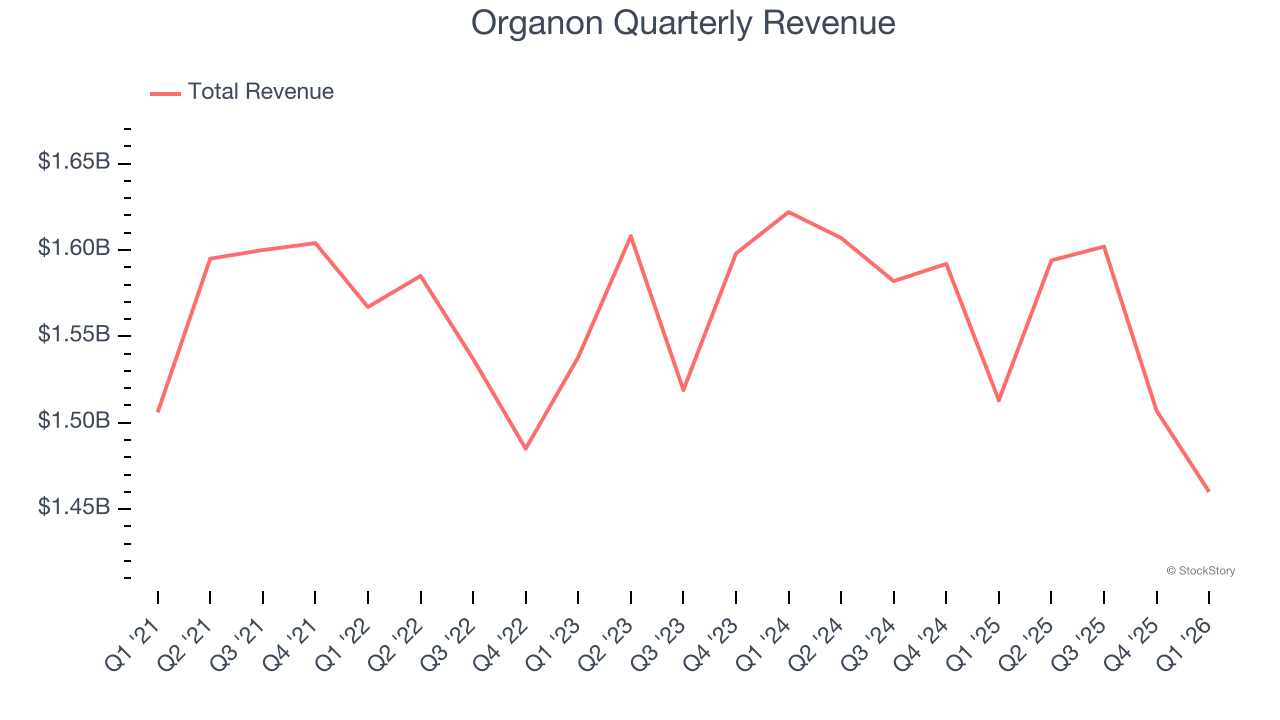

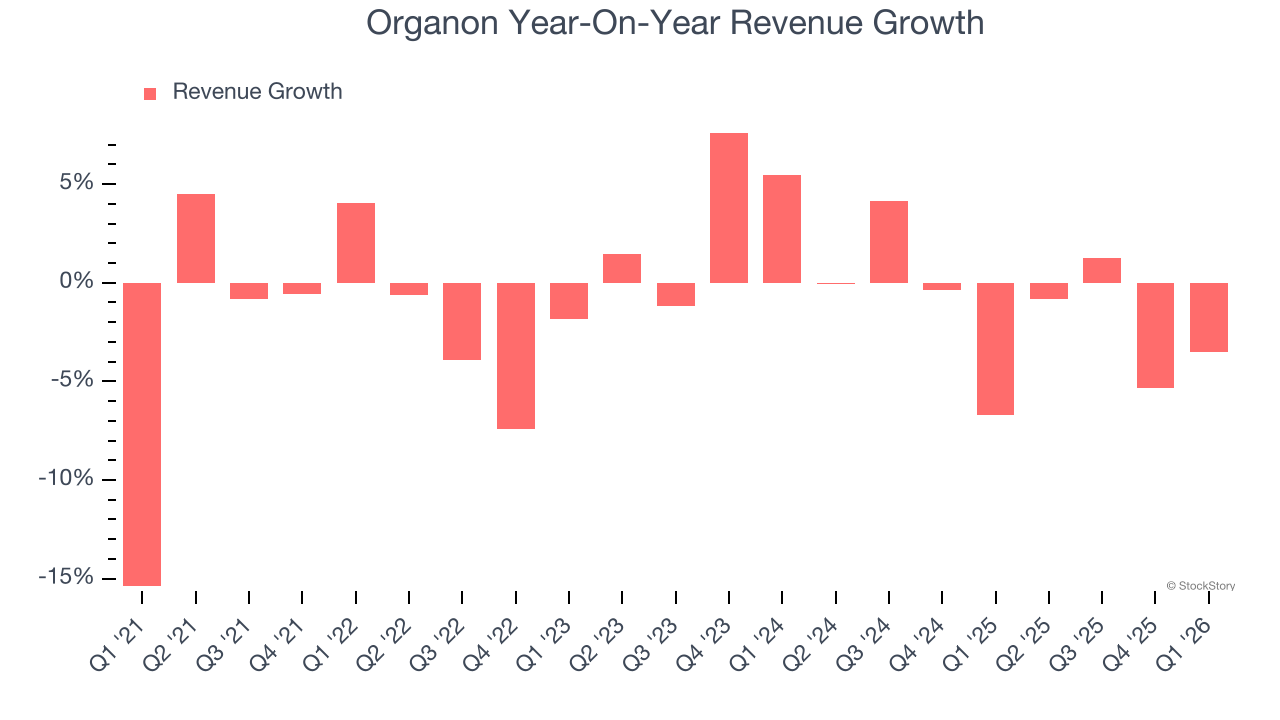

Pharmaceutical company Organon (NYSE: OGN) missed Wall Street’s revenue expectations in Q1 CY2026, with sales falling 3.5% year on year to $1.46 billion. Its non-GAAP profit of $0.71 per share was 16.8% below analysts’ consensus estimates.

Is now the time to buy Organon? Find out by accessing our full research report, it’s free.

Organon (OGN) Q1 CY2026 Highlights:

- Revenue: $1.46 billion vs analyst estimates of $1.47 billion (3.5% year-on-year decline, 0.7% miss)

- Adjusted EPS: $0.71 vs analyst expectations of $0.85 (16.8% miss)

- Adjusted EBITDA: $415 million vs analyst estimates of $422.5 million (28.4% margin, 1.8% miss)

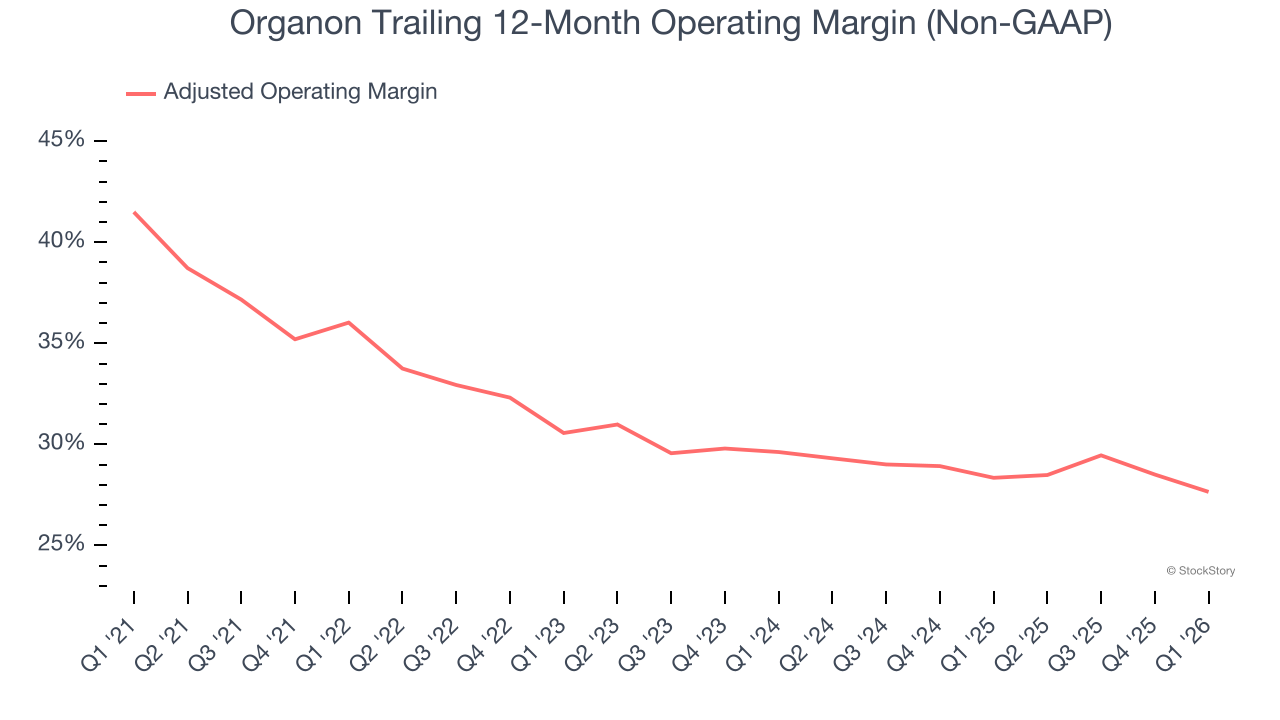

- Operating Margin: 18.2%, up from 15.4% in the same quarter last year

- Market Capitalization: $3.5 billion

Company Overview

Spun off from Merck in 2021 to create a company dedicated to addressing unmet needs in women's health, Organon (NYSE: OGN) is a global healthcare company focused on improving women's health through prescription therapies, medical devices, biosimilars, and established medicines.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Organon struggled to consistently increase demand as its $6.16 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and is a sign of lacking business quality.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Organon’s recent performance shows its demand remained suppressed as its revenue has declined by 1.5% annually over the last two years.

This quarter, Organon missed Wall Street’s estimates and reported a rather uninspiring 3.5% year-on-year revenue decline, generating $1.46 billion of revenue.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection indicates its newer products and services will spur better top-line performance, it is still below the sector average.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Adjusted Operating Margin

Organon has been a well-oiled machine over the last five years. It demonstrated elite profitability for a healthcare business, boasting an average adjusted operating margin of 30.5%.

Analyzing the trend in its profitability, Organon’s adjusted operating margin decreased by 8.4 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 2 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Organon generated an adjusted operating margin profit margin of 25.8%, down 3.6 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

Earnings Per Share

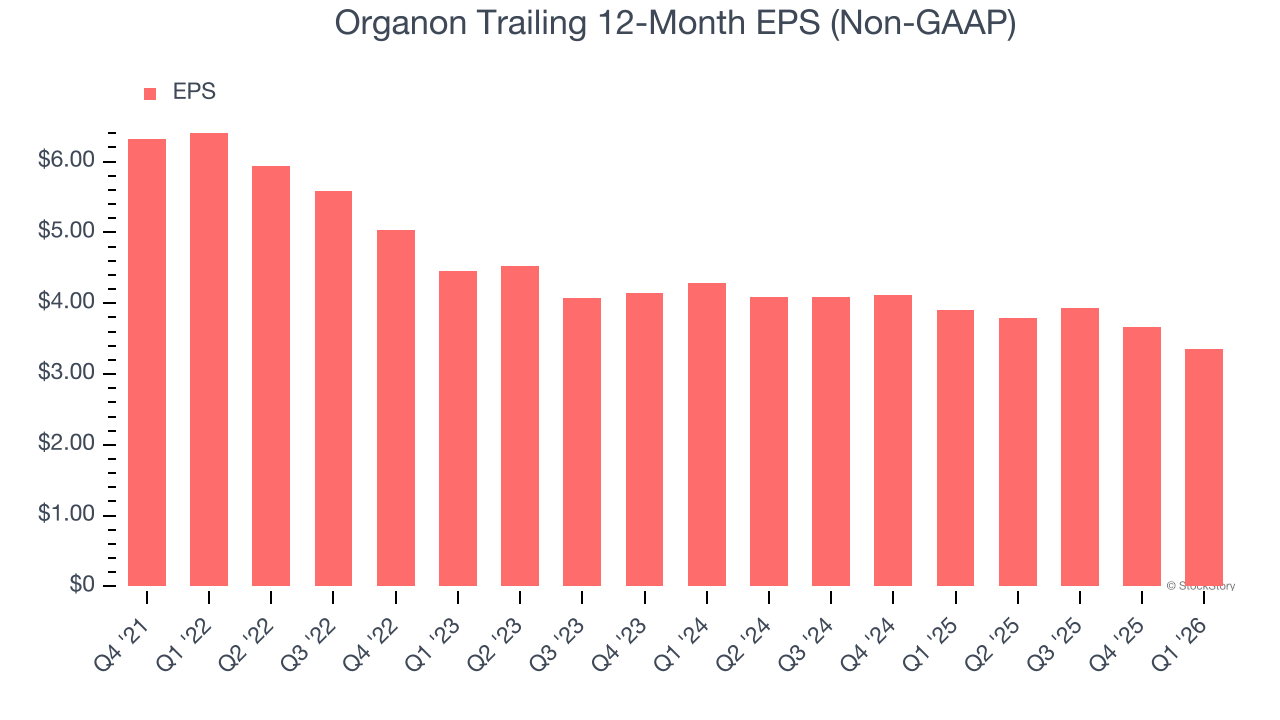

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Organon’s full-year EPS dropped 74.7%, or 15% annually, over the last four years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Organon’s low margin of safety could leave its stock price susceptible to large downswings.

In Q1, Organon reported adjusted EPS of $0.71, down from $1.02 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Organon’s full-year EPS of $3.35 to grow 3.2%.

Key Takeaways from Organon’s Q1 Results

We struggled to find many positives in these results. Its EPS missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $13.17 immediately following the results.

Organon’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).