iPhone and iPad maker Apple (NASDAQ: AAPL) reported Q3 CY2025 results exceeding the market’s revenue expectations, with sales up 7.9% year on year to $102.5 billion. Its GAAP profit of $1.85 per share was 4.5% above analysts’ consensus estimates.

Is now the time to buy Apple? Find out by accessing our full research report, it’s free for active Edge members.

Apple (AAPL) Q3 CY2025 Highlights:

- Revenue: $102.5 billion vs analyst estimates of $101.6 billion (0.8% beat)

- Operating Profit (GAAP): $32.43 billion vs analyst estimates of $31.68 billion (2.4% beat)

- EPS (GAAP): $1.85 vs analyst estimates of $1.77 (4.5% beat)

- Products Revenue: $73.72 billion vs analyst estimates of $73.35 billion (small beat)

- Services Revenue: $28.75 billion vs analyst estimates of $28.22 billion (1.9% beat)

- Gross Margin: 47.2%, in line with the same quarter last year

- Operating Margin: 31.6%, in line with the same quarter last year

- Free Cash Flow Margin: 25.8%, in line with the same quarter last year

- Market Capitalization: $4.00 trillion

Revenue Growth

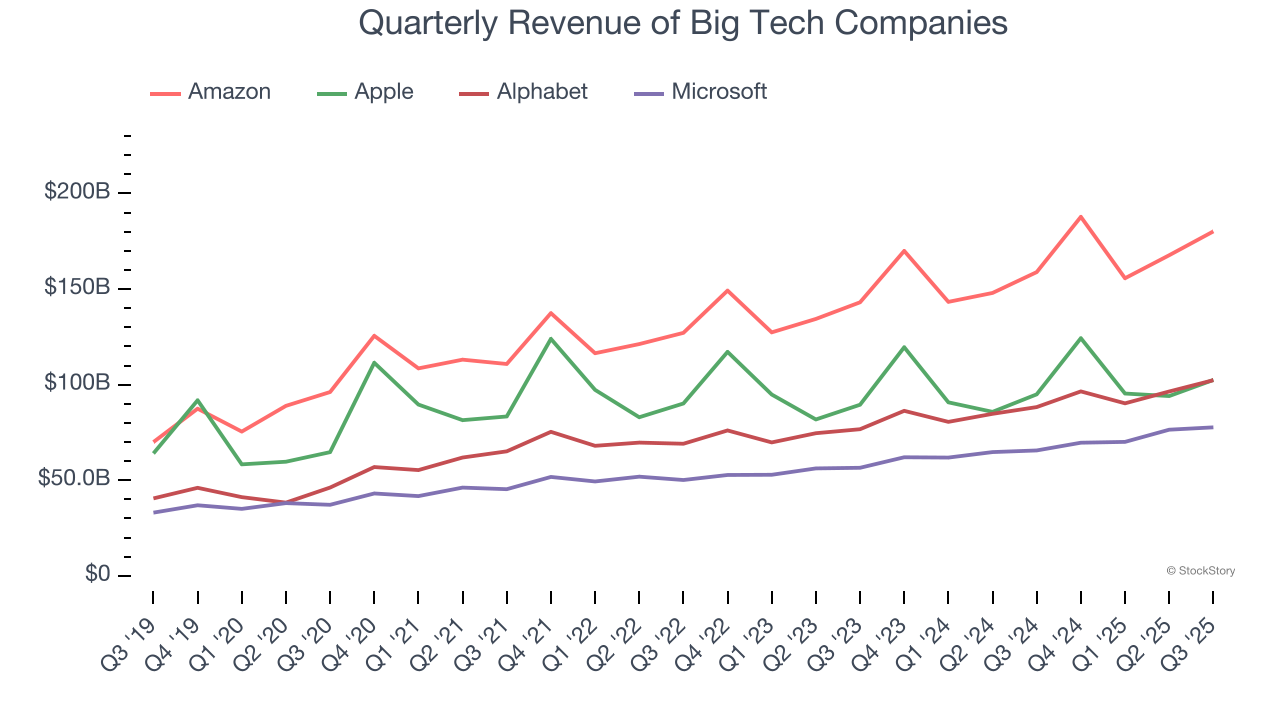

Apple (with its installed base of 2 billion+ devices) shows that growth and massive scale can coexist despite conventional wisdom. The company’s revenue base of $274.5 billion five years ago has increased to $416.2 billion in the last year, translating into a decent 8.7% annualized growth rate.

In light of its big tech peers, however, Apple’s growth trailed Amazon (14.7%), Alphabet (17.6%), and Microsoft (14.8%) over the same period. Comparing the four is relevant because investors often pit them against each other to derive their valuations. When adjusting for these benchmarks, we think Apple is expensive.

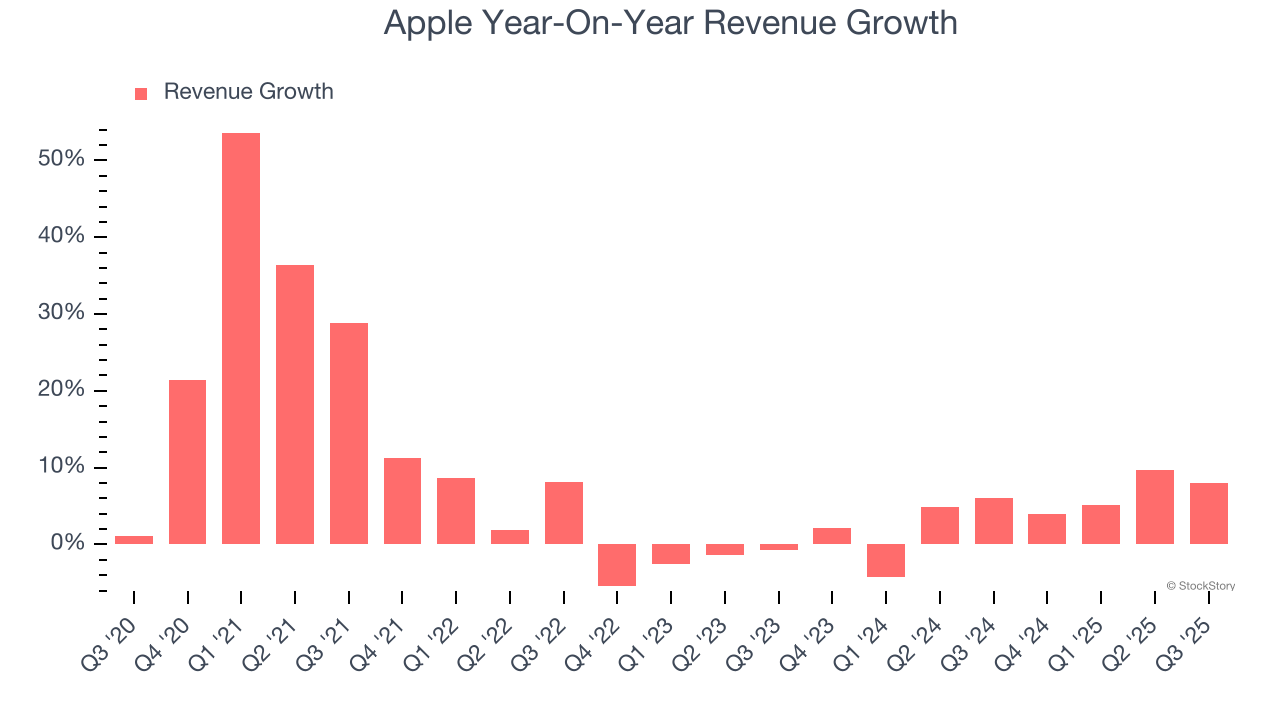

We at StockStory emphasize long-term growth, but for big tech companies, a half-decade historical view may miss emerging trends in AI. Apple’s recent performance shows its demand has slowed as its annualized revenue growth of 4.2% over the last two years was below its five-year trend.

This quarter, Apple reported year-on-year revenue growth of 7.9%, and its $102.5 billion of revenue exceeded Wall Street’s estimates by 0.8%. Looking ahead, sell-side This projection illustrates the market sees some success for its newer AI-enabling Apple Intelligence products. However, its anticipated growth is still a far cry from its heyday in the 2010s.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

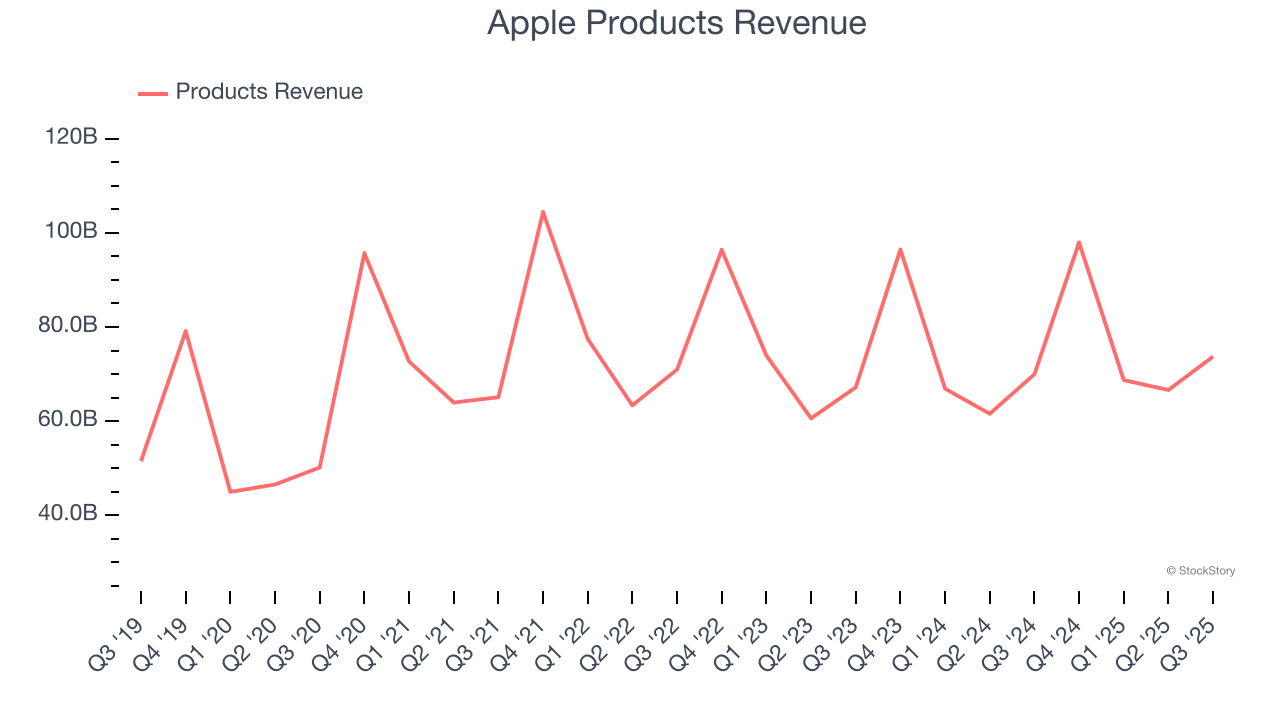

Products: Steve Jobs’s Legacy

Apple’s Products segment includes everything from its flagship iPhone, iPad, and MacBook computers to AirPods and Apple Watch. We are closely monitoring whether the GenAI-powered Apple Intelligence, which was released in September 2024 but has limited interoperability with older devices, can spur an upgrade cycle for the company.

Products sales are by far the biggest chunk of Apple’s revenue at 73.8%, and they grew by 6.8% annually over the last five years, slower than total revenue. Recently, sales have also decelerated, growing at an annual clip of 1.5% over the last two years. Apple could really use that upgrade cycle right about now.

This quarter, Products sales were up 5.4% year on year, in line with Wall Street’s estimates. Holding aside expectations, the recently improved rate of change shows that more customers are upgrading their devices than before. We’ll be watching to see if Apple Intelligence and iOS 18 can accelerate this trend. Wall Street is pricing the stock like it will.

Key Takeaways from Apple’s Q3 Results

It was encouraging to see Apple narrowly top analysts’ revenue expectations this quarter, and the beat in Services was a bright spot. We were also happy its EPS outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock traded up 1.5% to $275.50 immediately following the results.

Apple had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.