Despite a weakened commodity price environment, Viper Energy, Inc. (NASDAQ: VNOM) is showing some real bite.

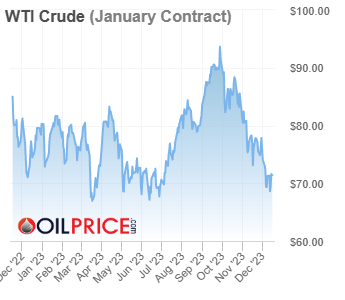

Shares of the Midland, Texas oil & gas company closed at $30.54 on Friday, up 25% from six months ago — and riding a six-month win streak. Meanwhile, WTI crude futures continued to trade in the low $70’s, down more than 20% from their September 2023 peak — and roughly flat from where they were six months ago.

In an industry that typically moves hand-in-hand with oil pricing, Viper Energy is going counterflow because its financial success is about more than realized selling prices. Capital efficiency matters too. And in what could be a deflationary U.S. economy in 2024, prospects of lower costs and higher margins are making investors forget about the recent oil price slick.

Viper Energy is a different animal in the exploration & production (E&P) space. For starters, it is a variable distribution limited partnership (LP). Common in the energy sector, an LP provides and manages resources for other oil companies. Rather than doing the actual oil drilling, it may provide supplies, logistics, pipeline transportation, refining or other support. The LP structure allows it to seek capital from investors and keep a stake in the business.

As for the ‘variable distribution’ part, Viper Energy returns a large portion of its cash flow to shareholders. Since LP distributions are considered ‘tax-sheltered’ money from a ‘pass-through entity,’ company profits and losses pass through to the investor. This makes shareholders — and not Viper Energy — effectively responsible for paying company income taxes. Unlike dividends, LP distributions lower the cost basis of the LP investment (instead of being taxed in the year received). The tax liability comes when shares are sold. Appreciation caused by the distributions is treated as a capital gain and not as ordinary income.

With Viper Energy, however, there’s no need to worry about the tax complications and tax-deferred, IRA-unfriendly nature of MLPs that often turn off investors. That is because the company is considered a regular corporation when it comes to U.S. federal income taxes. The cash distributions received by shareholders are simply treated as dividends.

Additionally, Viper Energy is a subsidiary of Diamondback Energy, a large cap oil, gas and natural gas liquids (NGL) producer that trades as a separate entity under the ‘FANG’ ticker. Through its relationship with Diamondback, Viper has mineral interests in the prolific, oil-rich Eagle Ford and Permian Basin shale plays of Texas and New Mexico. These assets are leased to the partnership’s ‘working interest owners’ who are responsible for exploration, development and production costs.

The better these costs are managed — in any oil price backdrop — the better its financial results. In other words, for energy LPs, it’s all about gaining scale and efficiency. These are two areas in which Viper excels — and is expected to derive future outperformance from.

Production, and profits are up

Last month, Viper reported that third-quarter production increased 11% year-over-year to 40,445 boe/d, the highest in company history. This drove a 12% jump in adjusted earnings per unit of $1.10, which was more than twice what Wall Street expected. It marked the sixth consecutive quarter in which Viper beat the consensus earnings estimate.

The production gains helped offset significant decreases in sale pricing. Average realized oil, natural gas and NGL prices were down 10%, 74% and 39%, respectively, from the prior year quarter. Since oil accounted for roughly 55% of production, it was the sharp drop in gas pricing that prevented a stronger quarter.

Remember though, that cost efficiency reigns supreme when it comes to energy LPs. On a per barrel of oil equivalent (boe) basis, Viper’s third-quarter operating expenses fell 32% while operating cash flow rose 12%. It was an ideal performance in a soft commodity backdrop — and one that has set the stage for a strong 2023 finish and 2024 outlook.

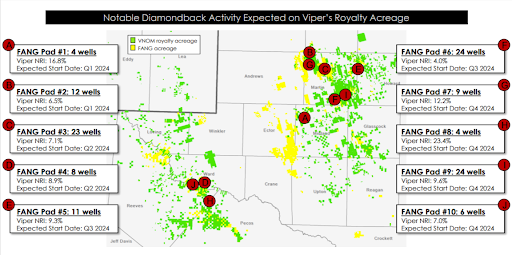

For all of 2023, management forecasts that production will be up 17% to 39,250 boe/d. This includes a sequential acceleration in fourth-quarter production to 43,750 boe/d (at the midpoint of guidance). The anticipated ramp stems from several Diamondback wells that were slated to start production in the current quarter. If all goes according to plan, some 125 wells across 10 shale pads will be launched this year. Rising production in an improving cost setting bodes well for future earnings.

Viper’s preliminary estimate for 2024 production of 48,000 represents 22% growth. According to the latest U.S. Energy Information Administration (IAE) forecast, oil prices will trend slightly higher in 2024. Last week, the EIA trimmed its 2024 average Brent spot price prediction to $82.57, but it’s a figure that remains above Friday’s closing spot rate of $76.89. Even if crude and gas prices stay relatively flat, profits should increase at Viper because of the company’s below-industry cost structure. Next year’s unit costs are expected to be just $9.75/boe.

GRP buyout boosts growth outlook

Diamondback gave Viper its original Permian Basin assets in June 2014 when Viper completed its initial public offering (IPO). Since then, it has amassed 27,189 net royalty acres and 73 operating rigs with estimated proved reserves of 149 million barrels of oil equivalent (MMBoe) as of September 30th.

Viper’s growth outlook got a significant boost last month when it acquired mineral and royalty interests from GRP Energy Capital and Warwick Capital Partners. The $1 billion cash-and-stock deal will add approximately 7,300 net royalty acres (mostly in the Permian Basin) that are currently producing 4,000 boe/d. Like much of Viper’s existing base, the GRP assets are considered to be premium undeveloped acreage. Next year, the assets are forecast to increase production to 4,750/bod/d and boost Viper’s acreage by 27% to 34,500.

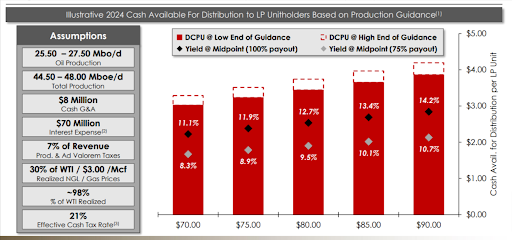

From an investment perspective, this is expected to mean more cash available for distributions. As the chart below illustrates, based on management’s assumptions around production, expenses and realized prices, LP unitholders are forecast to see 8.3% to 10.7% cash flow yields under the standard 75% payout scenario. The potential yield range increases to 11.1% to 14.2% under a 100% payout scenario.

Generous shareholder returns

Viper’s multi-layered return of capital framework stands out among mid-cap energy players. Its commitment is to return at least 75% of distributable cash to shareholders. This is accomplished through:

- a quarterly base distribution;

- a variable distribution; and

- opportunistic share repurchases.

In Q3, the company paid a base distribution of $0.27 per share and repurchased an amount equivalent to $0.06 per share. To get to the 75% payout target, it then added a variable dividend of $0.30 per share to bring the total quarterly return of capital to $0.63 per share.

Stripping out the distribution, or dividend, portion of the payout, Viper awarded shareholders with cash of $0.57 per share. This equates to a full-year payout of $2.28 per share. Based on Friday’s close, it also gives the stock a 7.5% forward dividend yield that is well above the average energy stock yield of 4.2%.

Due to its premium assets, connection to Diamondback and high payout policy, Viper shares trade at a premium to most E&P companies. Its price-to-earnings (P/E) ratio based on 2024 earnings is around 12x. This ranks fourth highest out of 27 mid-cap companies in the industry. It is still inexpensive, however, relative to most U.S. mid-caps and the broader S&P 400 index.

Wall Street is gushing

Viper’s premium valuation is one worth paying up for according to Wall Street research firms. Since the company’s November 7th Q3 earnings call, five analysts have offered updated opinions. All five have given VNOM a buy rating, including Evercore ISI — which began covering the stock this month.

The average price target from this ‘Fab 5’ is $38.40. This implies 26% upside from Friday’s close — and this doesn’t include the dividend. Adding the projected forward yield, VNOM has well over 30% upside over the next 12 months in the eyes of the Street. Not too shabby for a momentum stock that has already tripled from its pandemic lows.

Bottom Line

Viper Energy is well-positioned to benefit from exposure to one of North America’s top oil resources in Diamondback. The company’s oil and gas interests are rooted in high-margin, undeveloped shale acreage. Minimal capital spending requirements and a lean cost structure support the potential for outperformance throughout the ups and downs of the commodity price cycle. Viper’s high payout commitment makes it a slithery-good candidate for long-term income investors.