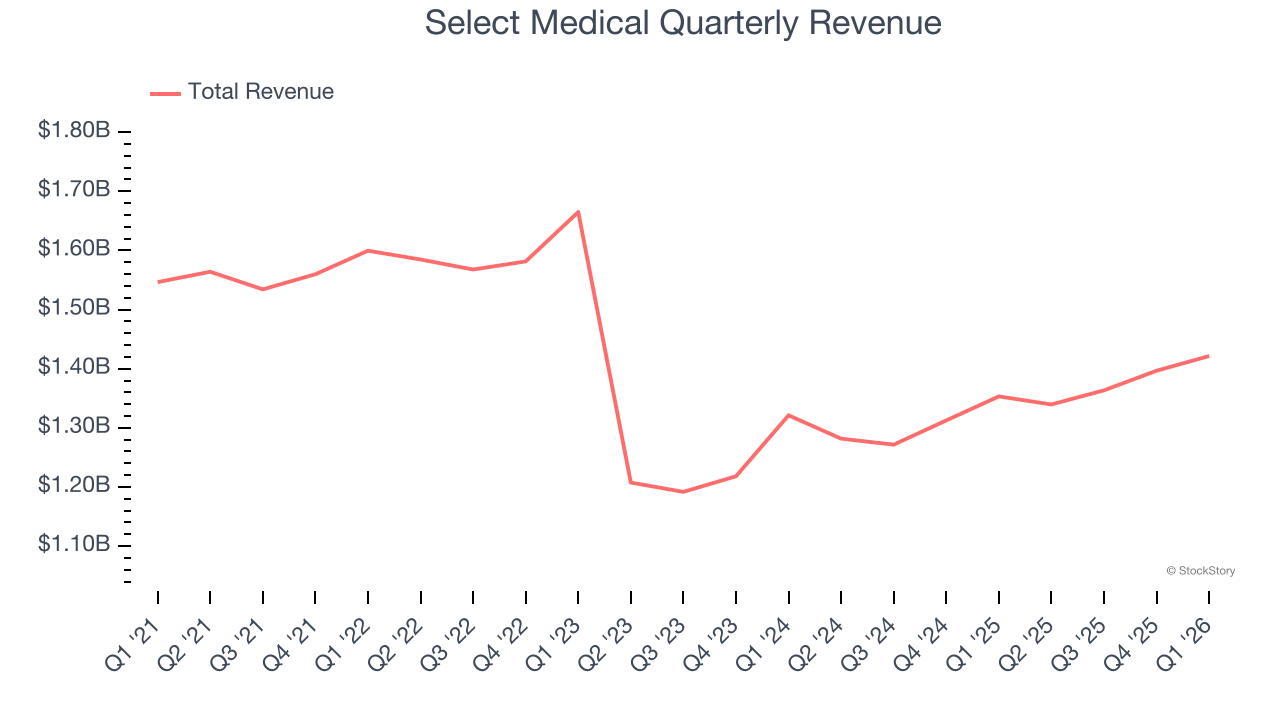

Healthcare services company Select Medical (NYSE: SEM) beat Wall Street’s revenue expectations in Q1 CY2026, with sales up 5% year on year to $1.42 billion. The company expects the full year’s revenue to be around $5.7 billion, close to analysts’ estimates. Its GAAP profit of $0.35 per share was 23.8% below analysts’ consensus estimates.

Is now the time to buy Select Medical? Find out by accessing our full research report, it’s free.

Select Medical (SEM) Q1 CY2026 Highlights:

- Revenue: $1.42 billion vs analyst estimates of $1.41 billion (5% year-on-year growth, 0.9% beat)

- EPS (GAAP): $0.35 vs analyst expectations of $0.46 (23.8% miss)

- Adjusted EBITDA: $141.6 million vs analyst estimates of $154.9 million (10% margin, 8.6% miss)

- The company reconfirmed its revenue guidance for the full year of $5.7 billion at the midpoint

- EPS (GAAP) guidance for the full year is $1.27 at the midpoint, roughly in line with what analysts were expecting

- EBITDA guidance for the full year is $530 million at the midpoint, in line with analyst expectations

- Operating Margin: 6.9%, down from 8.3% in the same quarter last year

- Free Cash Flow was -$21.04 million compared to -$55.8 million in the same quarter last year

- Sales Volumes rose 1% year on year (-1.9% in the same quarter last year)

- Market Capitalization: $2.05 billion

Company Overview

With a nationwide network spanning 46 states and over 2,700 healthcare facilities, Select Medical (NYSE: SEM) operates critical illness recovery hospitals, rehabilitation hospitals, outpatient rehabilitation clinics, and occupational health centers across the United States.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Select Medical struggled to consistently increase demand as its $5.52 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and is a sign of lacking business quality.

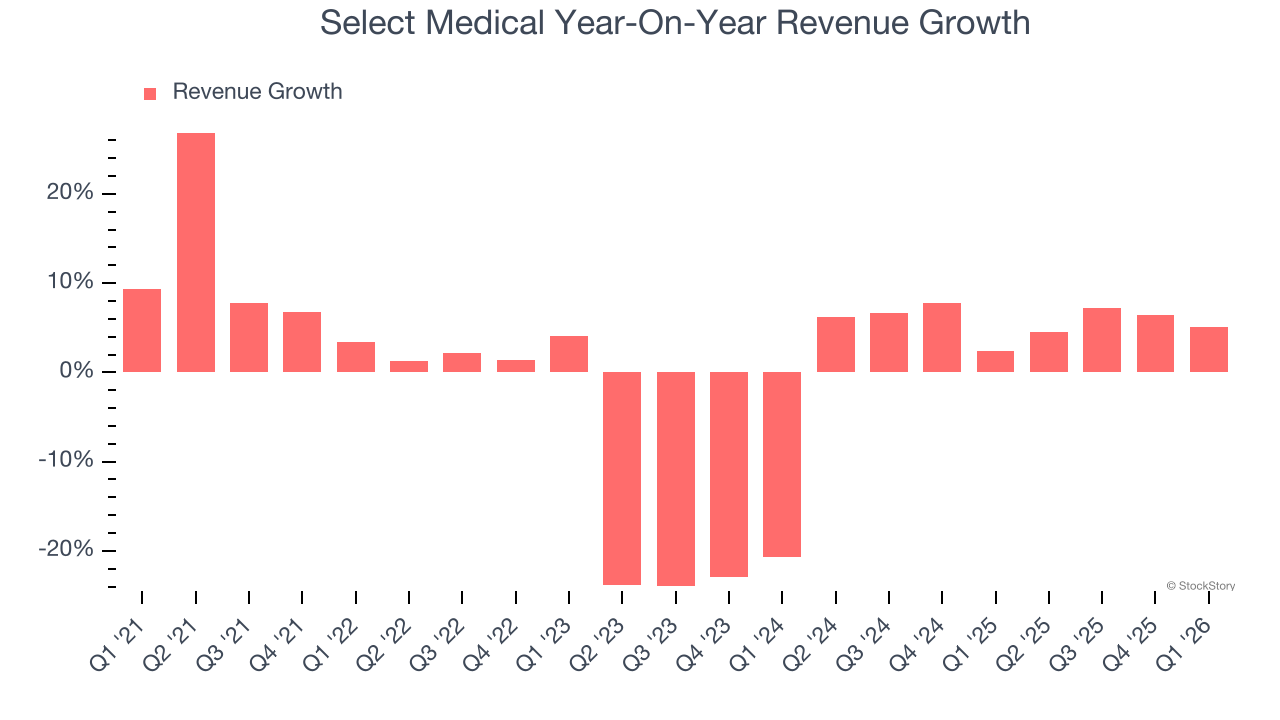

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Select Medical’s annualized revenue growth of 5.7% over the last two years is above its five-year trend, which is encouraging.

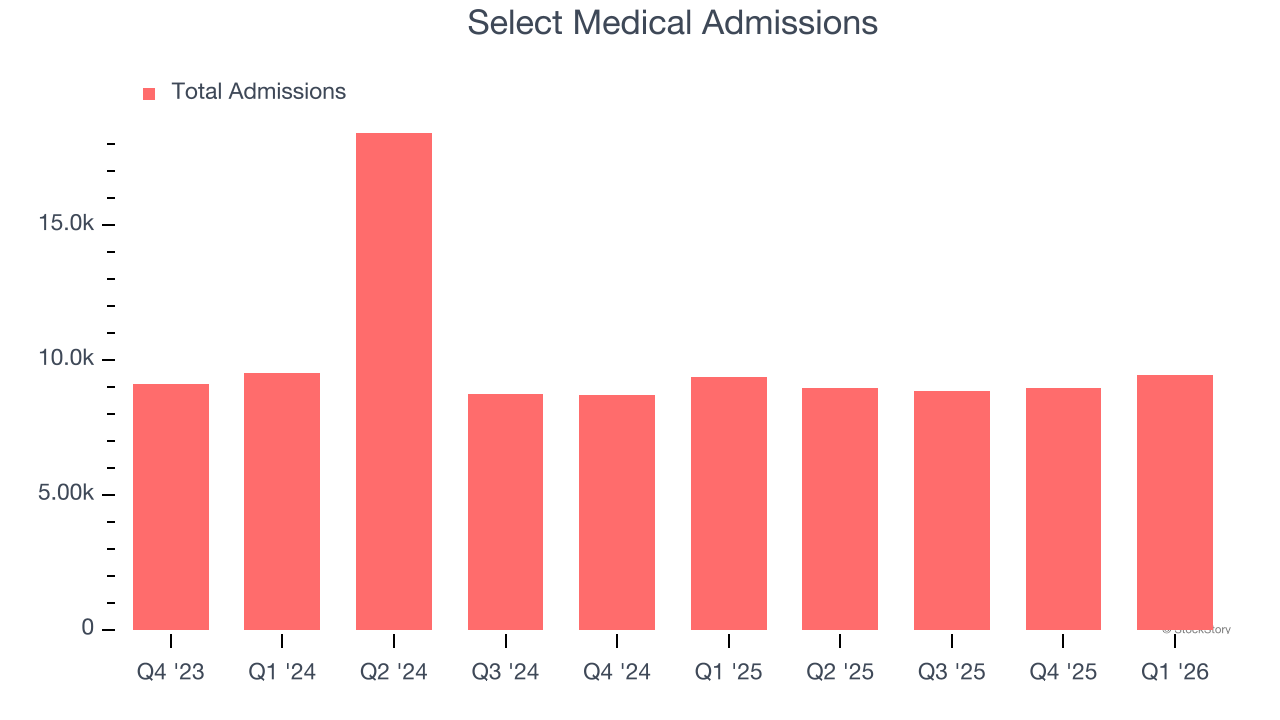

We can dig further into the company’s revenue dynamics by analyzing its number of admissions, which reached 9,449 in the latest quarter. Over the last two years, Select Medical’s admissions averaged 8.8% year-on-year declines. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, Select Medical reported year-on-year revenue growth of 5%, and its $1.42 billion of revenue exceeded Wall Street’s estimates by 0.9%.

Looking ahead, sell-side analysts expect revenue to grow 4.4% over the next 12 months, similar to its two-year rate. This projection is underwhelming and suggests its products and services will see some demand headwinds.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Adjusted Operating Margin

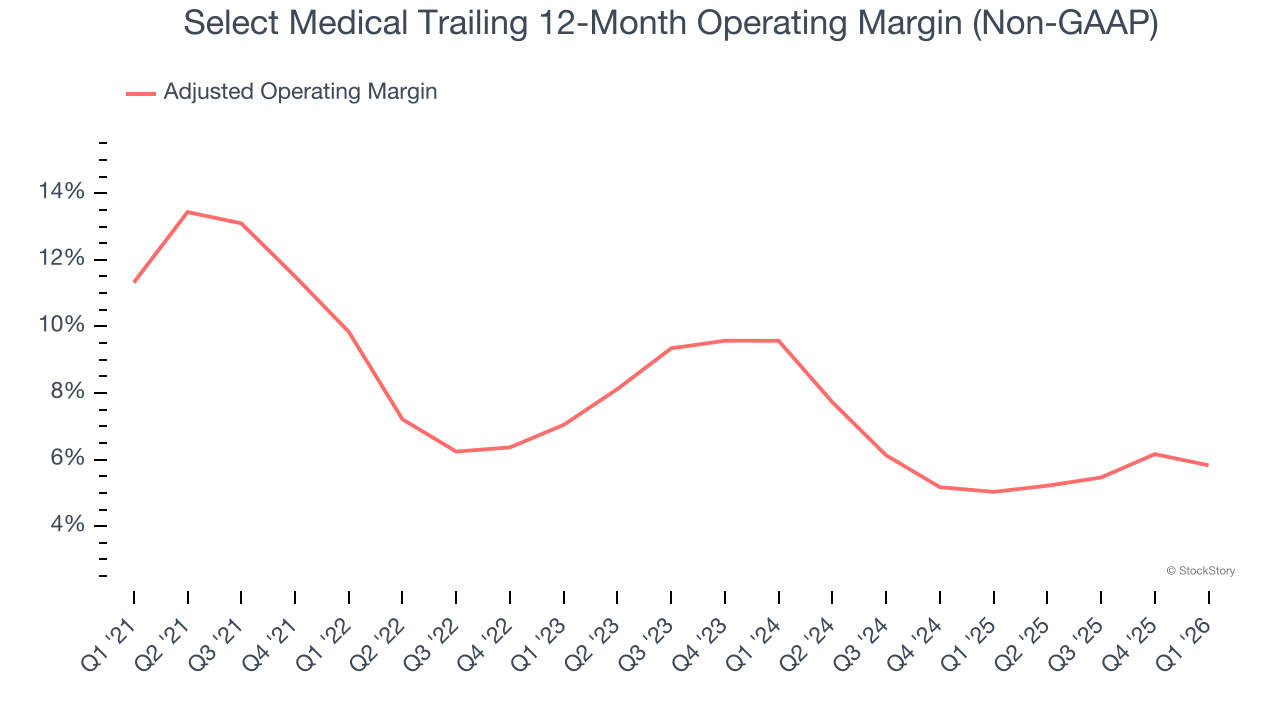

Select Medical was profitable over the last five years but held back by its large cost base. Its average adjusted operating margin of 7.5% was weak for a healthcare business.

Analyzing the trend in its profitability, Select Medical’s adjusted operating margin decreased by 4 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 3.7 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q1, Select Medical generated an adjusted operating margin profit margin of 6.9%, down 1.4 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

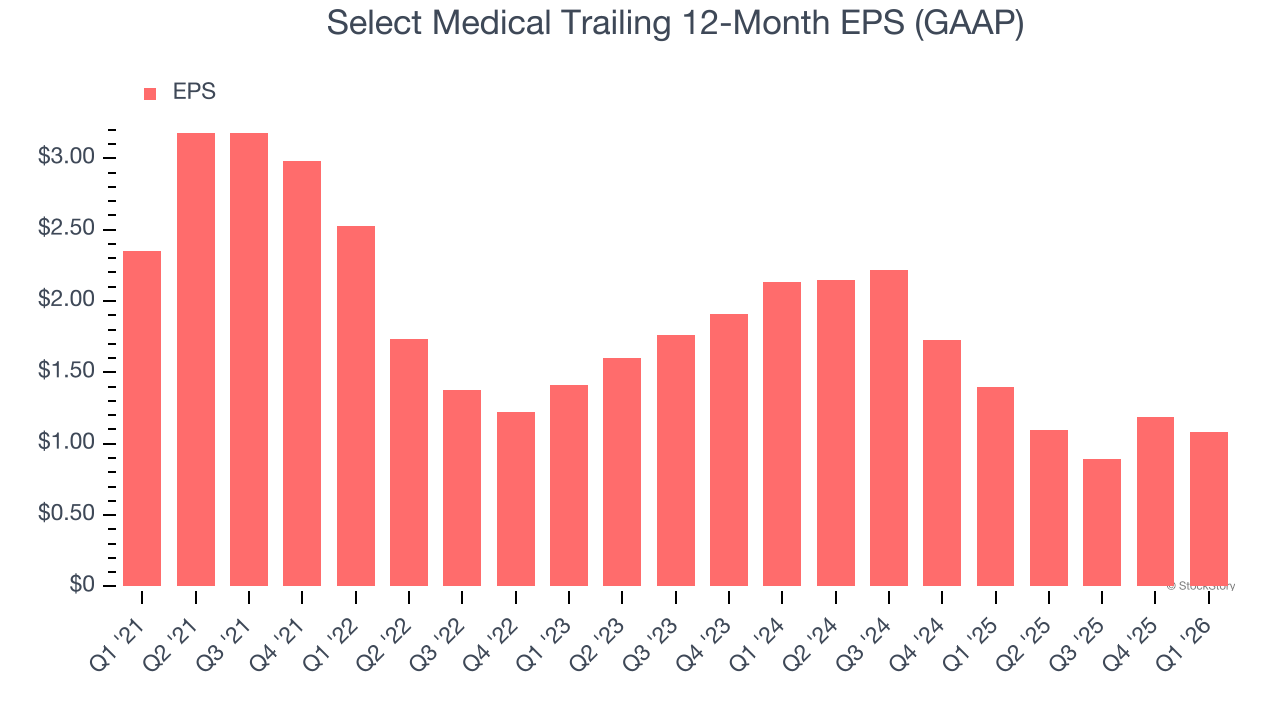

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Select Medical, its EPS declined by 14.3% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

Diving into the nuances of Select Medical’s earnings can give us a better understanding of its performance. As we mentioned earlier, Select Medical’s adjusted operating margin declined by 4 percentage points over the last five years. Its share count also grew by 39.8%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q1, Select Medical reported EPS of $0.35, down from $0.45 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Select Medical’s full-year EPS of $1.09 to grow 22.7%.

Key Takeaways from Select Medical’s Q1 Results

It was good to see Select Medical narrowly top analysts’ revenue expectations this quarter. On the other hand, its EPS missed and its full-year EPS guidance was just in line with Wall Street’s estimates. Overall, this quarter was mixed. The stock remained flat at $16.43 immediately following the results.

So do we think Select Medical is an attractive buy at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).