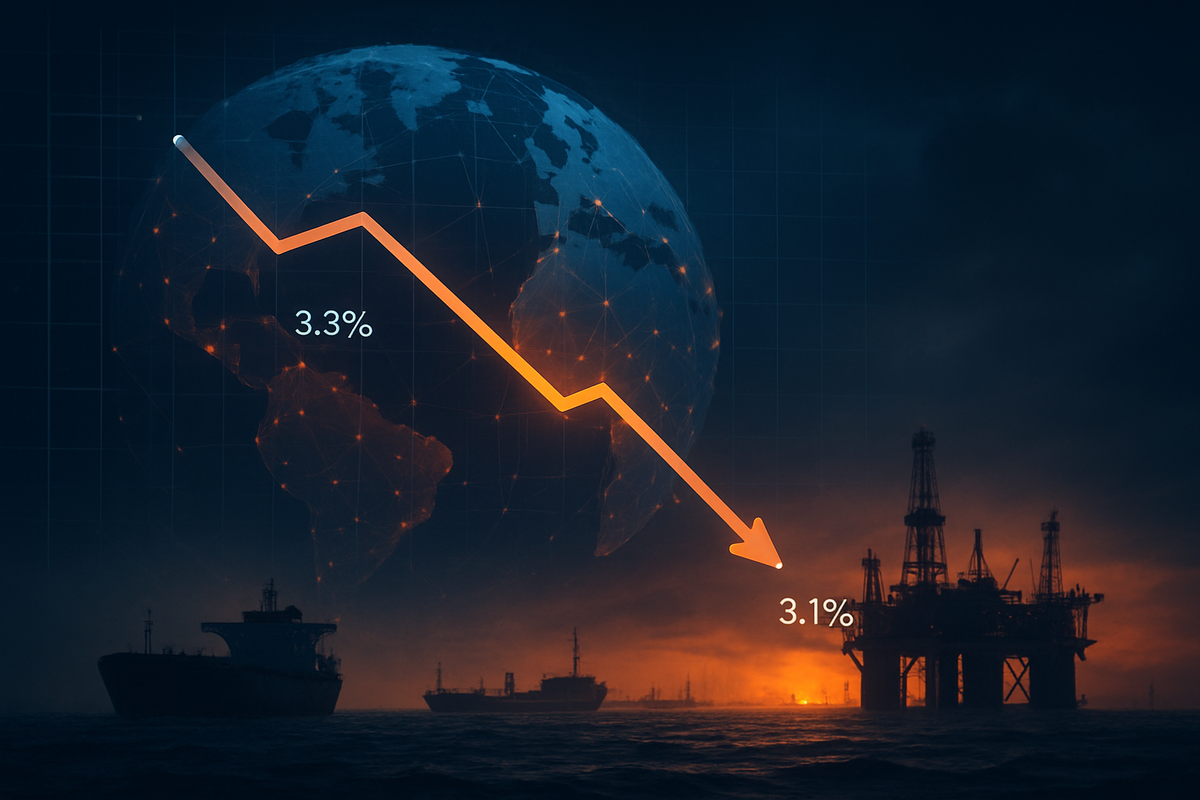

The global economic recovery has hit a significant roadblock as the International Monetary Fund (IMF) officially downgraded its 2026 global growth projection to 3.1%, a notable drop from the 3.3% forecast issued just three months ago in January. In its latest World Economic Outlook report released today, April 14, 2026, the IMF cited the escalating conflict in the Middle East and the resulting surge in energy prices as the primary drivers behind the revised outlook.

This downward revision signals an end to the "soft landing" optimism that characterized the start of the year. Economists at the IMF warned that while the global economy has shown resilience in recent years, the functional closure of key maritime corridors and the threat of a prolonged regional war have created a "fragile and uncertain" environment that could worsen if diplomatic efforts fail to restore stability in the Persian Gulf.

The downgrade follows a turbulent first quarter in 2026, dominated by the outbreak of hostalities involving several regional powers and the subsequent blockade of the Strait of Hormuz in late February. This maritime chokepoint, through which roughly 20% of the world’s oil and liquefied natural gas (LNG) flows, has seen traffic plummet as shipping insurance premiums skyrocketed and military activity intensified. As a result, Brent crude prices, which started the year around $66 per barrel, spiked to a mid-March peak of $126 before settling at the current level of approximately $102.

The timeline of this economic cooling began in earnest following the January forecast, when a series of escalations in the Persian Gulf led to "Force Majeure" declarations from major energy producers. By March, the impact on global supply chains became undeniable as the cost of shipping surged. The IMF’s Managing Director emphasized today that the 0.2 percentage point cut reflects the immediate "inflationary tax" that higher energy costs have placed on both industrial production and consumer spending across the globe.

Initial market reactions to the IMF's report were swift. Stock markets in Asia and Europe, which are more heavily dependent on Middle Eastern energy imports, saw broad sell-offs in the industrial and transport sectors. Conversely, defense and domestic energy stocks in the United States saw a modest uptick as investors pivoted toward perceived "safe havens." The IMF’s "Severe Scenario" warning—a chilling projection that global growth could collapse to just 2.0% if the energy shocks persist throughout the year—has added a layer of urgency to international diplomatic efforts.

The ripple effects of this forecast cut have created a stark divide between winners and losers in the corporate world. Major oil and gas companies, such as ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX), have seen their margins expand as global prices rise, though they face significant operational risks for their joint ventures in the affected region. Similarly, Saudi Aramco (TADAWUL: 2222) continues to navigate a high-price environment while dealing with the logistical nightmare of exporting oil around the Cape of Good Hope, a route that adds thousands of miles and significant costs to every barrel delivered.

In the logistics sector, shipping giants like A.P. Møller - Mærsk A/S (CPH: MAERSK-B) and Hapag-Lloyd (ETR: HLAG) are seeing a complex impact. While freight rates have spiked due to the necessity of rerouting vessels, the increased costs of bunker fuel and insurance are eating into profits. Meanwhile, the manufacturing sector is feeling the squeeze; Tesla (NASDAQ: TSLA) and other electric vehicle manufacturers are facing higher production costs due to the surge in electricity prices and potential disruptions in the supply of raw materials like aluminum and high-grade plastics, which are energy-intensive to produce.

Conversely, the renewable energy sector and firms specializing in energy efficiency, such as NextEra Energy (NYSE: NEE), are seeing renewed investor interest. The IMF’s report suggests that this crisis may accelerate the "Great Pivot" away from fossil fuel dependency in Europe and East Asia. However, the short-term pain is expected to hit consumer-facing giants like Amazon (NASDAQ: AMZN) and DHL Group (ETR: DHL), as the cost of fulfillment and global shipping reaches levels not seen since the 2022 energy crisis following the invasion of Ukraine.

The current situation is more than just a temporary spike in oil prices; it represents a significant threat to the post-pandemic stabilization trends of 2024 and 2025. This event mirrors the historical oil shocks of 1973 and 1979, yet the global economy in 2026 is structurally different. The IMF noted that while the volume of oil removed from the market is historically high, the global "oil intensity"—the amount of oil used to produce one dollar of GDP—has fallen by nearly 50% over the last four decades. This efficiency has prevented a full-scale global recession thus far, but the IMF warns that even an efficient economy has a breaking point.

The wider significance of this growth cut also lies in its potential to force central banks, such as the Federal Reserve and the European Central Bank, into a difficult position. Just as many expected a period of sustained interest rate cuts, the sudden rise in energy-driven inflation to 4.4% may force a "higher for longer" policy stance. This could exacerbate the debt burdens of emerging markets, many of which are already struggling with the dual impact of higher energy costs and a strengthening U.S. dollar.

Furthermore, this crisis highlights the ongoing trend of "regionalization" in global trade. As the Suez Canal and the Strait of Hormuz become high-risk zones, the IMF expects to see a surge in "friend-shoring" and "near-shoring" initiatives. This structural shift in how and where goods are produced could lead to a permanent increase in global cost bases, making the IMF’s 3.1% growth target seem optimistic if geopolitical fractures continue to widen.

Looking ahead, the next six months will be critical for determining which path the global economy takes. The IMF has laid out two distinct possibilities: a "Stabilization Scenario" where diplomatic interventions reopen the Strait of Hormuz by Q3 2026, allowing growth to rebound toward 3.2% by 2027, and the aforementioned "Severe Scenario." In the latter case, should military escalation continue, the world could face a period of stagflation—low growth coupled with high inflation—that would require radical economic policy shifts.

Market participants should look for strategic pivots from major industrial players. We may see a rapid acceleration in the adoption of hydrogen fuel and small modular nuclear reactors as nations scramble for energy independence. For companies, the "just-in-time" supply chain model may be permanently replaced by "just-in-case" strategies, requiring higher inventory levels and greater capital expenditure, which could further dampen short-term growth but build long-term resilience.

The IMF’s downgrade of global growth to 3.1% is a sobering reminder of how quickly geopolitical events can unravel economic progress. While the world is better prepared for energy shocks than it was in the 20th century, the interconnectedness of modern trade means that a disruption in the Persian Gulf is felt in every corner of the market, from the gas pump to the semiconductor factory.

As we move forward into the remainder of 2026, the key for investors will be monitoring the duration of the conflict and the response of central banks to the new inflationary pressure. The resilience of the U.S. economy as a net energy exporter provides some cushion, but the fragility of the Eurozone and Asian manufacturing hubs remains a significant concern. The transition from 3.3% to 3.1% may seem small on paper, but it represents hundreds of billions of dollars in lost economic output and a significant shift in the global risk landscape.

This content is intended for informational purposes only and is not financial advice.