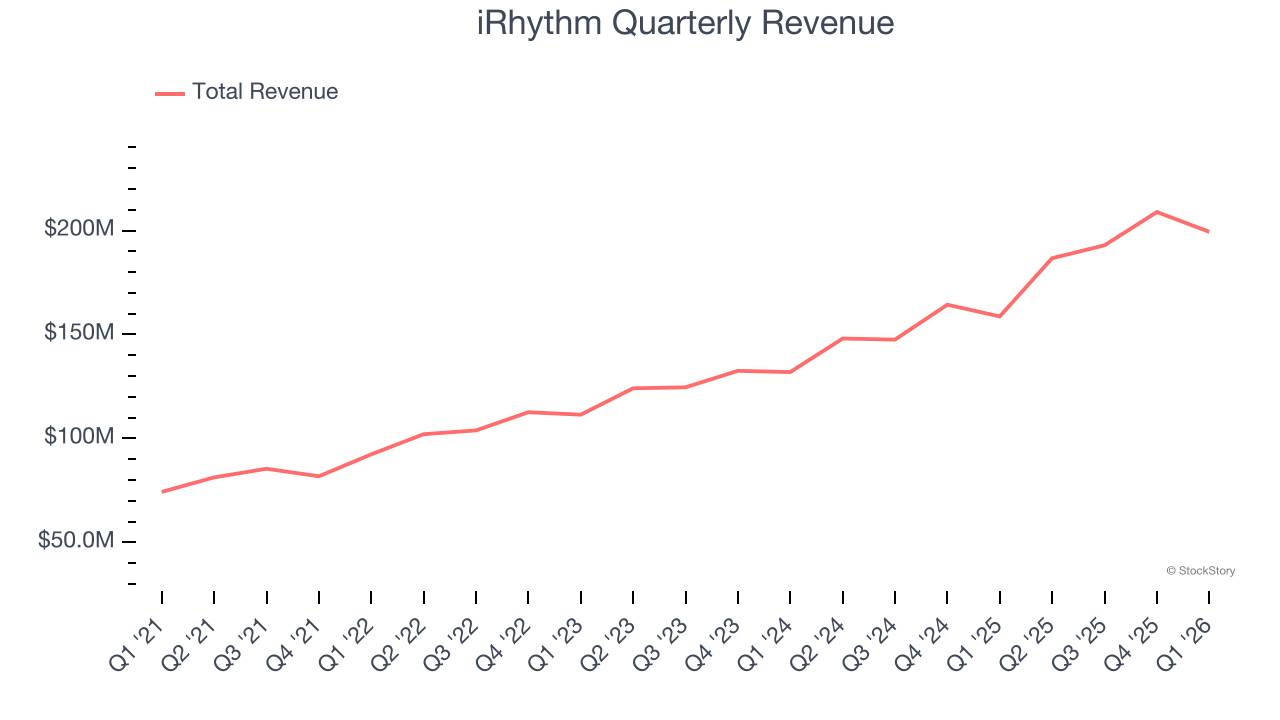

Medical technology company iRhythm Technologies (NASDAQ: IRTC) announced better-than-expected revenue in Q1 CY2026, with sales up 25.7% year on year to $199.4 million. The company expects the full year’s revenue to be around $880 million, close to analysts’ estimates. Its non-GAAP loss of $0.35 per share was 45.3% above analysts’ consensus estimates.

Is now the time to buy iRhythm? Find out by accessing our full research report, it’s free.

iRhythm (IRTC) Q1 CY2026 Highlights:

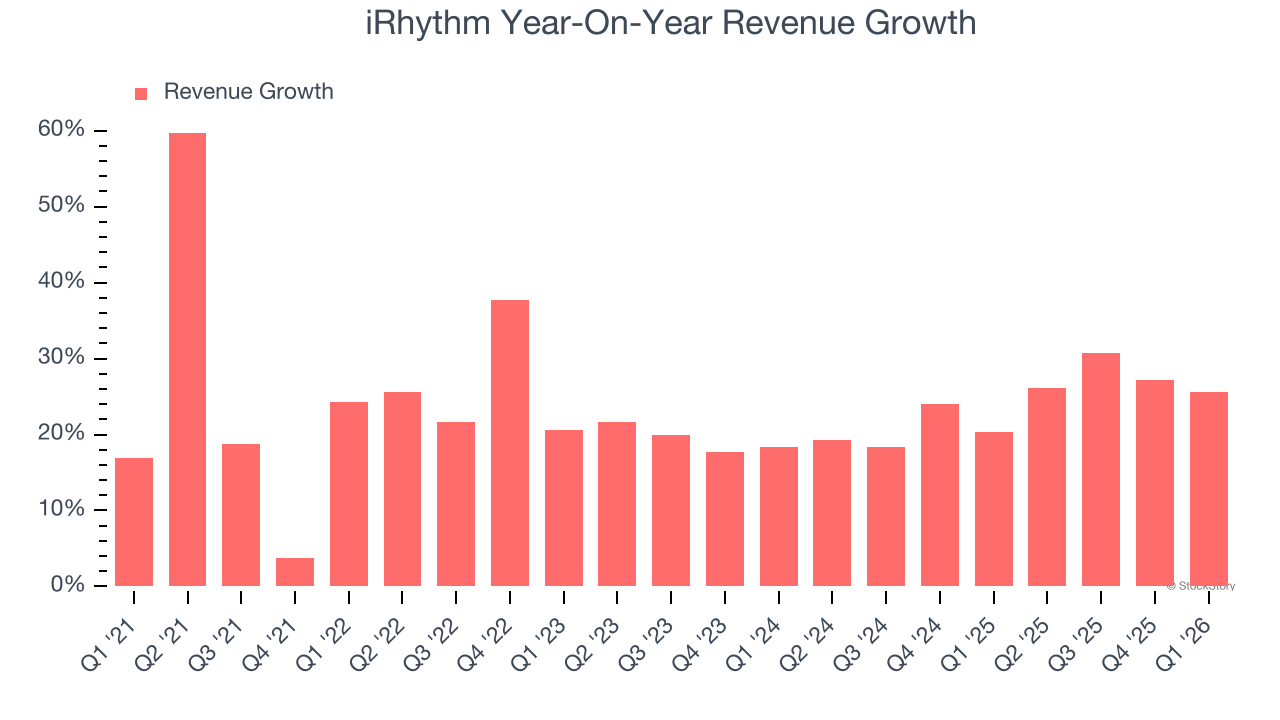

- Revenue: $199.4 million vs analyst estimates of $194 million (25.7% year-on-year growth, 2.8% beat)

- Adjusted EPS: -$0.35 vs analyst estimates of -$0.64 (45.3% beat)

- Adjusted EBITDA: $14.1 million vs analyst estimates of $6.88 million (7.1% margin, significant beat)

- The company slightly lifted its revenue guidance for the full year to $880 million at the midpoint from $875 million

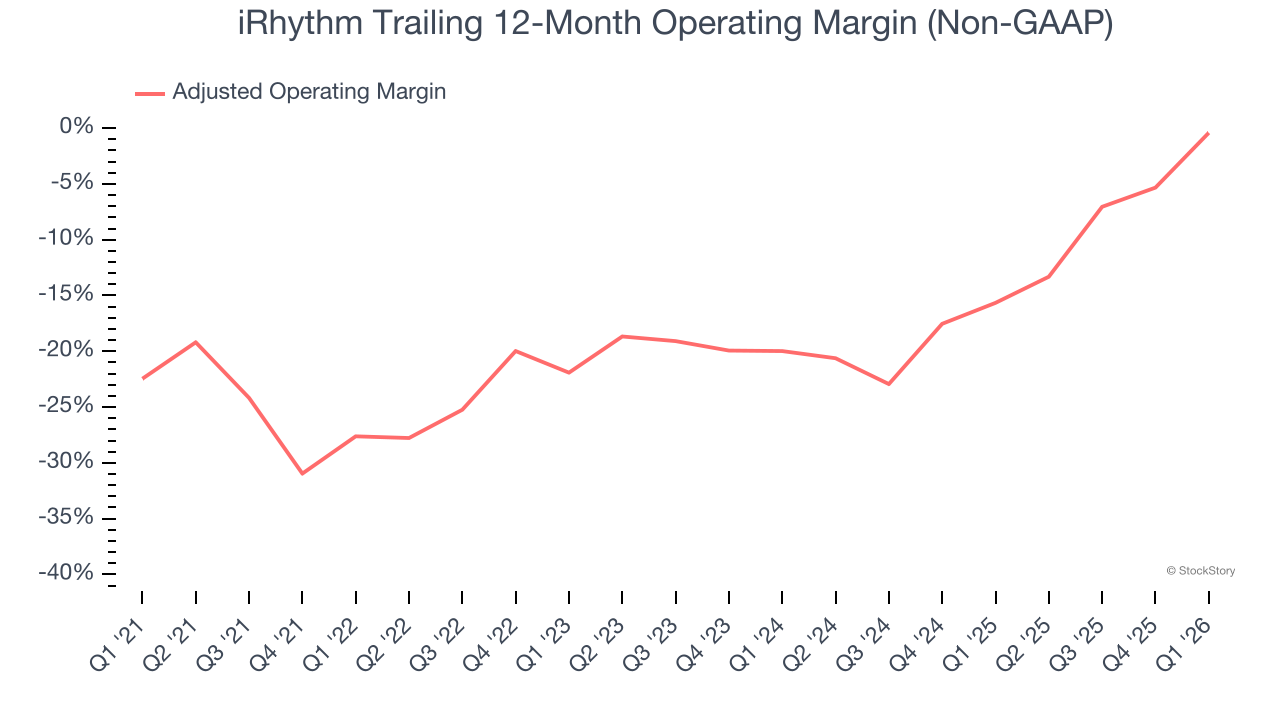

- Operating Margin: -8.1%, up from -20.5% in the same quarter last year

- Market Capitalization: $3.94 billion

Company Overview

Pioneering the shift from bulky, short-term heart monitors to sleek, wire-free patches, iRhythm Technologies (NASDAQ: IRTC) provides wearable cardiac monitoring devices and AI-powered analysis services that help physicians detect and diagnose heart rhythm disorders.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, iRhythm grew its sales at an excellent 23.3% compounded annual growth rate. Its growth beat the average healthcare company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. iRhythm’s annualized revenue growth of 23.9% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

This quarter, iRhythm reported robust year-on-year revenue growth of 25.7%, and its $199.4 million of revenue topped Wall Street estimates by 2.8%.

Looking ahead, sell-side analysts expect revenue to grow 15.3% over the next 12 months, a deceleration versus the last two years. Still, this projection is healthy and suggests the market sees success for its products and services.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Adjusted Operating Margin

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

Although iRhythm was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average adjusted operating margin of negative 14.5% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, iRhythm’s adjusted operating margin rose by 27.2 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 19.6 percentage points on a two-year basis. These data points are very encouraging and show momentum is on its side.

This quarter, iRhythm generated an adjusted operating margin profit margin of 2.7%, up 22.3 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

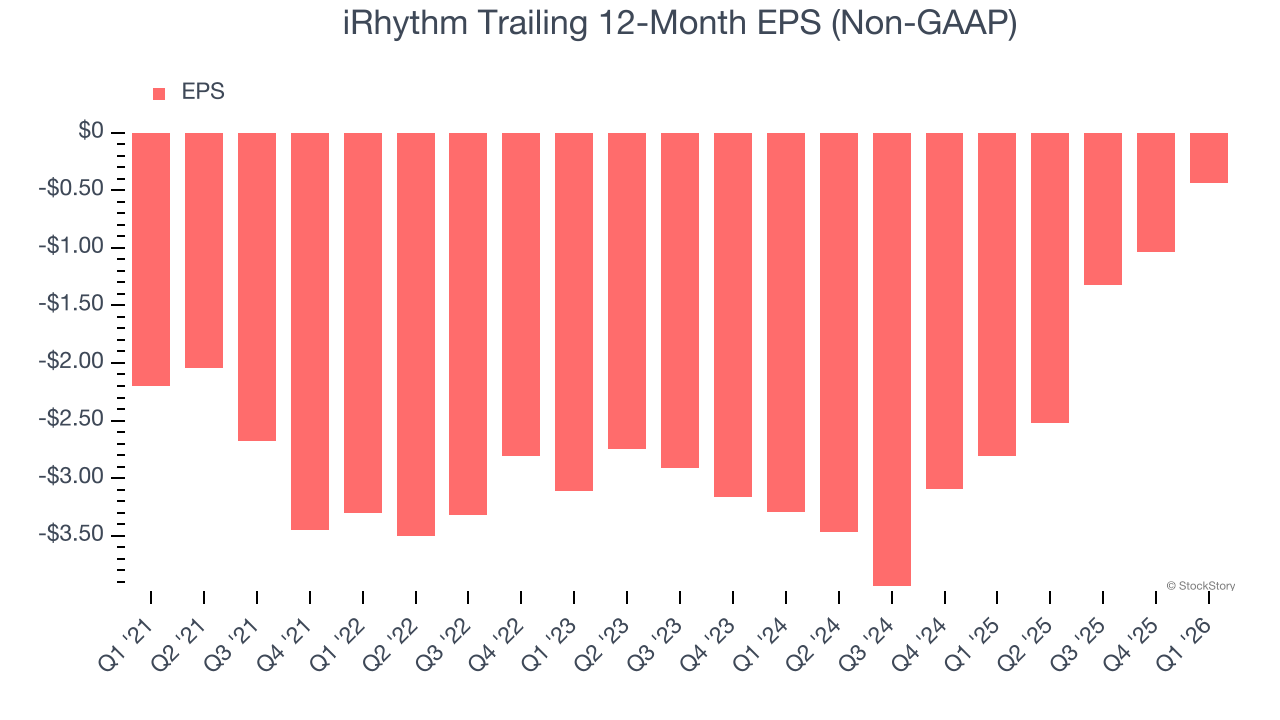

Although iRhythm’s full-year earnings are still negative, it reduced its losses and improved its EPS by 27.5% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

In Q1, iRhythm reported adjusted EPS of negative $0.35, up from negative $0.95 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street is optimistic. Analysts forecast iRhythm’s full-year EPS of negative $0.44 will flip to positive $0.32.

Key Takeaways from iRhythm’s Q1 Results

It was good to see iRhythm beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 2.9% to $132.96 immediately following the results.

Sure, iRhythm had a solid quarter, but if we look at the bigger picture, is this stock a buy? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).