Okta’s stock price has taken a beating over the past six months, shedding 22.1% of its value and falling to $71.14 per share. This might have investors contemplating their next move.

Is now the time to buy Okta, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Okta Not Exciting?

Even though the stock has become cheaper, we don't have much confidence in Okta. Here are three reasons we avoid OKTA and a stock we'd rather own.

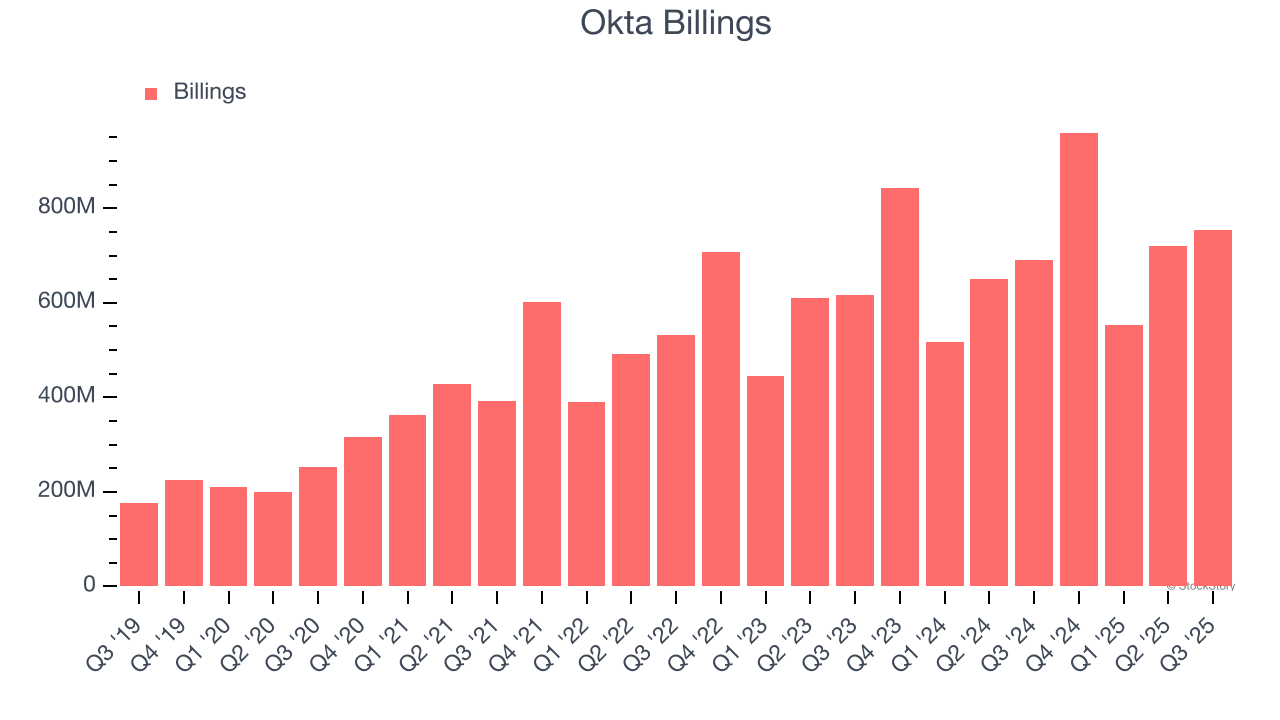

1. Weak Billings Point to Soft Demand

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Okta’s billings came in at $754 million in Q3, and over the last four quarters, its year-on-year growth averaged 10.2%. This performance was underwhelming and suggests that increasing competition is causing challenges in acquiring/retaining customers.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Okta’s revenue to rise by 9.2%, a deceleration versus its 29.9% annualized growth for the past five years. This projection is underwhelming and suggests its products and services will face some demand challenges.

3. Cash Flow Margin Set to Decline

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the next year, analysts predict Okta’s cash conversion will fall. Their consensus estimates imply its free cash flow margin of 31.5% for the last 12 months will decrease to 29.3%.

Final Judgment

Okta isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 4× forward price-to-sales (or $71.14 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at one of our top digital advertising picks.

Stocks We Would Buy Instead of Okta

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.