Automotive parts company LKQ (NASDAQ: LKQ) beat Wall Street’s revenue expectations in Q1 CY2026, but sales were flat year on year at $3.47 billion. Its non-GAAP profit of $0.67 per share was in line with analysts’ consensus estimates.

Is now the time to buy LKQ? Find out by accessing our full research report, it’s free.

LKQ (LKQ) Q1 CY2026 Highlights:

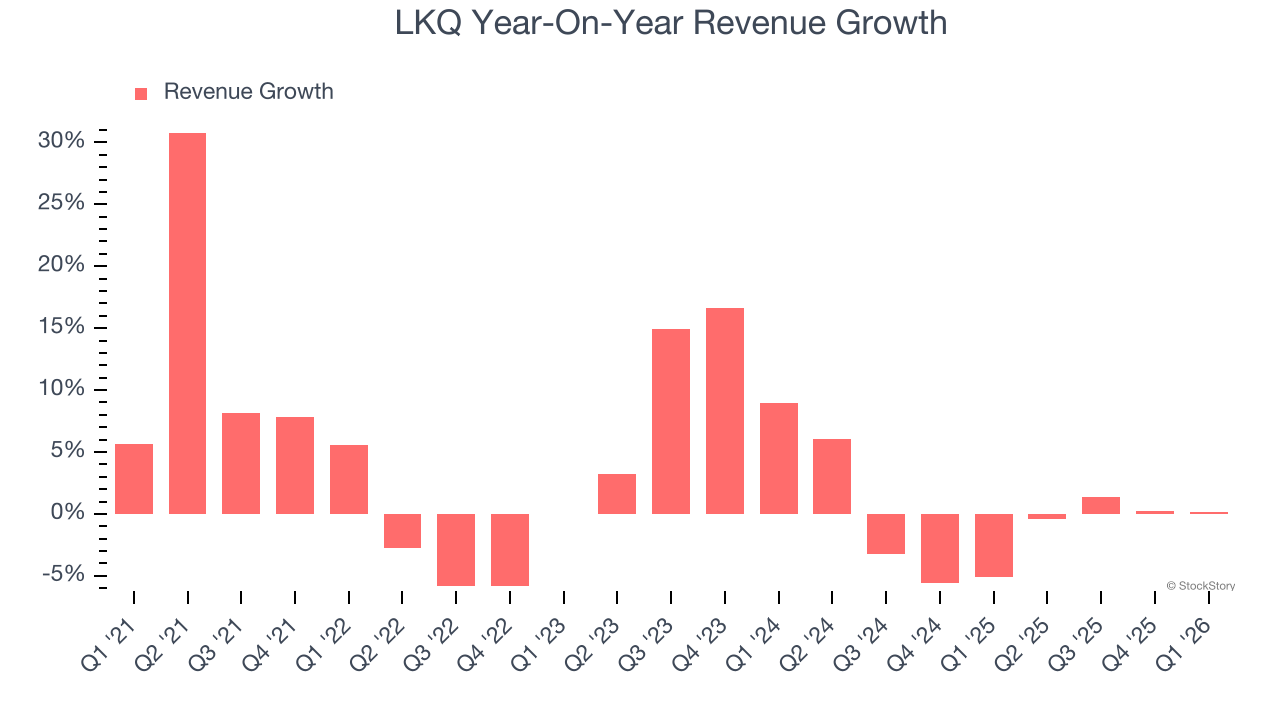

- Revenue: $3.47 billion vs analyst estimates of $3.38 billion (flat year on year, 2.5% beat)

- Adjusted EPS: $0.67 vs analyst estimates of $0.67 (in line)

- Adjusted EBITDA: $347 million vs analyst estimates of $348.8 million (10% margin, 0.5% miss)

- Management reiterated its full-year Adjusted EPS guidance of $3.05 at the midpoint

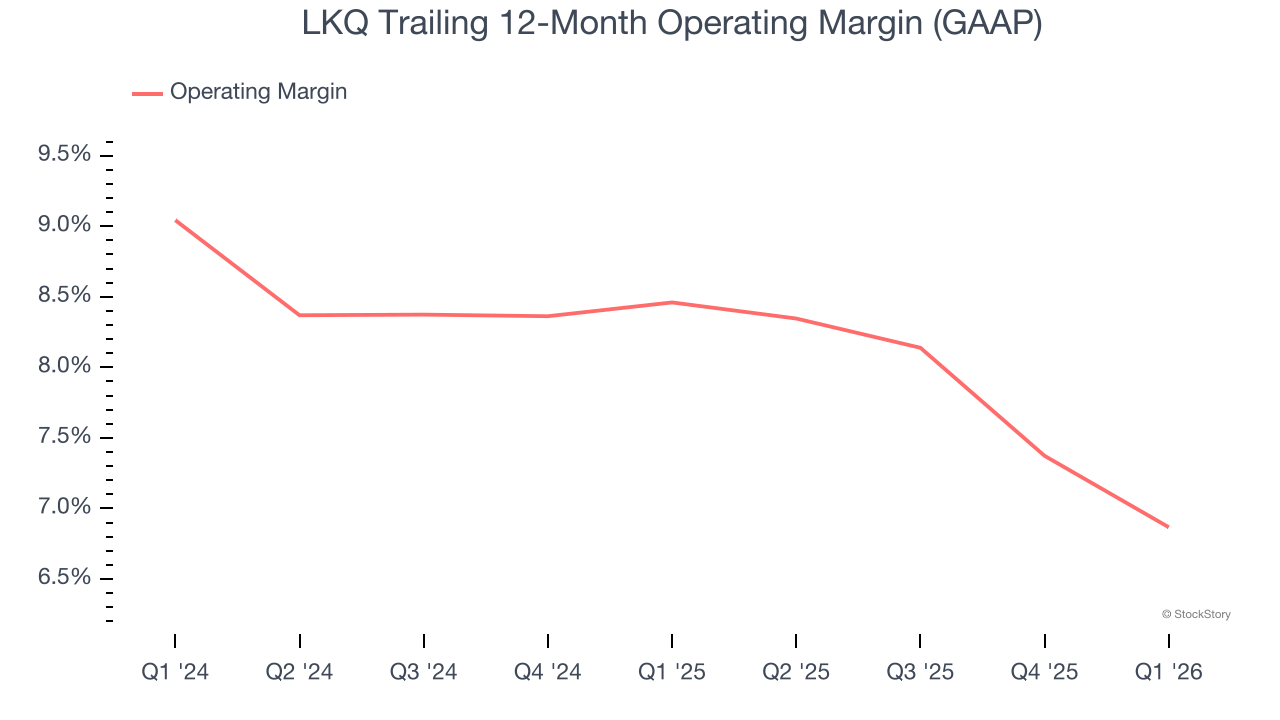

- Operating Margin: 6.3%, down from 8.3% in the same quarter last year

- Free Cash Flow was -$96 million compared to -$57 million in the same quarter last year

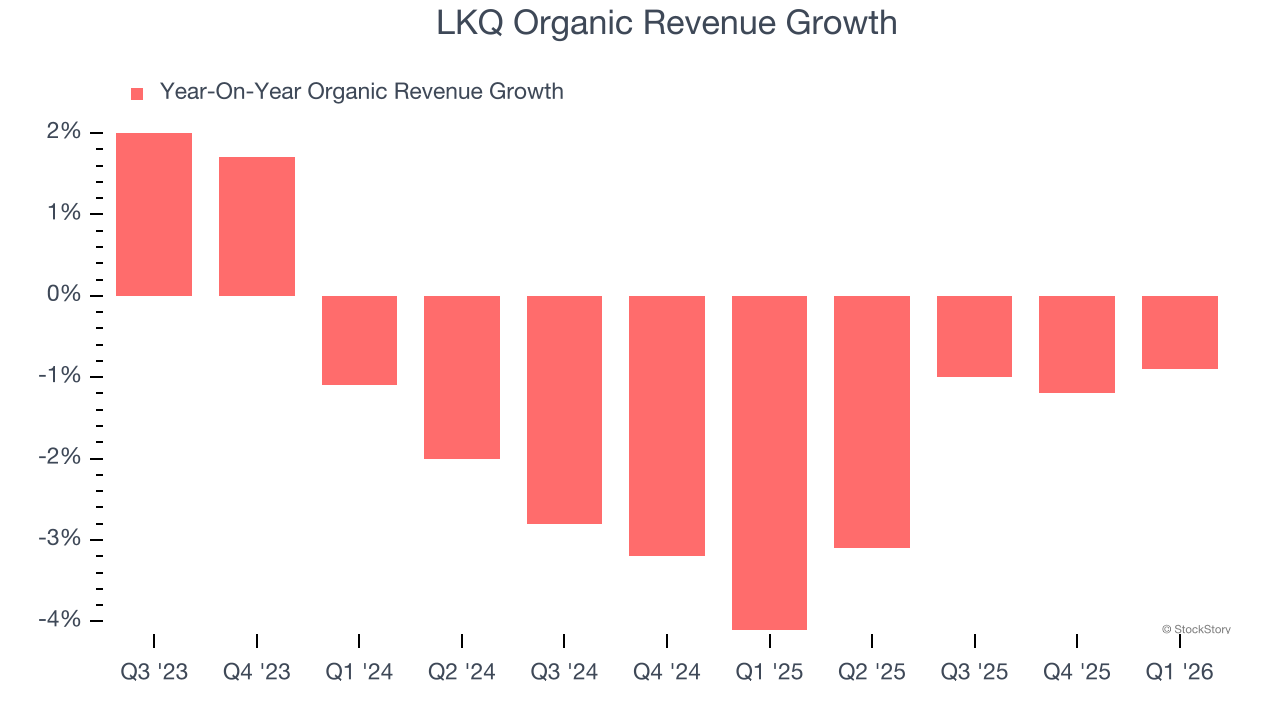

- Organic Revenue was flat year on year (beat)

- Market Capitalization: $7.82 billion

“We are operating in a challenging environment and are focused on improving our results. Our teams are taking deliberate actions to reduce costs, streamline operations while taking market share, and position ourselves for success going forward as the environment improves. In North America, our business held up well in the quarter with above market growth, and we’re starting to see signs of recovery in the market. In Europe, we saw continual improvements through the quarter, and we’re continuing to work on integration. In early April, we took a large step forward with an ERP migration in a major market that is part of our overall operational improvement initiatives. But there is more work to do. We are operating with urgency and focused on execution, improving our customer relationships, and strengthening the business to create value for our shareholders,” commented Justin Jude, President and Chief Executive Officer.

Company Overview

A global distributor of vehicle parts and accessories, LKQ (NASDAQ: LKQ) offers its customers a comprehensive selection of high-quality, affordably priced automobile products.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, LKQ’s 3.4% annualized revenue growth over the last five years was weak. This was below our standard for the consumer discretionary sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. LKQ’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, LKQ’s organic revenue averaged 2.3% year-on-year declines. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, LKQ’s $3.47 billion of revenue was flat year on year but beat Wall Street’s estimates by 2.5%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection implies its newer products and services will spur better top-line performance, it is still below average for the sector.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

LKQ’s operating margin has been trending down over the last 12 months and averaged 7.7% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

In Q1, LKQ generated an operating margin profit margin of 6.3%, down 2 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

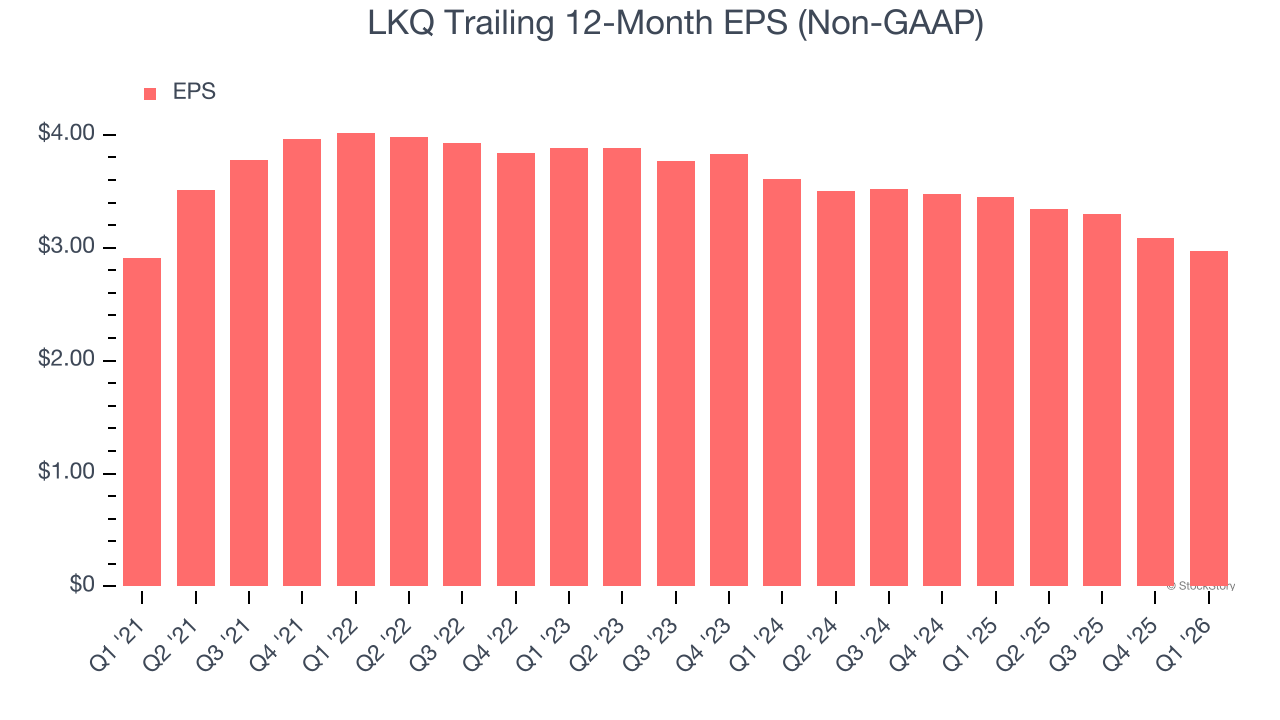

LKQ’s flat EPS over the last five years was below its 3.4% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

In Q1, LKQ reported adjusted EPS of $0.67, down from $0.79 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects LKQ’s full-year EPS of $2.97 to grow 4.3%.

Key Takeaways from LKQ’s Q1 Results

It was encouraging to see LKQ beat analysts’ organic revenue and reported revenue expectations this quarter. We were also happy its organic revenue narrowly outperformed Wall Street’s estimates. On the other hand, its operating income missed and EPS was just in line. Zooming out, we think this was a mixed quarter. The stock remained flat at $30.84 immediately following the results.

So should you invest in LKQ right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).