Questions Roark Capital’s Motivations for Maintaining the Status Quo

Believes That Strategic Process Is Required to Maximize Value for All Shareholders

Urges the Board to Listen to Shareholders and Engage with ADW Capital

MIAMI BEACH, Fla., June 09, 2026 (GLOBE NEWSWIRE) -- ADW Capital Management, LLC, which beneficially owns approximately 4.8% of the Common Stock of Driven Brands Holdings Inc. (NASDAQ: DRVN) (the “Company”), issued an open letter to the Company’s board of directors and controlling shareholder Roark Capital Group urging the Company to undertake a strategic review process.

A full copy of the letter is below:

June 9, 2026

Board of Directors

Driven Brands Holdings Inc.

440 South Church Street, Suite 700

Charlotte, NC 28202

and

Roark Capital Group

1180 Peachtree Street NE, Suite 2500

Atlanta, GA 30309

Members of the Board of Directors of Driven Brands Holdings Inc. and Representatives of Roark Capital Group:

ADW Capital Management, LLC (“ADW”), a significant stockholder in Driven Brands Holdings Inc. (NASDAQ: DRVN) (“Driven” or the “Company”), is yet again writing to express our disdain for the status quo. Our firm has continued to increase our stake in Driven and today beneficially owns approximately 4.8% of the shares outstanding through stock and options.

We have repeatedly attempted to impel action from the management of Driven and its controlling shareholder, Roark Capital (“Roark”), which have clearly yielded no progress whatsoever. We believe the business is showing signs of even worse mismanagement than when we first got involved. Driven’s stock has endured a double-digit percentage decline year-to-date while the market is up nearly 10% and the Company is STILL not current on its financials. As detailed recently in the Wall Street Journal,1 the low consumer receptivity to electric vehicles / elimination of tax credit, increased used and new car prices, consumer attitude to slowing changes in feature set, and stickier interest rates have extended the life of the average combustion-engine vehicle to over 13 years. There has never been a better time to be in the aftermarket autocare business, and yet, Driven still figures out a way to fumble the ball!

The Problems Are Hiding in Plain Sight

Let us start with the obvious. Driven’s corporate SG&A has ballooned to new highs, even after divesting a major business.2 We cannot fathom how this is possible. When questioned about it on the earnings call, there were no satisfactory answers — only some rambling about portfolio-management activities and excuses of corporate deleveraging. Consider this math: Driven is expected to earn a 49% gross margin in 2027 and a 23% EBITDA margin according to consensus estimates.3 Valvoline on the other hand is slated to earn a 38.5% gross margin and a 27.5% EBITDA margin in 2027.4 How does Driven manage to earn 4.5% less on EBITDA when it has nearly 10% higher gross margins? When asked privately, Driven’s management has been evasive and leaves investors continuously puzzled and angry. For a management team plagued by a clear lack of credibility with the market, this is just more of what beleaguered shareholders have come to expect: financial metrics that defy logic, a meager and evasive explanation, and consequently a stock that is wholly unownable for the large passive investors. But who can blame them? Governance issues, a spending problem, accounting failures — how can anyone possibly expect the public markets to trust this team and this structure? How could Driven ever reach a fair price with this persistent, multidimensional overhang on the stock?

Consider the mechanics: A long-only mutual fund likely has a single-team / pool of capital evaluating and investing in stocks below $10 billion in market capitalization effectively reducing the “TAM” of prospective investors to effectively zero. So, at a reasonable 12x EBITDA multiple the Company would have to earn at least $1 billion of EBITDA to merit consideration to the broader investing universe – a $12 billion market cap, but realistically $1.5 billion is the more practical threshold – closer to $20 billion in market capitalization – on the verge of being S&P 500 eligible. Driven faces two discrete roadblocks to ever getting there. First, management has demonstrated no acumen in allocating capital, so we have no confidence it can grow the business to that scale in a risk adjusted manner – see car wash exploits detailed in our previous letters for reference.5 Second, Roark owns too much of the stock, so these long-only investors would need to buy from Roark — and how can they, given the lack of trust and track record to date? Roark’s plan is, as per usual, dead on arrival!

Why Would a Sophisticated Sponsor Tolerate This?

While we were at first puzzled as to why a seemingly sophisticated sponsor such as Roark would tolerate the continued mismanagement of a portfolio company, the picture came into focus when we zoomed out and analyzed the greater picture. Driven resides in two of Roark’s earlier vehicles: Fund III (2012) and Fund IV (2016). Publicly available data suggests that Fund IV has fallen short of all expectations. Ten years out, it has returned a paltry 0.25x (as of September 30, 2025)6 and sits at roughly a 7% IRR and this is before the recent decline in Driven’s stock! Furthermore, Fund III where the majority of Roark’s investment in Driven resides, is nearly fifteen years old! These exceedingly patient LPs are starved for returns, and the windfall from executing a transaction in Driven would put nearly $2 billion of cash7 back in their hands — and that is if the Company were sold for the $18 that ADW has already offered. Running a process could and would likely yield materially higher bids. It sounds simple enough, so why isn’t Roark — which owns over 60% of Driven — pushing for it, given the clear benefits to its own LPs as well as to the owners of Driven’s stock?

Roark’s Incentives Are Diametrically Opposed to Yours

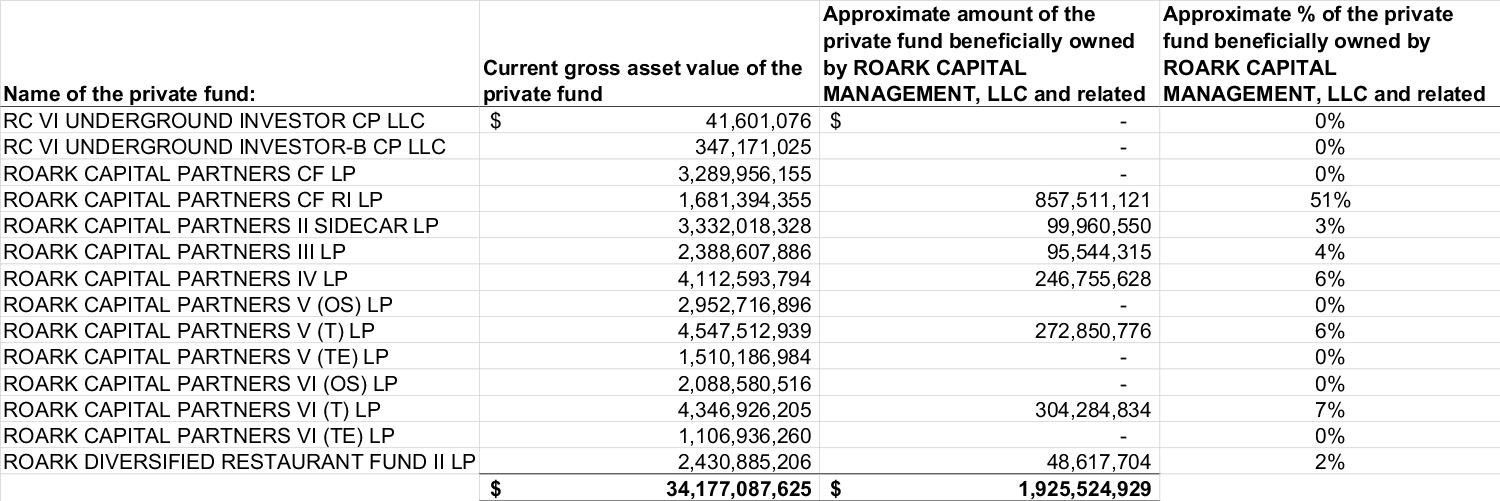

We can think of two likely reasons. First, Roark, like most private-equity firms, is not largely paid on IRR (low hurdles with catchups). It ultimately cares about its gross cash gains or cash multiple --“MOIC”. If Roark believes it can hold Driven for a few more years and slowly grind its way to a higher value, it has every incentive to do so. Even if that means a modest IRR and more anguish for Driven investors who have already been waiting forever, it means more money in Roark’s, and managing partner Neal Aronson’s, pockets when all is said and done — and Roark sits in total control under the current governance structure. Second, Roark as a business has other priorities — namely, preparing its “crown jewel” asset Inspire Brands for a massive IPO to generate liquidity. Roark’s work on Inspire Brands shows the market what “drives” Neal Aronson. Take a look at Roark’s ownership table our firm was able to derive from the firm’s ADV.8

Despite Neal and Roark’s public commitment of being long term and aligned with their LPs, their interests/commitments to the funds are rather pedestrian except what appears to be a continuation fund for Inspire Brands. While we do not have all the specifics (we are not LPs of Roark), it appears that Neal/Roark sold some or all of Inspire Brands to a continuation fund and rolled over his/the firm’s carry in stock which was likely a tax-free transaction. While now in direct possession of the stock, the traditional private equity waterfall dynamics change and he’s already gotten paid. Maybe Neal wants to use Inspire Brands to create his own public “Berkshire Hathaway” on the backs of his LPs? Take the fees in stock, pay no tax, never distribute the shares, and sit in his ivory tower while investors continue to be de-prioritized? Maybe he wants to take Inspire Brands public and merge it with Driven so it’s one large 1960’s style conglomerate with cross interests where it trades at a massive discount and all stakeholders lose except for “King Neal”? Furthermore, is it a coincidence that GoTo Foods, Youth Enrichment Brands, and the other “brand platforms” have yet to be sold/monetized? Perhaps this is truly part of a larger plan of merging all these businesses into a single entity controlled by your friend King Neal?

Taking Inspire Brands public will be an intense process, one that requires Roark to cultivate the trust of passive investors and other public-market participants. Those groups need to believe Roark is a thoughtful and responsible steward of the companies it takes public, and Driven is a highly inconvenient thorn in the side of that narrative. To put it all together: we believe that Roark actually gets paid more, and enjoys an easier path to an Inspire Brands IPO, by sweeping Driven under the rug and letting the clock keep running. Its incentives appear to be diametrically opposed to those of common shareholders of Driven like us — and to the many mom-and-pop investors we have heard from, who ended up with Driven shares through a business acquisition and have watched their value crater meaningfully since the IPO price of $22 over 5 years ago in January of 2021.

A Direct Message to Neal Aronson

Mr. Aronson, this one is for you. We know you like to keep a low profile, embrace long-term thinking, and let the results speak for themselves. But that professed philosophy is the perfect cover for you to deliver years of mediocre results to your LPs while quietly earning yourself a king’s ransom. You have built, by any measure, a wildly profitable firm that has almost certainly left you with a fabulous personal fortune of $4 Billion (according to Forbes9) far greater than Driven’s entire market capitalization. But what about your LPs in Fund III and Fund IV and their stakeholders? Among them are many public employees who depend on the pension dollars they have entrusted to your funds for subsistence in retirement. They have been waiting — in some cases for more than a decade — for you to realize the value in this business, while Roark continues to collect significant management fees. According to Roark’s Form ADV,10 your firm’s AUM is over $34 billion, charging as much as 2 percent management fees not including other fees that could be charged at the portfolio level, and only employs 145 people – 104 in an advisory setting. One of these investment professionals just so happens to be the son of Jonathan Fitzpatrick (former CEO and current Chairman of Driven). So, how can we see things any way other than Roark taking advantage of Driven’s public market investors, mismanaging the Company and misallocating capital, all while writing checks directly to the family of the former CEO and current chairman?

To put things in perspective, even if each Roark employee made an even $1m, that would be approximately $145m per year of firmwide compensation for a business with one single office in Atlanta (where rent is cheap). Are we to assume that means you, Neal, are personally clearing over $500 million in management fee income per year? We calculate internal capital in the funds of approximately $2 Billion (see above table). And we have also heard that “Neal is the only one that makes any money there” according to a number of personal accounts. What’s the ROIC on $500 million of perpetual fee income on a $2bn “investment” in the business. We would also like to note that this analysis does not include carry from keeping capital tied up in Driven rather than selling it off. How should we compare the astronomical return you earn to what LPs in your funds get? Do you intend to write pensioners checks out of your own multi-billion-dollar coffers / fee stream as they wait for a return and you extract every last dollar of carry? What would you say to investors who believe that you are not doing everything in your power to deliver all available value to your earliest LPs because it conflicts with your other priorities? TO US, YOUR ACTIONS APPEAR MORE CONSISTENT WITH A ZOMBIE FUND GP THAN ONE WHO IS LOOKING TO RAISE FUTURE FUNDS AND MAXIMIZE LP RETURNS!

Driven is a valuable business with a reason to exist, but not this way, as a standalone public company under majority Roark ownership, with a set of incentives that aren’t aligned with the Company’s public shareholders. Do the right thing for us, for your early LPs, and for the company’s shareholders. And do it now — even if your investor-relations team tells you to wait until after the fundraise, or your capital-markets advisors tell you to wait until after the Inspire Brands IPO. When it comes to corporate governance, we believe “sunlight is always the best disinfectant,” and we will continue to dig through all available data until everything is out in the open.

Our Demand

We offered $18 per share and were met with silence. How can this Board fail even to respond to an offer representing a 40% premium to today’s price? Who is really calling the shots? Where are the “independent” board members? Each of you owes a fiduciary duty to those of us who own this stock. Roark may do as it pleases with its private portfolio companies (and it has!), but Driven needs to be sold — and our voice will only grow louder until it is. We will make our case in the court of public opinion: the very venue where Roark hopes to finish raising Fund VII and take Inspire Brands public. If Driven’s management and Roark do not take decisive and immediate action to address this situation, they will reveal themselves to be unfit stewards not only of this business, but of any company – public or private.

Sincerely,

Adam Wyden

Managing Member

ADW Capital Management, LLC

About ADW Capital Management, LLC

ADW Capital Management, LLC is the investment advisor for a concentrated, long-biased investment partnership founded by Adam Wyden in 2010.

Contact

Adam Wyden

ADW Capital Management, LLC

(646) 684-4086

adam@adwcapital.com

1 https://www.wsj.com/business/autos/americans-are-keeping-their-cars-longer-than-ever-and-remaking-the-auto-industry-c169e494

2 Company Filings

3 S&P Capital IQ

4 S&P Capital IQ

5 ADW estimates and analysis

6 Santa Barbara County Employees’ Retirement System 2026 Private Equity Portfolio Review

https://public.onboardmeetings.com/Meeting/ZQyPM00%2FWIR7MMnkqXwyPAtGXpL8E40IlIWKbCxv4h8A/DsUibpcueKfhvylArtNsnoFe6HzIvPWrs870L0v7Et0A/WpdpPSUDUxscVKDlcui3vnYMvIpswpDjTRQKvvvEY3YA/FBN10Dmhjcy3VhuqYYV28Ft8OjaZ%2F2gJmawp%2FV4Z3EoA/Agenda%20Document

7 Company Filings / ADW estimates and analysis

8 https://reports.adviserinfo.sec.gov/reports/ADV/160368/PDF/160368.pdf / ADW estimates and analysis

9 https://www.forbes.com/profile/neal-aronson/

10 https://reports.adviserinfo.sec.gov/reports/ADV/160368/PDF/160368.pdf

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/ed2e25fc-b26b-4ec7-9258-b2ab803a5f98