Over the last six months, OneMain’s shares have sunk to $61.85, producing a disappointing 9% loss - a stark contrast to the S&P 500’s 6.1% gain. This might have investors contemplating their next move.

Is now the time to buy OneMain, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is OneMain Not Exciting?

Despite the more favorable entry price, we’re cautious about OneMain. Here are three reasons you should be careful with OMF, plus one stock we’d rather own.

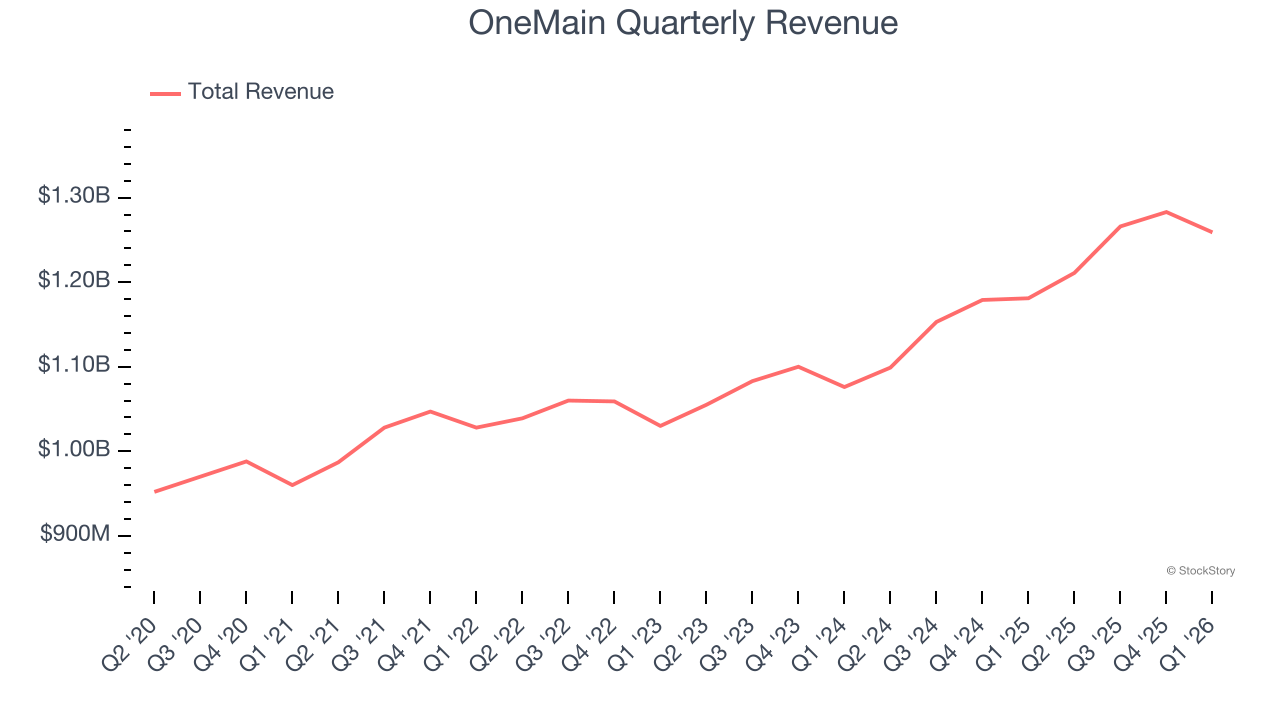

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

Over the last five years, OneMain grew its revenue at a tepid 5.3% compounded annual growth rate. This was below our standard for the financials sector.

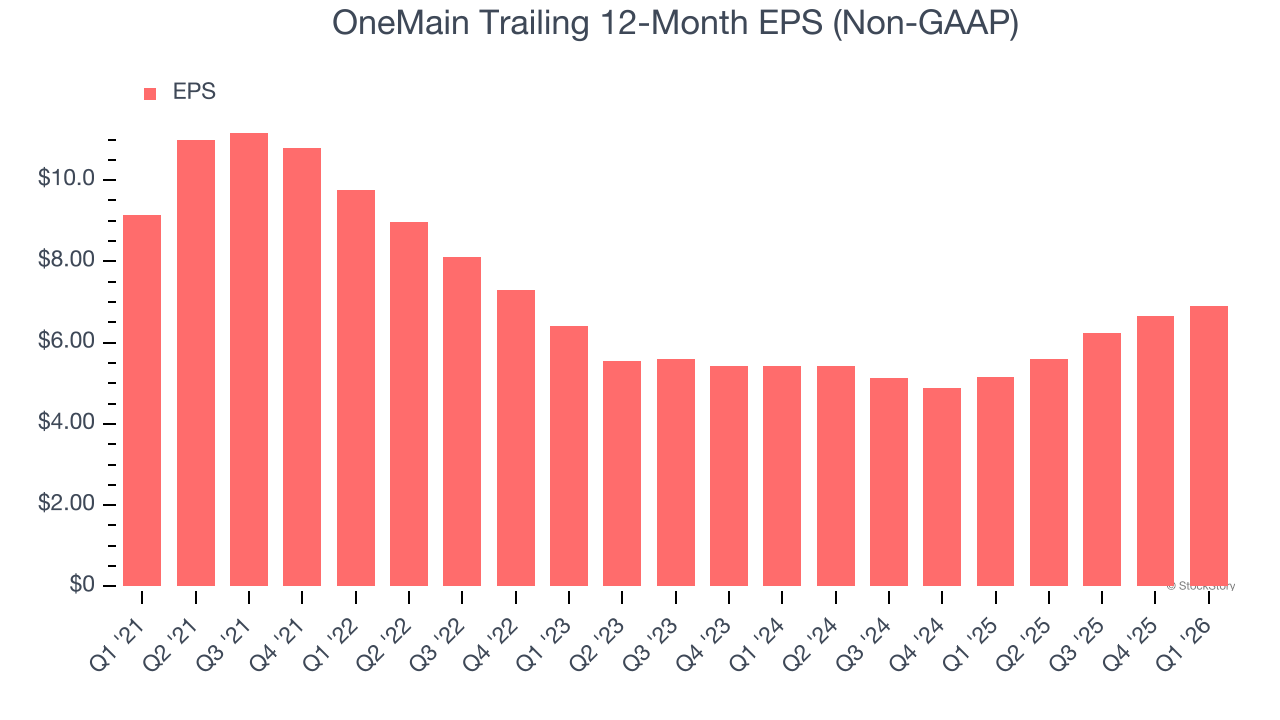

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for OneMain, its EPS declined by 5.5% annually over the last five years while its revenue grew by 5.3%. This tells us the company became less profitable on a per-share basis as it expanded.

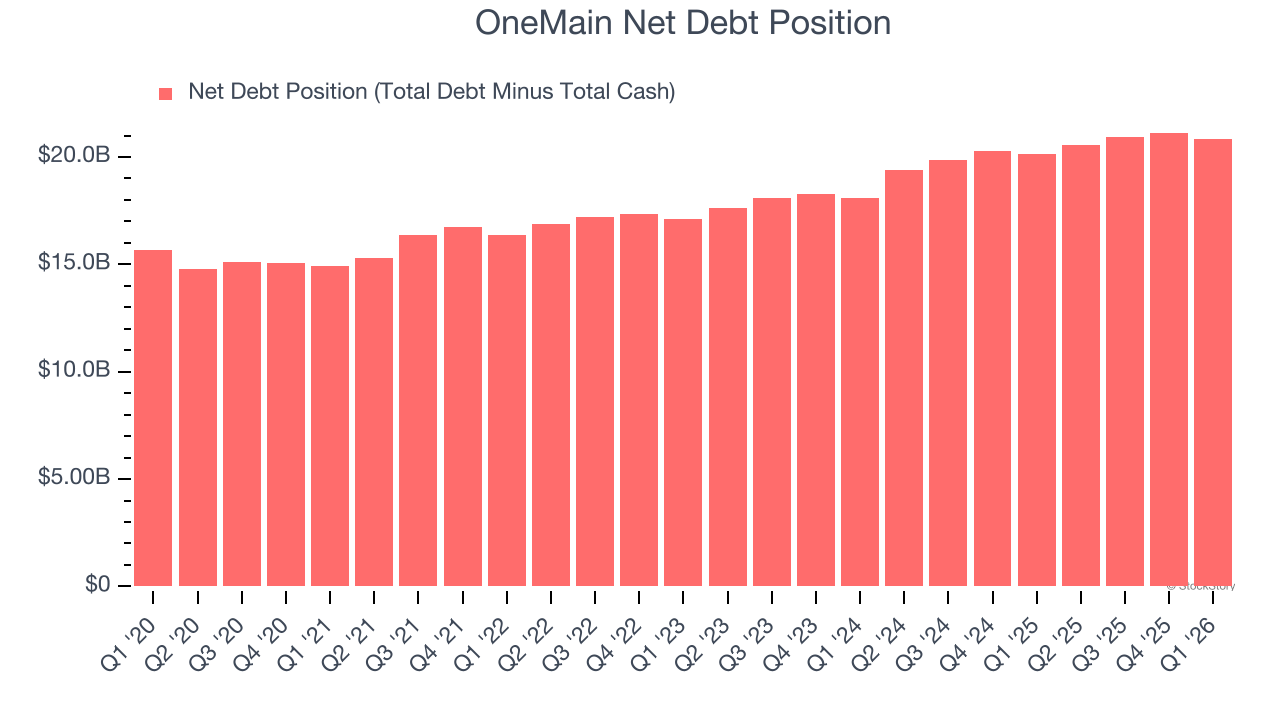

3. High Debt Levels Increase Risk

OneMain reported $1.56 billion of cash and $22.4 billion of debt on its balance sheet in the most recent quarter.

As investors in high-quality companies, we primarily focus on whether a company’s profits can support its debt.

With $1.40 billion of EBITDA over the last 12 months, we view OneMain’s 14.9× net-debt-to-EBITDA ratio as inadequate. The company’s lacking profits relative to its borrowings give it little breathing room, raising red flags.

Final Judgment

OneMain isn’t a terrible business, but it isn’t one of our picks. After the recent drawdown, the stock trades at 7.9× forward P/E (or $61.85 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We’re pretty confident there are superior stocks to buy right now. We’d suggest looking at one of our top digital advertising picks.

Stocks We Like More Than OneMain

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.