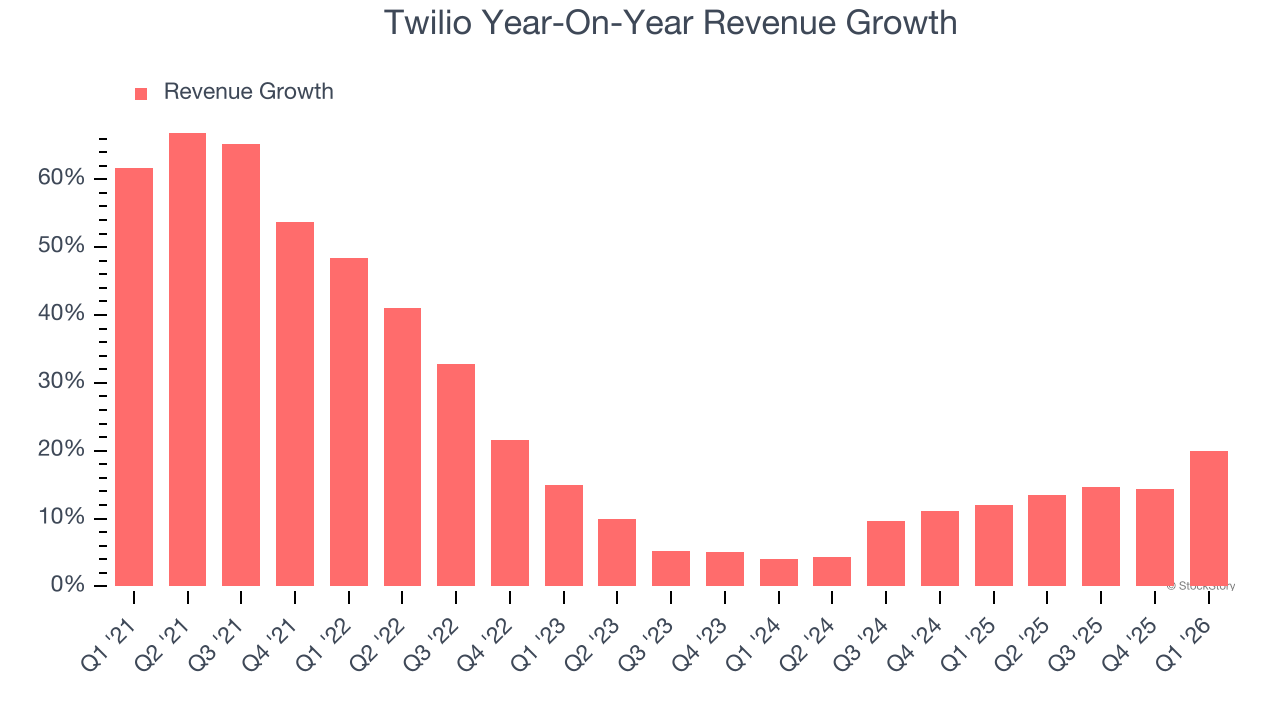

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Twilio grew its sales at a decent 21.7% compounded annual growth rate. Its growth was slightly above the average software company and shows its offerings resonate with customers.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Twilio’s recent performance shows its demand has slowed as its annualized revenue growth of 12.4% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Twilio reported year-on-year revenue growth of 20%, and its $1.41 billion of revenue exceeded Wall Street’s estimates by 4.7%. Company management is currently guiding for a 16% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 9.7% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Customer Retention

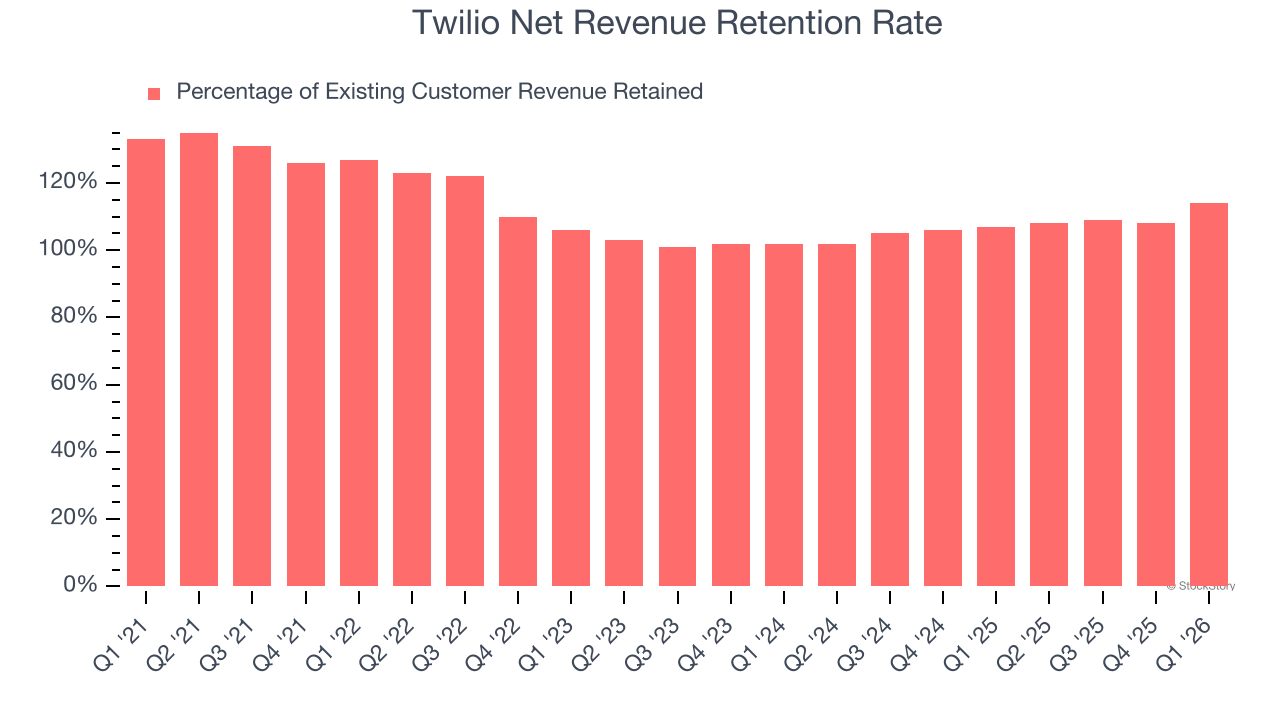

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Twilio’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 110% in Q1. This means Twilio would’ve grown its revenue by 9.7% even if it didn’t win any new customers over the last 12 months.

Trending up over the last year, Twilio has a decent net retention rate, showing us that its customers not only tend to stick around but also get increasing value from its software over time.

Key Takeaways from Twilio’s Q1 Results

We were impressed by Twilio’s superb growth in net revenue retention this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Revenue guidance for next quarter was also ahead. Overall, we think this was a very good quarter with some key metrics above expectations. The stock traded up 15.7% to $169.35 immediately following the results.

Sure, Twilio had a solid quarter, but if we look at the bigger picture, is this stock a buy? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).