Healthcare services company The Ensign Group (NASDAQ: ENSG). missed Wall Street’s revenue expectations in Q1 CY2026, but sales rose 18.4% year on year to $1.39 billion. On the other hand, the company’s full-year revenue guidance of $5.84 billion at the midpoint came in 0.5% above analysts’ estimates. Its non-GAAP profit of $1.85 per share was 1.8% above analysts’ consensus estimates.

Is now the time to buy The Ensign Group? Find out by accessing our full research report, it’s free.

The Ensign Group (ENSG) Q1 CY2026 Highlights:

- Revenue: $1.39 billion vs analyst estimates of $1.52 billion (18.4% year-on-year growth, 8.4% miss)

- Adjusted EPS: $1.85 vs analyst estimates of $1.82 (1.8% beat)

- Adjusted EBITDA: $171.2 million vs analyst estimates of $167 million (12.3% margin, 2.5% beat)

- The company slightly lifted its revenue guidance for the full year to $5.84 billion at the midpoint from $5.81 billion

- Adjusted EPS guidance for the full year is $7.55 at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: 9%, in line with the same quarter last year

- Sales Volumes fell 86.3% year on year (12.5% in the same quarter last year)

- Market Capitalization: $10.89 billion

“Our local leaders and their teams continue to be examples of excellence in healthcare services as they earn the trust of patients, families, and their local healthcare communities through high-quality clinical outcomes. As each operation solidifies its reputation in its respective market, they are not only seeing more patients, but they are also being entrusted to care for increasingly complex cases, including a larger share of Medicare, managed care, and other skilled patients. As we’ve said many times, our consistent financial performance is a direct reflection of a relentless, patient-focused culture—one that empowers our frontline teams to deliver exceptional care in a family-like environment where people genuinely care about one another,” said Barry Port, Ensign’s Chief Executive Officer.

Company Overview

Founded in 1999 and named after a naval term for a flag-bearing ship, The Ensign Group (NASDAQ: ENSG) operates skilled nursing facilities, senior living communities, and rehabilitation services across 15 states, primarily serving high-acuity patients recovering from various medical conditions.

Revenue Growth

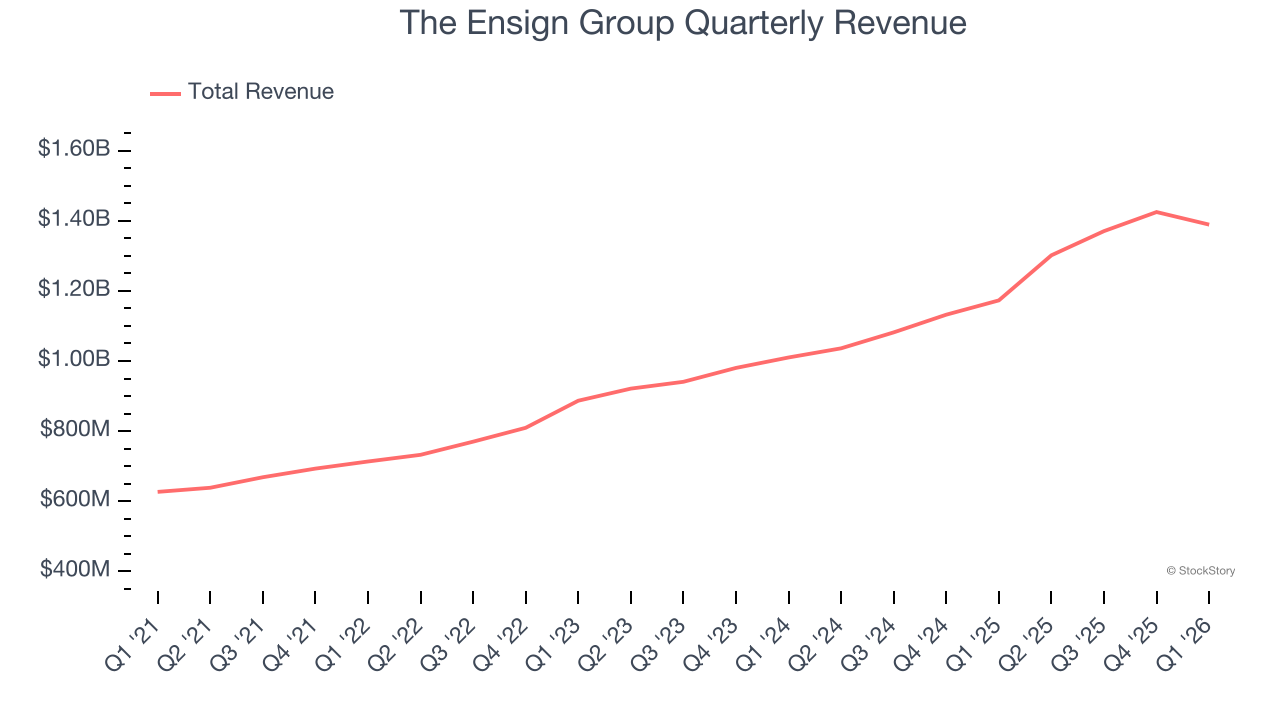

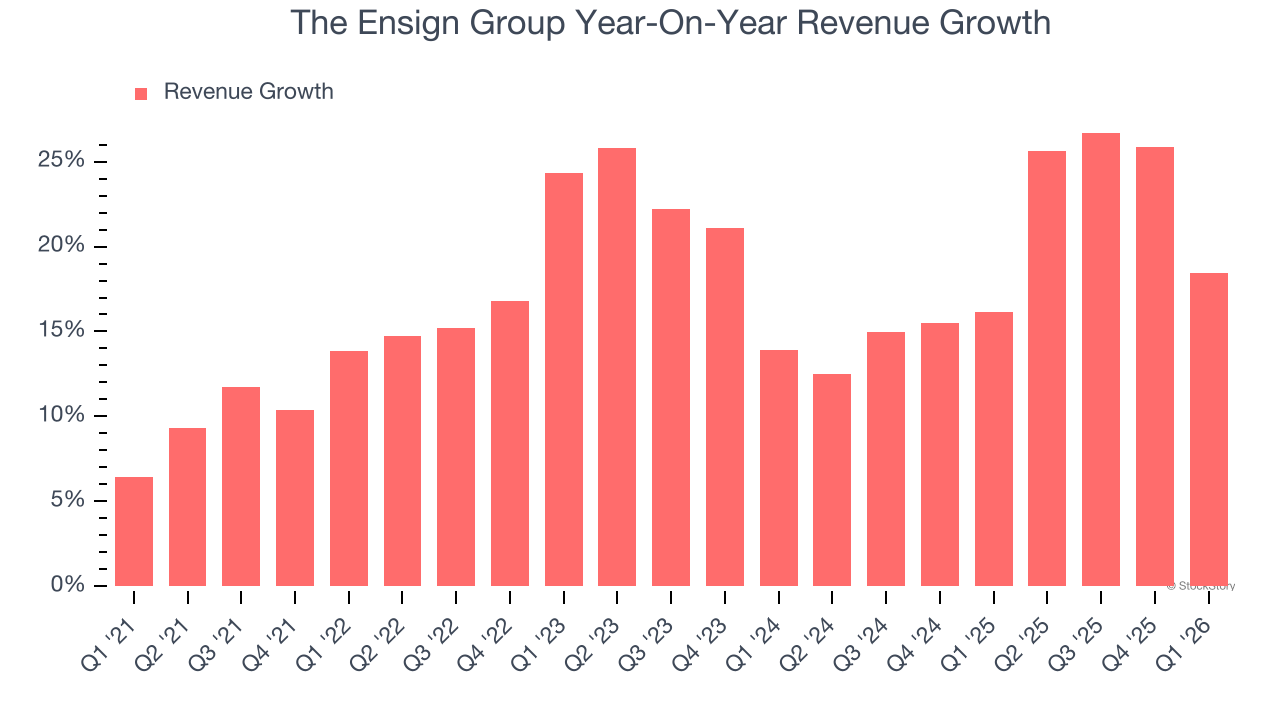

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, The Ensign Group’s 17.6% annualized revenue growth over the last five years was impressive. Its growth beat the average healthcare company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. The Ensign Group’s annualized revenue growth of 19.3% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

The Ensign Group also reports its number of units sold, which reached 348,389 in the latest quarter. Over the last two years, The Ensign Group’s units sold averaged 8.9% year-on-year declines. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, The Ensign Group’s revenue grew by 18.4% year on year to $1.39 billion but fell short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 16.7% over the next 12 months, a slight deceleration versus the last two years. Despite the slowdown, this projection is admirable and indicates the market is baking in success for its products and services.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Adjusted Operating Margin

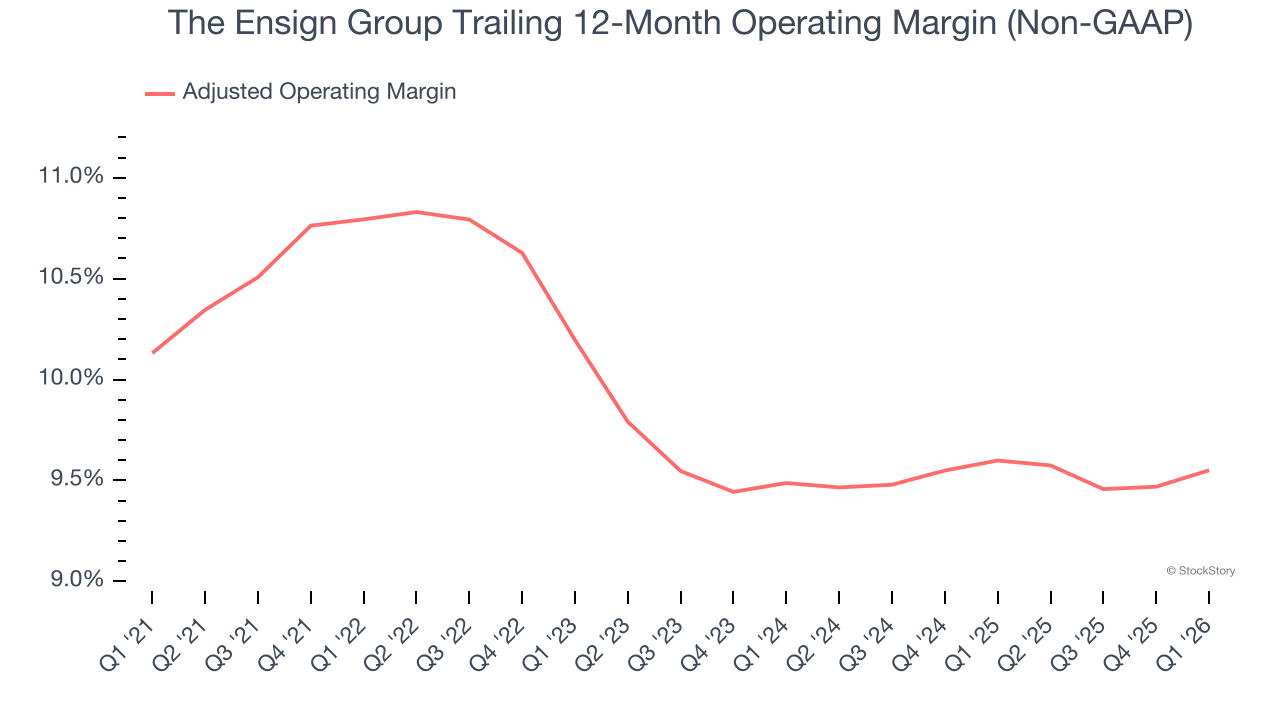

The Ensign Group was profitable over the last five years but held back by its large cost base. Its average adjusted operating margin of 9.8% was weak for a healthcare business.

Analyzing the trend in its profitability, The Ensign Group’s adjusted operating margin decreased by 1.2 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. The Ensign Group’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, The Ensign Group generated an adjusted operating margin profit margin of 10%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

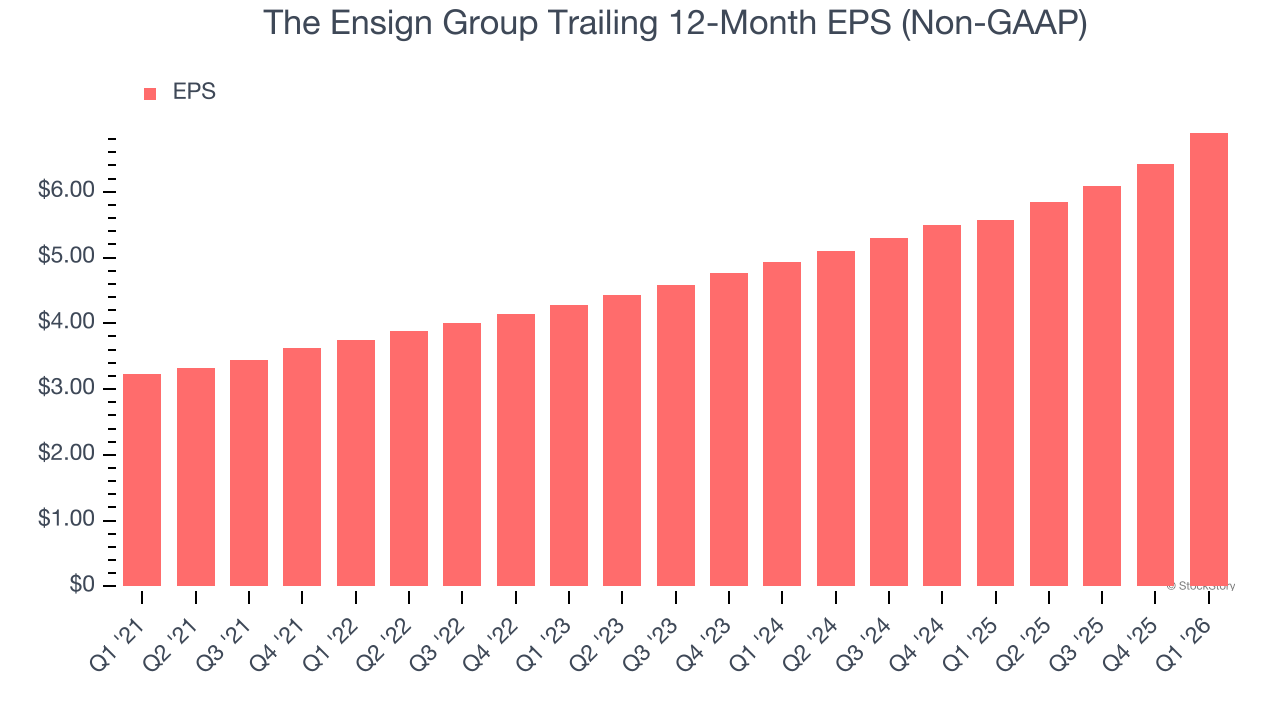

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

The Ensign Group’s astounding 16.4% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q1, The Ensign Group reported adjusted EPS of $1.85, up from $1.37 in the same quarter last year. This print beat analysts’ estimates by 1.8%. Over the next 12 months, Wall Street expects The Ensign Group’s full-year EPS of $6.90 to grow 11.6%.

Key Takeaways from The Ensign Group’s Q1 Results

It was good to see The Ensign Group provide full-year revenue guidance that slightly beat analysts’ expectations. On the other hand, its revenue missed. Overall, this was a softer quarter. The stock remained flat at $186.56 immediately following the results.

So should you invest in The Ensign Group right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).