Over the past six months, Medpace’s shares (currently trading at $483.21) have posted a disappointing 11.2% loss while the S&P 500 was down 5.5%. This might have investors contemplating their next move.

Following the pullback, is now a good time to buy MEDP? Find out in our full research report, it’s free.

Why Do Investors Watch MEDP Stock?

Founded in 1992 as a scientifically-driven alternative to traditional contract research organizations, Medpace (NASDAQ: MEDP) provides outsourced clinical trial management and research services to help pharmaceutical, biotechnology, and medical device companies develop new treatments.

Three Things to Like:

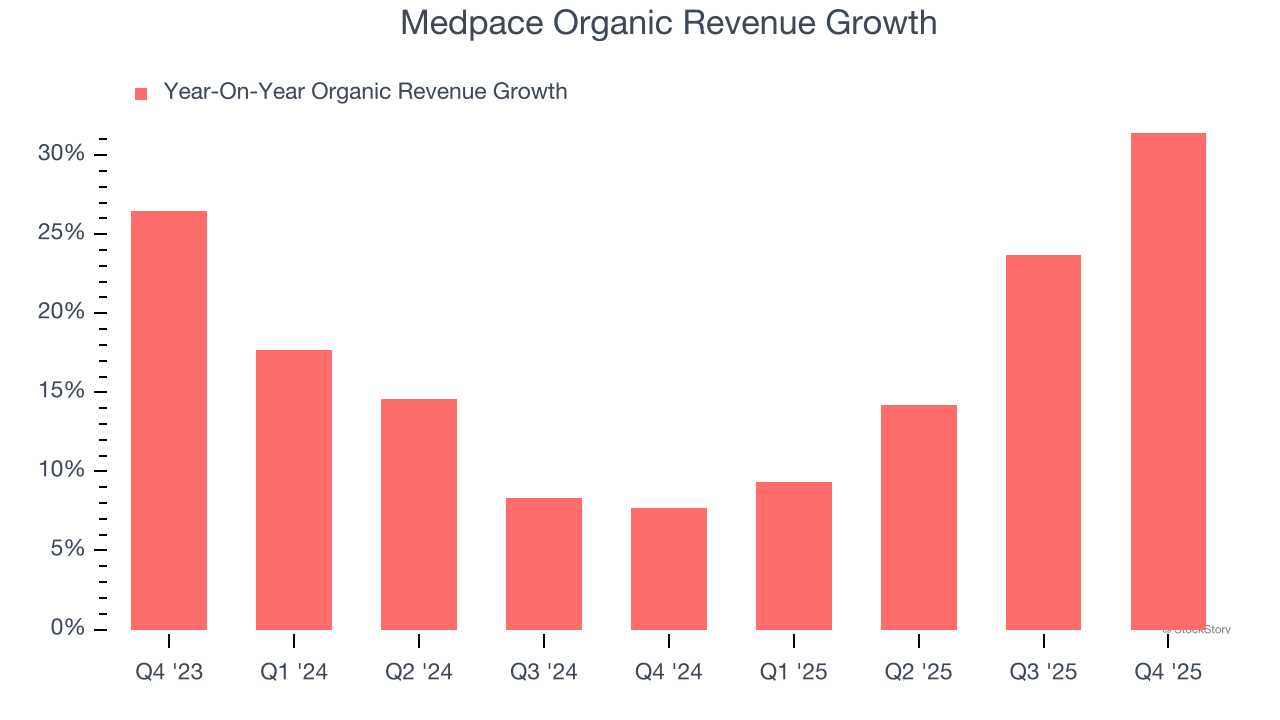

1. Core Business Firing on All Cylinders

In addition to reported revenue, organic revenue is a useful data point for analyzing Drug Development Inputs & Services companies. This metric gives visibility into Medpace’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Medpace’s organic revenue averaged 15.9% year-on-year growth. This performance was impressive and shows it can expand quickly without relying on expensive (and risky) acquisitions.

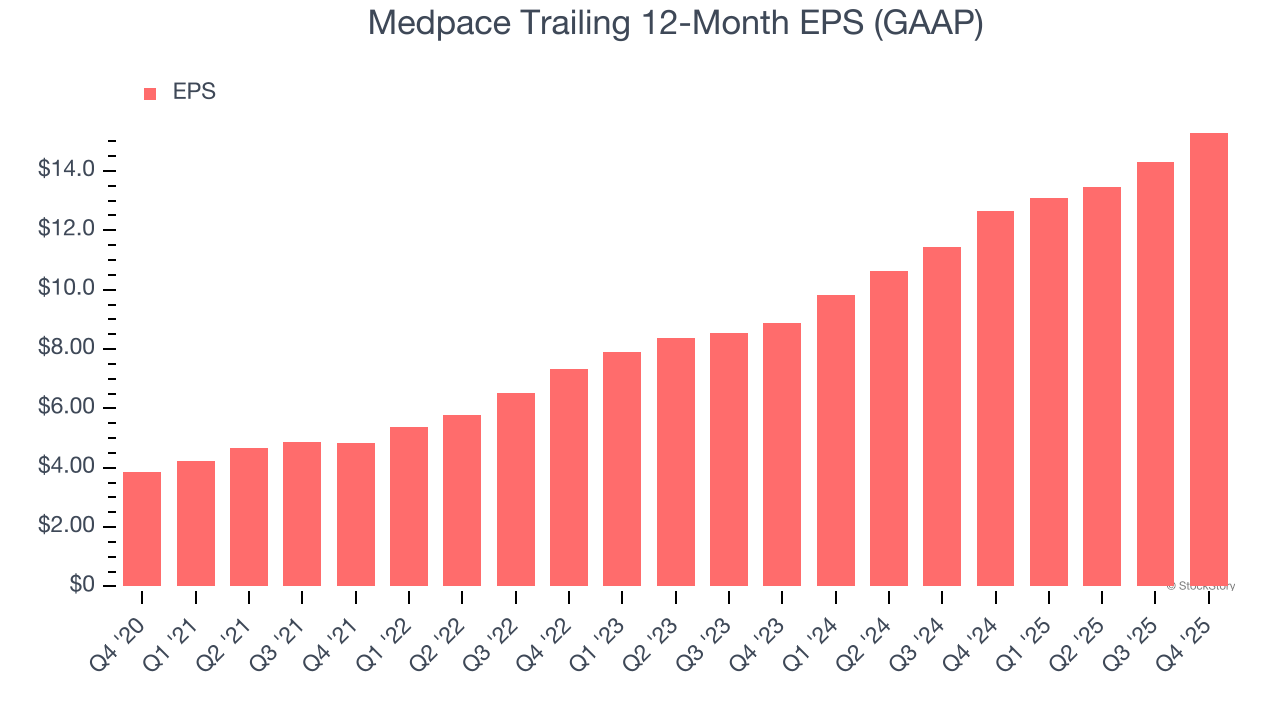

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Medpace’s EPS grew at 31.7% compounded annual growth rate over the last five years, higher than its 22.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

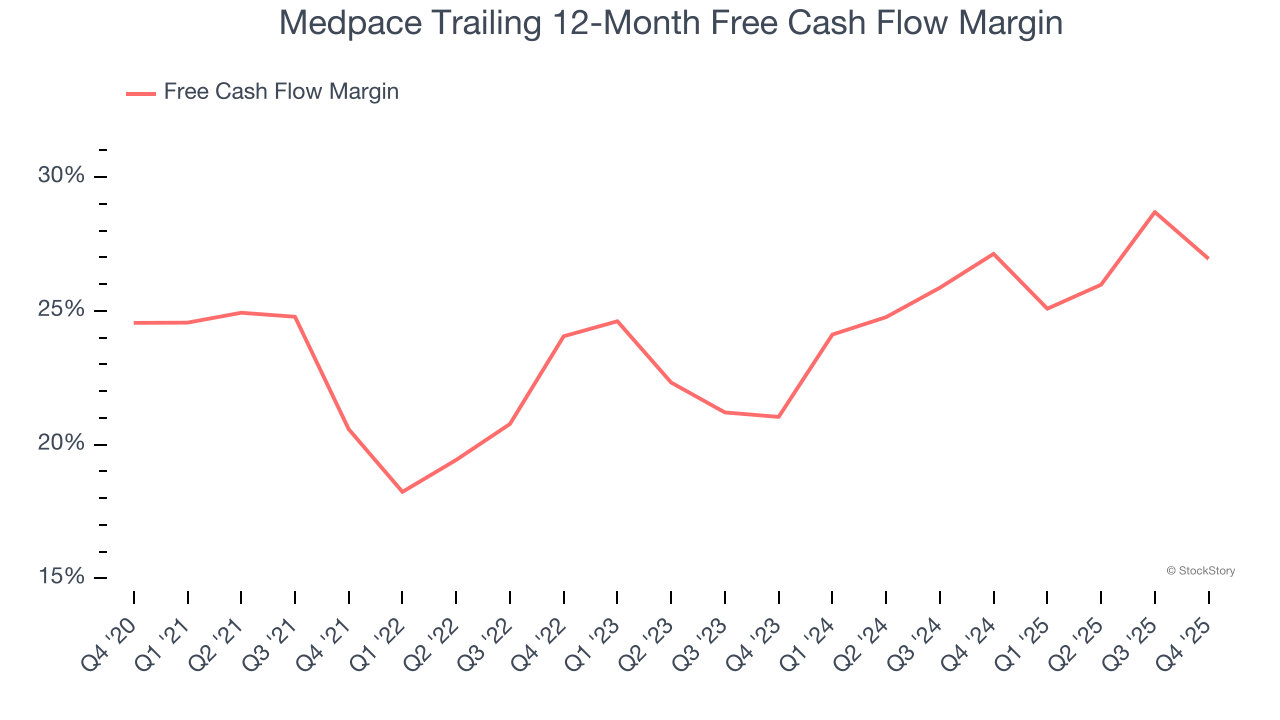

3. Increasing Free Cash Flow Margin Juices Financials

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Medpace’s margin expanded by 6.4 percentage points over the last five years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability. Medpace’s free cash flow margin for the trailing 12 months was 26.9%.

Final Judgment

Medpace is an interesting business with potential. With the recent decline, the stock trades at 26.4× forward P/E (or $483.21 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Medpace

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.