Conductive bags are becoming essential industrial packaging solutions, driven by semiconductor growth, ESD protection demand, compliance standards, and resilient supply chain expansion.

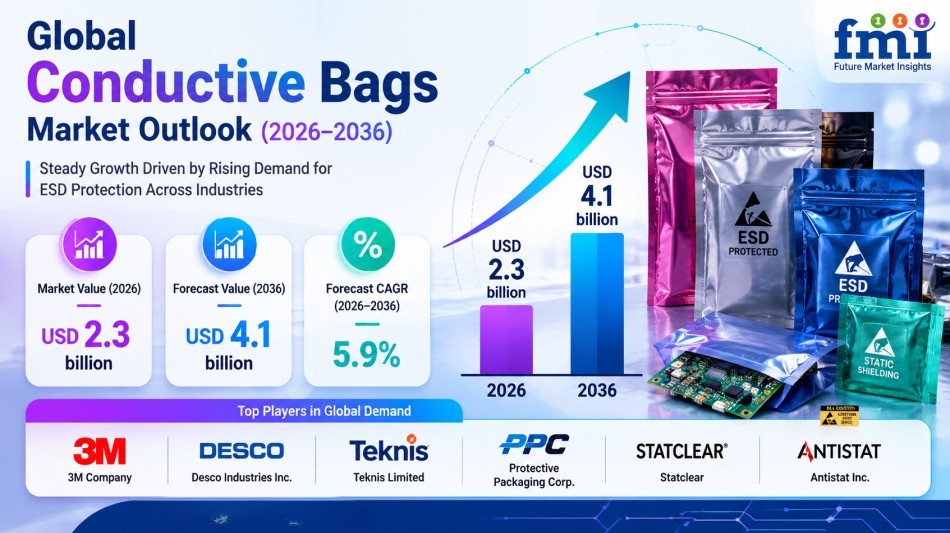

NEWARK, DE / ACCESS Newswire / May 25, 2026 / According to the latest market analysis by Future Market Insights, the conductive bags market is evolving from a niche protective packaging category into a critical component of industrial supply chains, particularly across electronics, semiconductors, automotive, and pharmaceutical equipment industries. Valued at USD 2.2 billion in 2025 and projected to reach USD 2.3 billion by 2026-end, the market is expected to expand at a CAGR of 5.9%, ultimately reaching USD 4.1 billion by 2036.

The market's growth reflects a broader industrial transition toward higher compliance standards, sensitive component protection, and localized manufacturing ecosystems designed to reduce operational risk and supply chain disruptions.

Quick Stats at a Glance

Market size (2025): USD 2.2 billion

Estimated value (2026): USD 2.3 billion

Forecast (2036): USD 4.1 billion

CAGR (2026-2036): 5.9%

Incremental opportunity: USD 1.8 billion

Leading product type: Plain conductive bags (41% share)

Dominant material segment: Aluminum Coated (56% share)

Leading growth market: Germany (6.8% CAGR)

Other key growth markets: USA (6.7%), South Korea (6.5%), UK (6.4%), Japan (6.3%)

Get detailed market forecasts, competitive benchmarking, and pricing trends:

https://www.futuremarketinsights.com/reports/sample/rep-gb-4792

Market Size and Structural Shift

The conductive bags market is entering a long-term expansion phase as industries increasingly prioritize electrostatic discharge (ESD) protection, moisture resistance, and contamination control across critical manufacturing environments.

Historically, conductive bags were treated as commodity packaging products with limited strategic importance. That perception is changing rapidly. As semiconductor miniaturization, advanced electronics manufacturing, and sensitive component logistics expand globally, conductive packaging is becoming essential infrastructure rather than optional protection.

Manufacturers are now investing in higher-specification conductive packaging solutions capable of meeting strict compliance standards while supporting operational continuity in increasingly automated and globally distributed supply chains.

Growth Drivers: Compliance, Electronics Expansion, and Industrial Reliability

Three major structural trends are accelerating market adoption globally.

1. Rising Semiconductor and Electronics Production

The rapid expansion of semiconductor fabrication, PCB manufacturing, and electronics assembly operations is significantly increasing demand for reliable ESD-safe packaging solutions.

Conductive bags play a critical role in protecting sensitive components during storage, transportation, and assembly processes.

2. Tightening Regulatory and Quality Standards

Global industries are facing stricter safety, environmental, and quality compliance requirements. Procurement teams increasingly prefer suppliers with strong certification portfolios, proven material reliability, and consistent product performance.

This trend particularly favors established manufacturers with integrated manufacturing and testing capabilities.

3. Regional Manufacturing Expansion

Governments and industrial sectors are accelerating investments in localized manufacturing infrastructure to reduce dependency on global supply chains.

As regional electronics and automotive manufacturing hubs expand, demand for locally sourced conductive packaging solutions is increasing alongside production capacity.

Market Constraints: Cost Pressure and Supply Chain Complexity

Despite strong long-term demand, the market faces operational and structural challenges.

Raw material price volatility remains a significant concern, particularly for aluminum-coated materials and specialty polymer films. Margin pressure is especially intense in commodity-grade product categories where low-cost producers dominate.

Supply chain concentration also creates operational risks. Manufacturers dependent on limited raw material suppliers or concentrated logistics networks remain vulnerable to disruptions, price spikes, and lead-time volatility.

At the same time, compliance requirements related to material sourcing, environmental standards, and safety certifications are increasing operational complexity across global supply chains.

Speak to Analyst: Customize insights for your business strategy:

https://www.futuremarketinsights.com/customization-available/rep-gb-4792

Opportunity Landscape: Where Future Value Is Emerging

Several high-value opportunities are shaping the next phase of conductive bags market expansion:

Expansion of semiconductor manufacturing capacity globally

Increasing demand for ESD-safe logistics and storage solutions

Growth of pharmaceutical equipment protection applications

Regionalized manufacturing and local sourcing strategies

Development of advanced moisture-barrier and shielding materials

Rising demand for reusable conductive packaging systems

The shift toward resilient and localized industrial ecosystems is expected to create sustained demand for suppliers with diversified production footprints and integrated manufacturing capabilities.

Segment Insights: Where the Market Is Concentrated

By Product Type:

Plain conductive bags are expected to dominate with a 41% market share in 2026, supported by broad industrial applicability, cost efficiency, and growing adoption across electronics and component storage applications.

Other product categories including tubing, grid, and bubble conductive bags continue expanding to address specialized packaging and protection requirements.

By Material:

Aluminum Coated materials are projected to hold 56% share of the market due to their superior electrostatic shielding, moisture barrier performance, and durability.

These materials are increasingly preferred for semiconductor packaging, PCB handling, and sensitive industrial component protection.

Regional Dynamics: Industrial Hubs Continue to Lead

Growth remains concentrated in industrial manufacturing economies with strong electronics, automotive, and advanced manufacturing ecosystems.

Germany (6.8% CAGR): Germany is expected to remain the leading growth market, supported by industrial automation expansion, precision manufacturing demand, and strong compliance-driven procurement standards.

United States (6.7% CAGR): The U.S. market continues benefiting from semiconductor investment, reshoring initiatives, and expanding advanced manufacturing infrastructure.

South Korea (6.5% CAGR): South Korea's leadership in semiconductor and electronics production continues driving demand for advanced ESD packaging solutions.

United Kingdom (6.4% CAGR): Industrial modernization and compliance-focused procurement are supporting steady market expansion across the UK manufacturing sector.

Japan (6.3% CAGR): Japan's high-value electronics manufacturing ecosystem continues to generate demand for precision protective packaging applications.

Unlock high-growth opportunities with FMI's niche business market insights:

https://www.futuremarketinsights.com/industry-analysis

Competitive Landscape: Reliability and Integration Becoming Decisive

The competitive environment is increasingly shifting beyond price competition toward operational reliability, manufacturing scale, and integrated product capabilities.

Leading companies including 3M Company, Desco Industries Inc., Teknis Limited, Protective Packaging Corp., Statclear, and Antistat Inc. are focusing on:

Integrated manufacturing capabilities

Multi-regional distribution networks

Product portfolio diversification

Technical differentiation and specialty applications

Long-term procurement relationships

Supply chain resilience and compliance management

For buyers, the priority is increasingly shifting toward dependable supply continuity, certification strength, and consistent product quality.

Strategic Implications for Industry Stakeholders

For manufacturers, competitive advantage will increasingly depend on balancing cost efficiency with technical specialization and regional production flexibility.

For procurement leaders, supplier selection criteria are evolving beyond pricing to include compliance reliability, sourcing diversification, and operational resilience.

For investors, recurring growth opportunities are emerging across specialized conductive materials, ESD protection technologies, and integrated industrial packaging ecosystems.

For industrial operators, conductive packaging is becoming a critical risk-management tool supporting product integrity, logistics efficiency, and manufacturing continuity.

Future Outlook: From Commodity Packaging to Strategic Infrastructure

Over the next decade, conductive bags are expected to transition from standard protective packaging products into essential components of advanced manufacturing ecosystems.

Key trends likely to shape the market include:

Expansion of semiconductor manufacturing investments

Increasing localization of industrial supply chains

Growth of reusable and sustainable packaging systems

Advanced multi-layer shielding technologies

Higher automation across industrial packaging workflows

Greater integration of compliance-driven procurement systems

As industrial sectors become increasingly dependent on sensitive electronics and precision manufacturing, conductive packaging will play a more strategic role across global value chains.

Executive Takeaways

Conductive bags are evolving into essential industrial protection infrastructure.

Semiconductor growth and ESD protection requirements are driving long-term demand.

Regulatory compliance and supply chain resilience are reshaping procurement priorities.

Aluminum coated materials continue dominating due to shielding and barrier performance.

Germany and the U.S. remain leading growth markets supported by industrial investment.

Competitive differentiation is increasingly tied to reliability, compliance, and manufacturing integration.

Future growth will be driven by localized production ecosystems and higher-value industrial applications.

Explore the Latest Packaging Industry Analysis Now:

https://www.futuremarketinsights.com/industry-analysis/packaging

Related Reports:

Conductive Polymer Packaging Market: https://www.futuremarketinsights.com/reports/conductive-polymer-packaging-market

Conductive Cardboard Market: https://www.futuremarketinsights.com/reports/conductive-cardboard-market

Polybags Market: https://www.futuremarketinsights.com/reports/polybags-market

Food Bags Market: https://www.futuremarketinsights.com/reports/food-bags-market

Paper Bags Market: https://www.futuremarketinsights.com/reports/paper-bags-market

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading provider of market intelligence and consulting services, serving clients in over 150 countries. Headquartered in Delaware, USA, with a global delivery center in India and offices in the UK and UAE, FMI delivers actionable insights to businesses across industries including automotive, technology, consumer products, manufacturing, energy, and chemicals.

An ESOMAR-certified research organization, FMI provides custom and syndicated market reports and consulting services, supporting both Fortune 1,000 companies and SMEs. Its team of 300+ experienced analysts ensures credible, data-driven insights to help clients navigate global markets and identify growth opportunities.

For Press & Corporate Inquiries

Rahul Singh

AVP - Marketing and Growth Strategy

Future Market Insights, Inc.

+91 8600020075

For Sales - sales@futuremarketinsights.com

For Media - Rahul.singh@futuremarketinsights.com

For Web - https://www.futuremarketinsights.com/

For Web - https://www.factmr.com/

SOURCE: Future Market Insights, Inc.

View the original press release on ACCESS Newswire