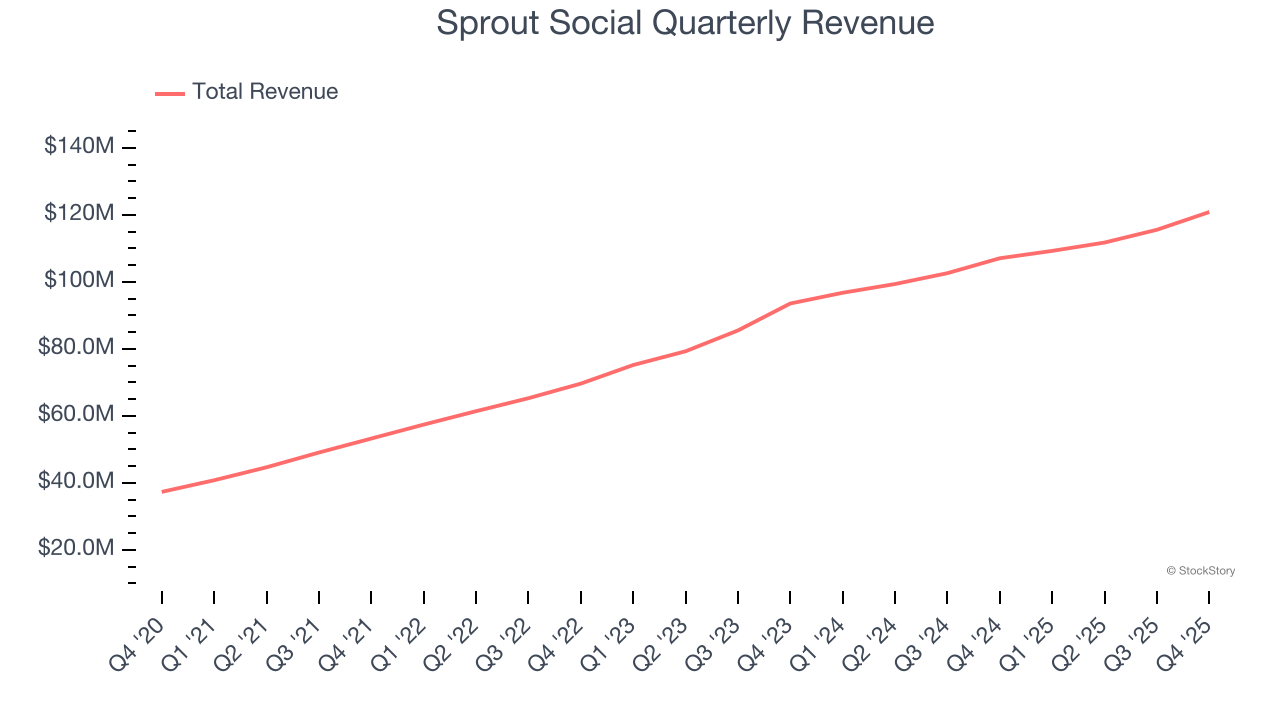

Social media management platform Sprout Social (NASDAQ: SPT) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 12.9% year on year to $120.9 million. On the other hand, next quarter’s revenue guidance of $120.3 million was less impressive, coming in 0.8% below analysts’ estimates. Its non-GAAP profit of $0.20 per share was 26.3% above analysts’ consensus estimates.

Is now the time to buy Sprout Social? Find out by accessing our full research report, it’s free.

Sprout Social (SPT) Q4 CY2025 Highlights:

- Revenue: $120.9 million vs analyst estimates of $118.8 million (12.9% year-on-year growth, 1.8% beat)

- Adjusted EPS: $0.20 vs analyst estimates of $0.16 (26.3% beat)

- Adjusted Operating Income: $11.51 million vs analyst estimates of $10.24 million (9.5% margin, 12.5% beat)

- Revenue Guidance for Q1 CY2026 is $120.3 million at the midpoint, below analyst estimates of $121.3 million

- Adjusted EPS guidance for the upcoming financial year 2026 is $0.93 at the midpoint, beating analyst estimates by 3%

- Operating Margin: -9%, up from -12.8% in the same quarter last year

- Free Cash Flow Margin: 9%, up from 7.4% in the previous quarter

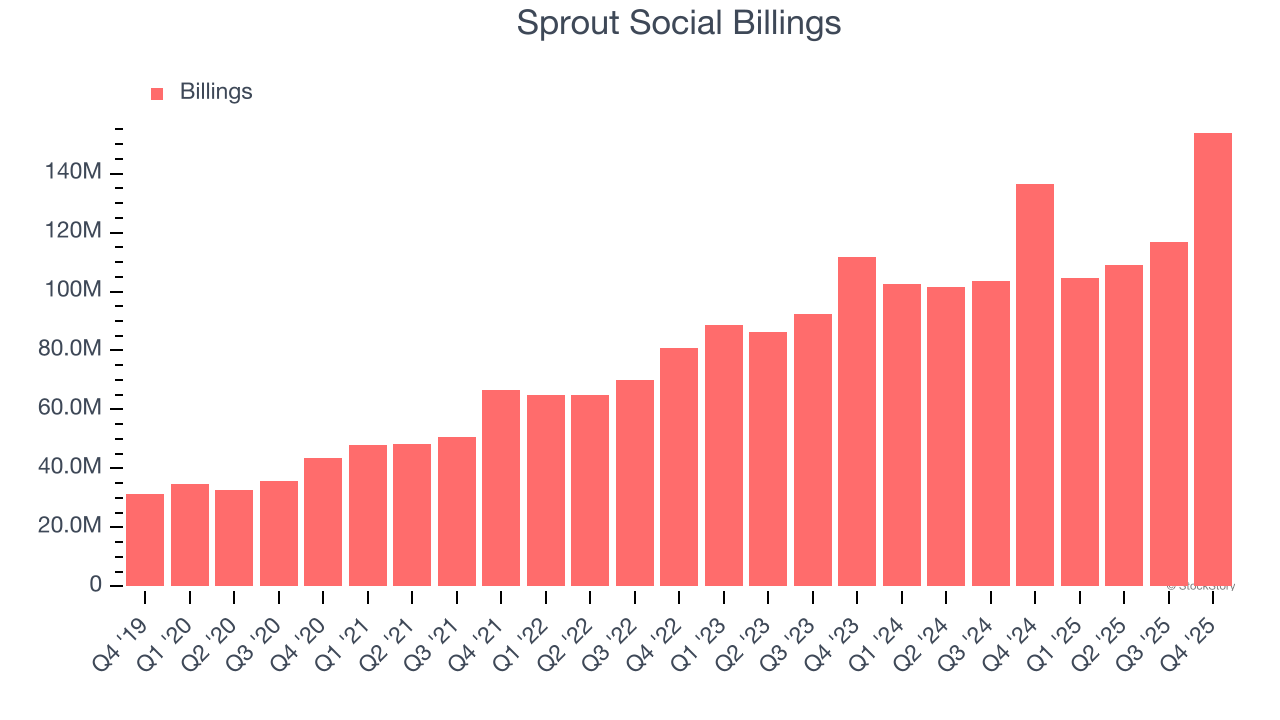

- Billings: $153.9 million at quarter end, up 12.7% year on year

- Market Capitalization: $400.1 million

“Our team delivered strong results in the fourth quarter, highlighted by 15% total RPO growth and strong non-GAAP profitability," said Ryan Barretto, CEO of Sprout Social.

Company Overview

Born from the recognition that businesses needed a centralized way to handle their growing social media presence, Sprout Social (NASDAQ: SPT) provides a comprehensive software platform that helps businesses manage, analyze, and optimize their presence across various social media networks.

Revenue Growth

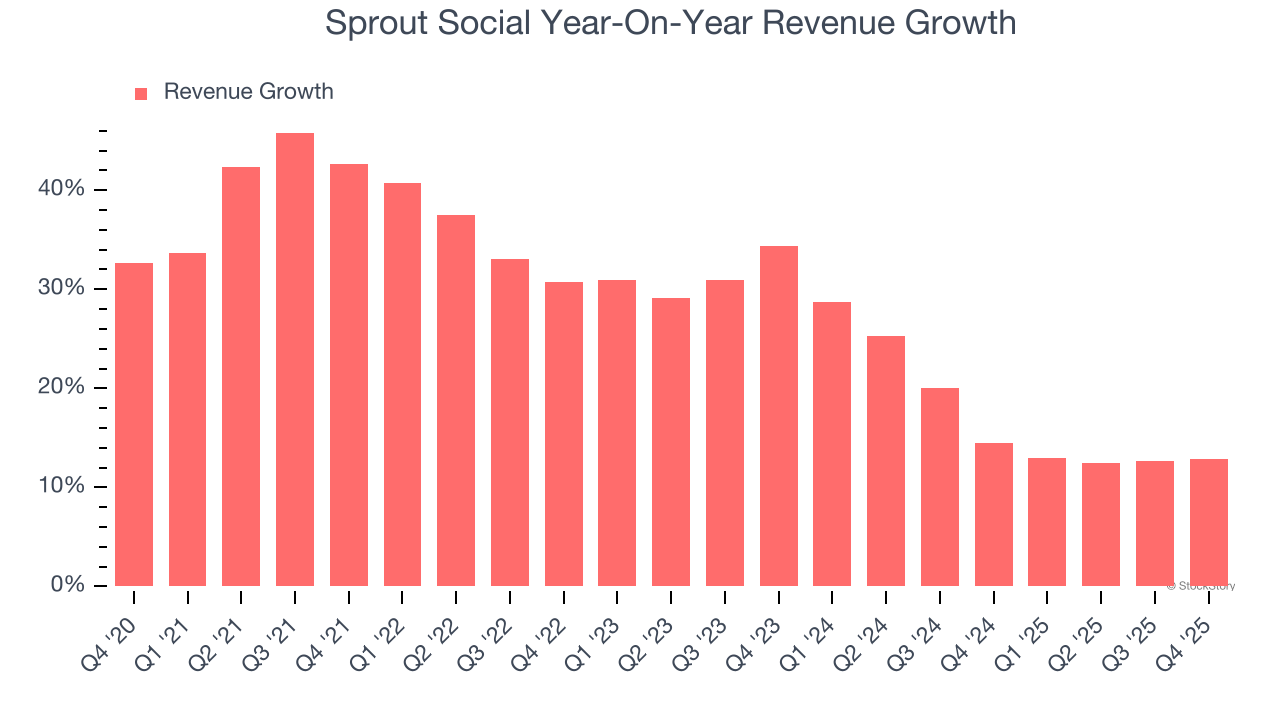

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Sprout Social grew its sales at an impressive 28% compounded annual growth rate. Its growth beat the average software company and shows its offerings resonate with customers.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Sprout Social’s annualized revenue growth of 17.1% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Sprout Social reported year-on-year revenue growth of 12.9%, and its $120.9 million of revenue exceeded Wall Street’s estimates by 1.8%. Company management is currently guiding for a 10.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 10.3% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will face some demand challenges.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Sprout Social’s billings came in at $153.9 million in Q4, and over the last four quarters, its growth was underwhelming as it averaged 8.7% year-on-year increases. This alternate topline metric grew slower than total sales, meaning the company recognizes revenue faster than it collects cash - a headwind for its liquidity that could also signal a slowdown in future revenue growth.

Key Takeaways from Sprout Social’s Q4 Results

It was great to see Sprout Social’s full-year EPS guidance top analysts’ expectations. We were also glad its billings outperformed Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed and its full-year revenue guidance fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 1.7% to $7.01 immediately after reporting.

Sprout Social underperformed this quarter, but does that create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).