Strategic Education trades at $81.32 and has moved in lockstep with the market. Its shares have returned 8.7% over the last six months while the S&P 500 has gained 9.8%.

Is now the time to buy Strategic Education, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Strategic Education Will Underperform?

We don't have much confidence in Strategic Education. Here are three reasons we avoid STRA and a stock we'd rather own.

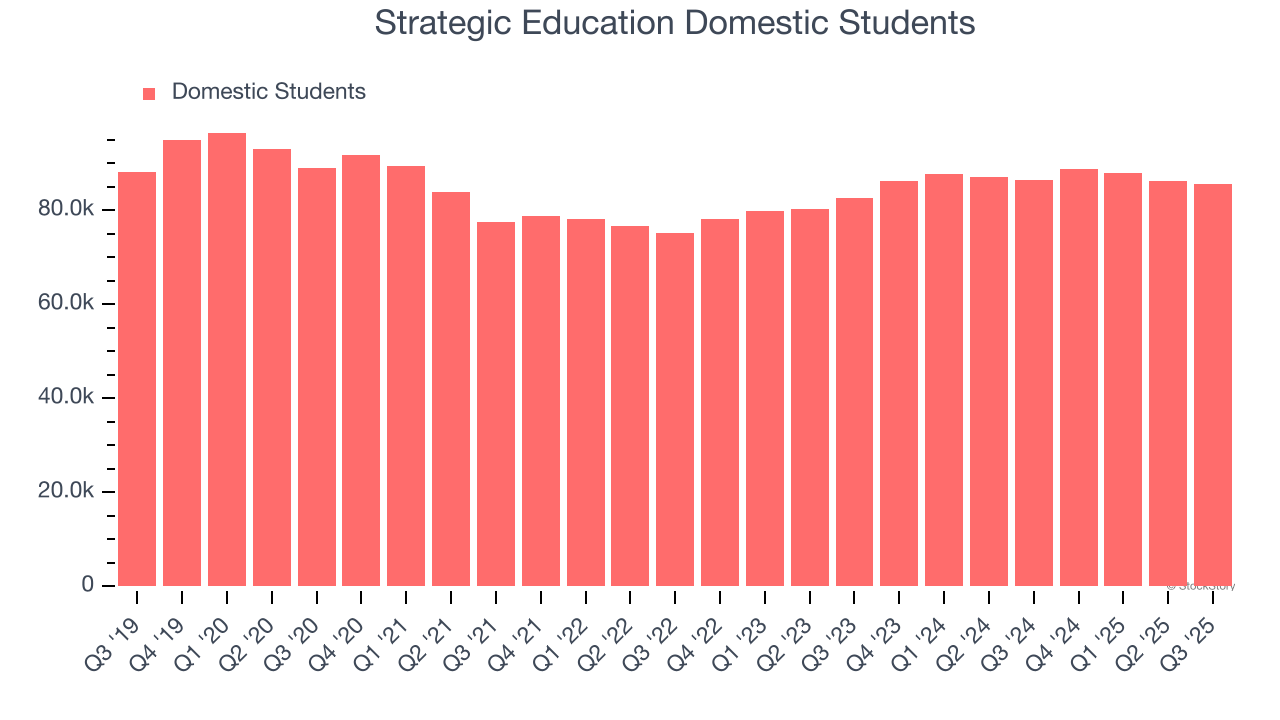

1. Weak Growth in Domestic Students Points to Soft Demand

Revenue growth can be broken down into changes in price and volume (for companies like Strategic Education, our preferred volume metric is domestic students). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Strategic Education’s domestic students came in at 85,640 in the latest quarter, and over the last two years, averaged 4.3% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

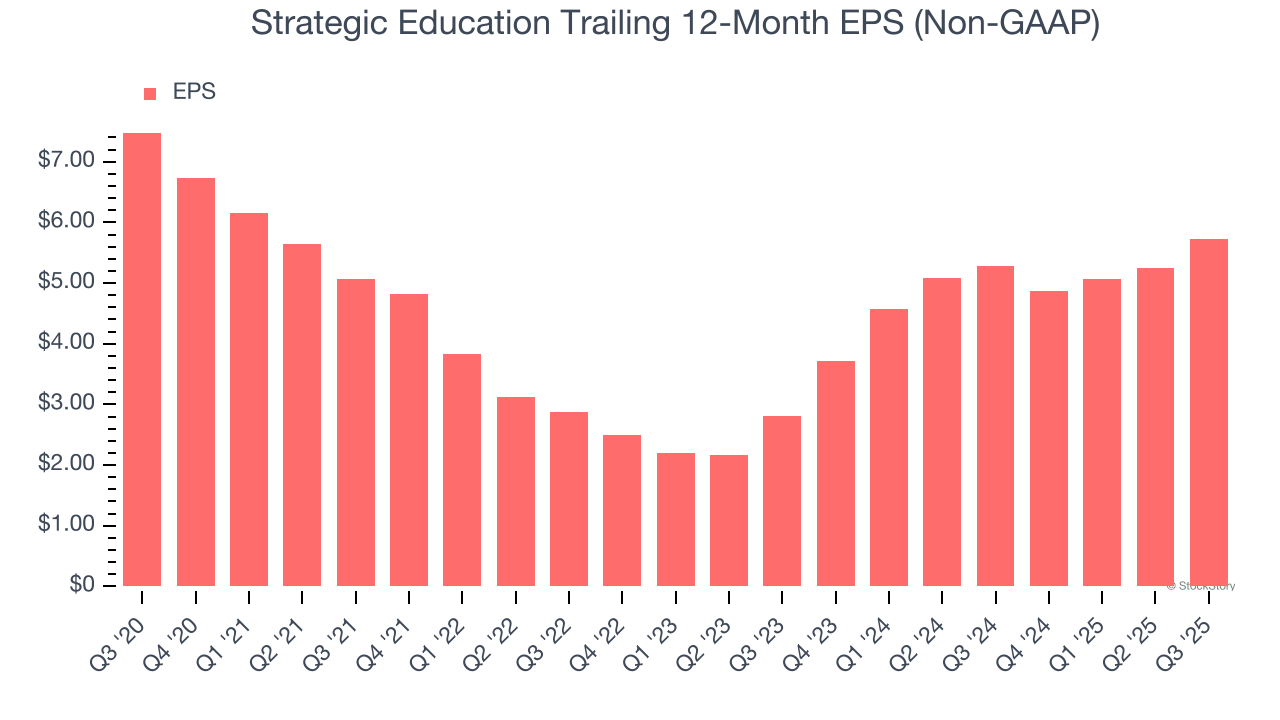

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Strategic Education, its EPS declined by 5.2% annually over the last five years while its revenue grew by 4.2%. This tells us the company became less profitable on a per-share basis as it expanded.

3. Free Cash Flow Projections Disappoint

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Over the next year, analysts’ consensus estimates show they’re expecting Strategic Education’s free cash flow margin of 10.5% for the last 12 months to remain the same.

Final Judgment

Strategic Education falls short of our quality standards. That said, the stock currently trades at 12.9× forward P/E (or $81.32 per share). While this valuation is reasonable, we don’t see a big opportunity at the moment. There are superior stocks to buy right now. We’d recommend looking at a top digital advertising platform riding the creator economy.

Stocks We Like More Than Strategic Education

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.