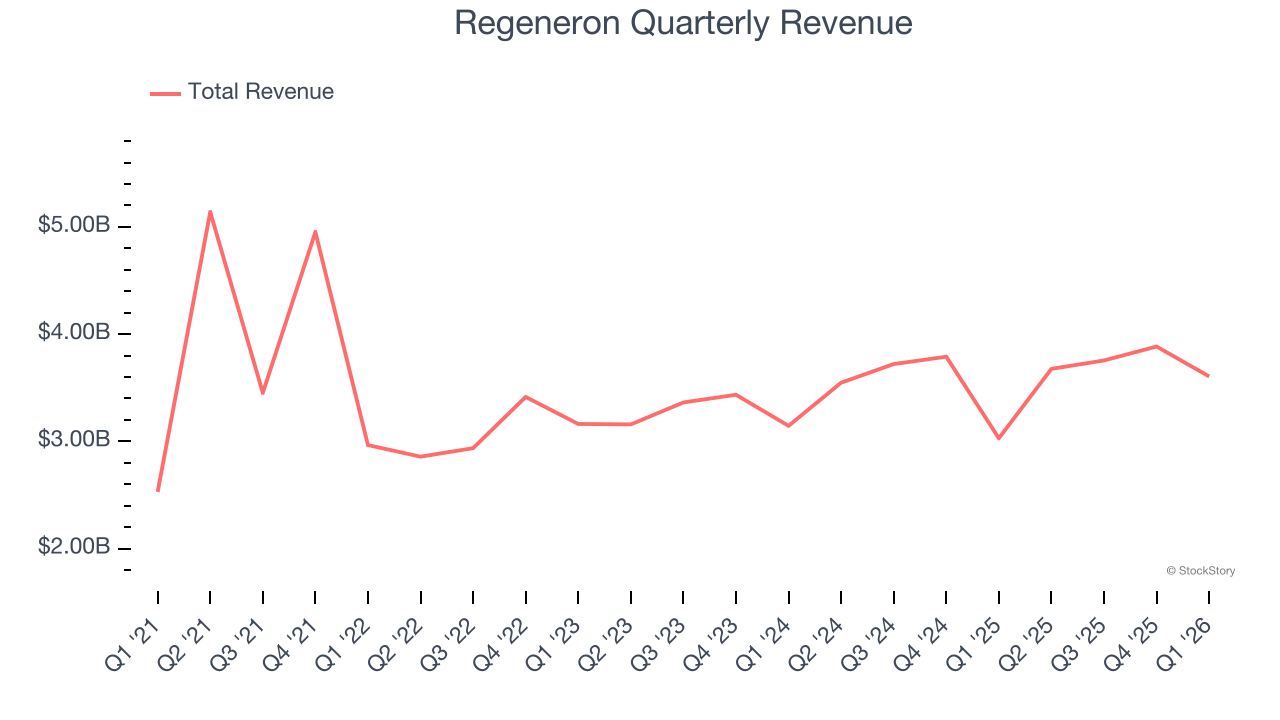

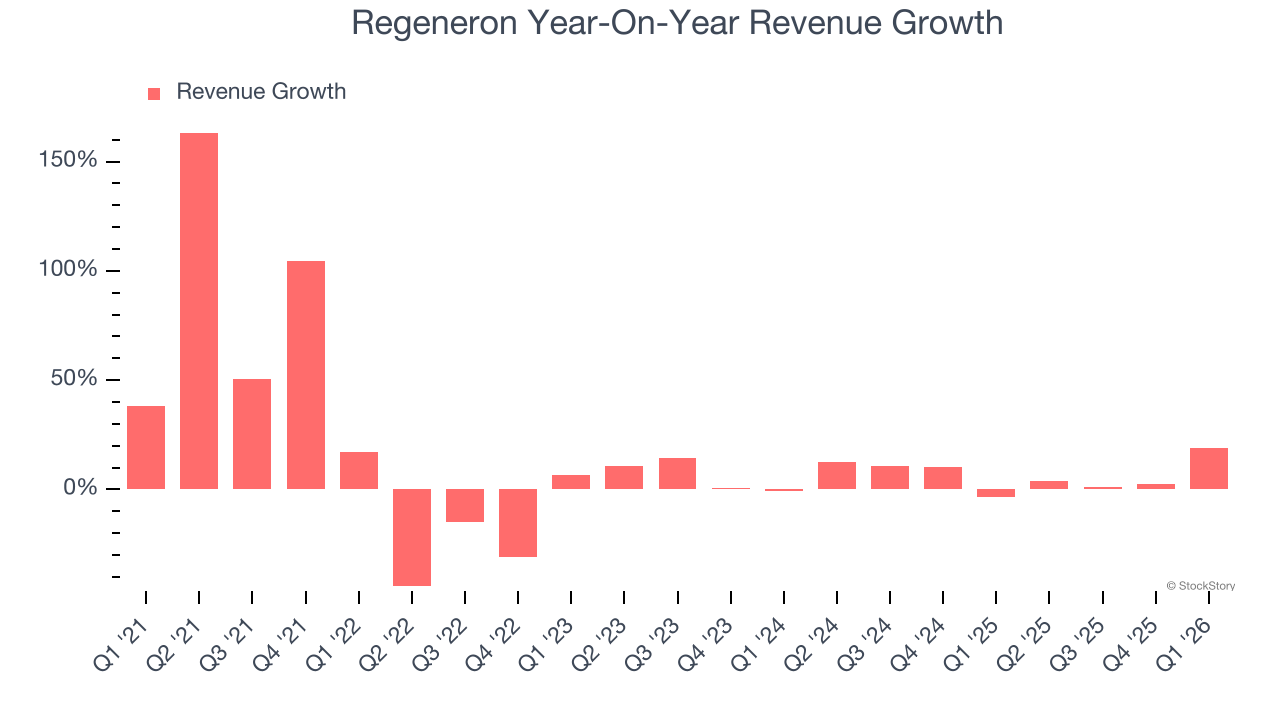

Biotech company Regeneron (NASDAQ: REGN) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 19% year on year to $3.61 billion. Its non-GAAP profit of $9.47 per share was 6.4% above analysts’ consensus estimates.

Is now the time to buy Regeneron? Find out by accessing our full research report, it’s free.

Regeneron (REGN) Q1 CY2026 Highlights:

- Revenue: $3.61 billion vs analyst estimates of $3.47 billion (19% year-on-year growth, 3.8% beat)

- Adjusted EPS: $9.47 vs analyst estimates of $8.90 (6.4% beat)

- Adjusted Operating Income: $642.9 million vs analyst estimates of $951.4 million (17.8% margin, 32.4% miss)

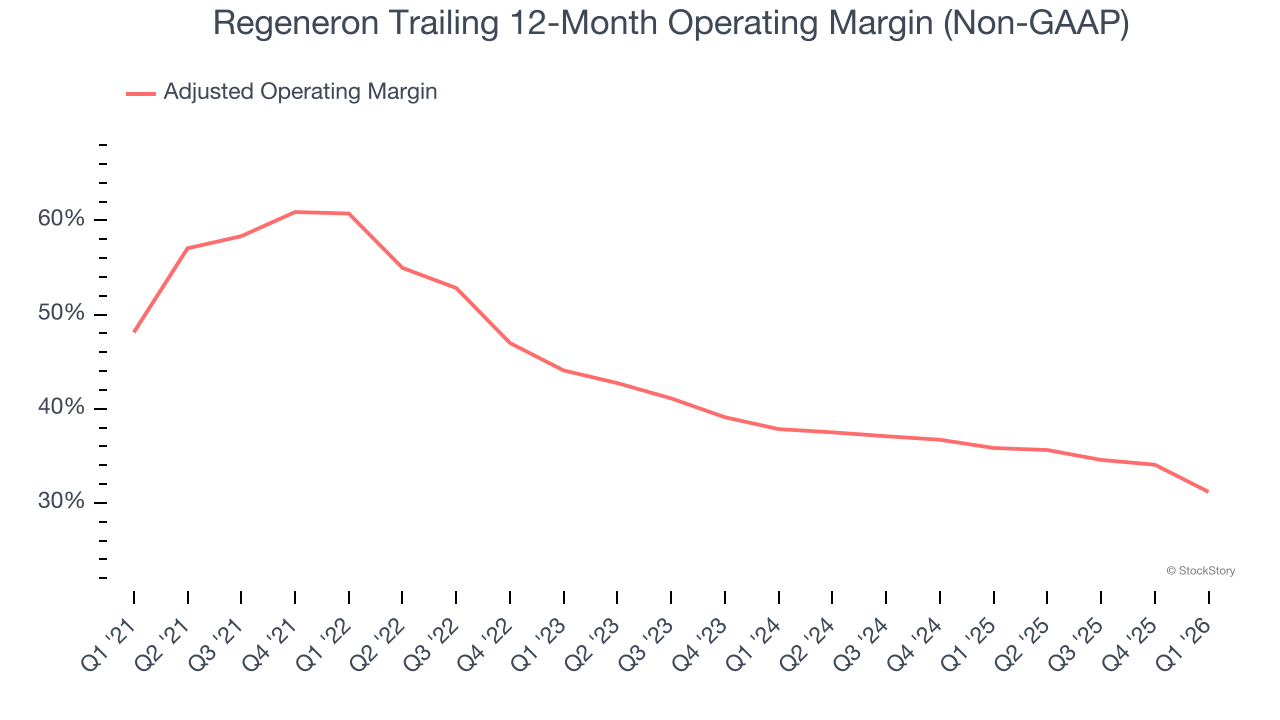

- Operating Margin: 17.8%, down from 19.5% in the same quarter last year

- Free Cash Flow Margin: 23.5%, down from 26.9% in the same quarter last year

- Market Capitalization: $74.45 billion

"In the first quarter of this year, we were able to achieve strong double-digit growth on both the top and bottom line while continuing to invest significant resources in our portfolio of nearly 50 product candidates in clinical development," said Leonard S. Schleifer, M.D., Ph.D., Board co-Chair, President and Chief Executive Officer of Regeneron.

Company Overview

Founded by scientists who wanted to build a company where science could thrive, Regeneron Pharmaceuticals (NASDAQ: REGN) develops and commercializes medicines for serious diseases, with key products treating eye conditions, allergic diseases, cancer, and other disorders.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Regeneron’s 10.2% annualized revenue growth over the last five years was decent. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Regeneron’s recent performance shows its demand has slowed as its annualized revenue growth of 6.7% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

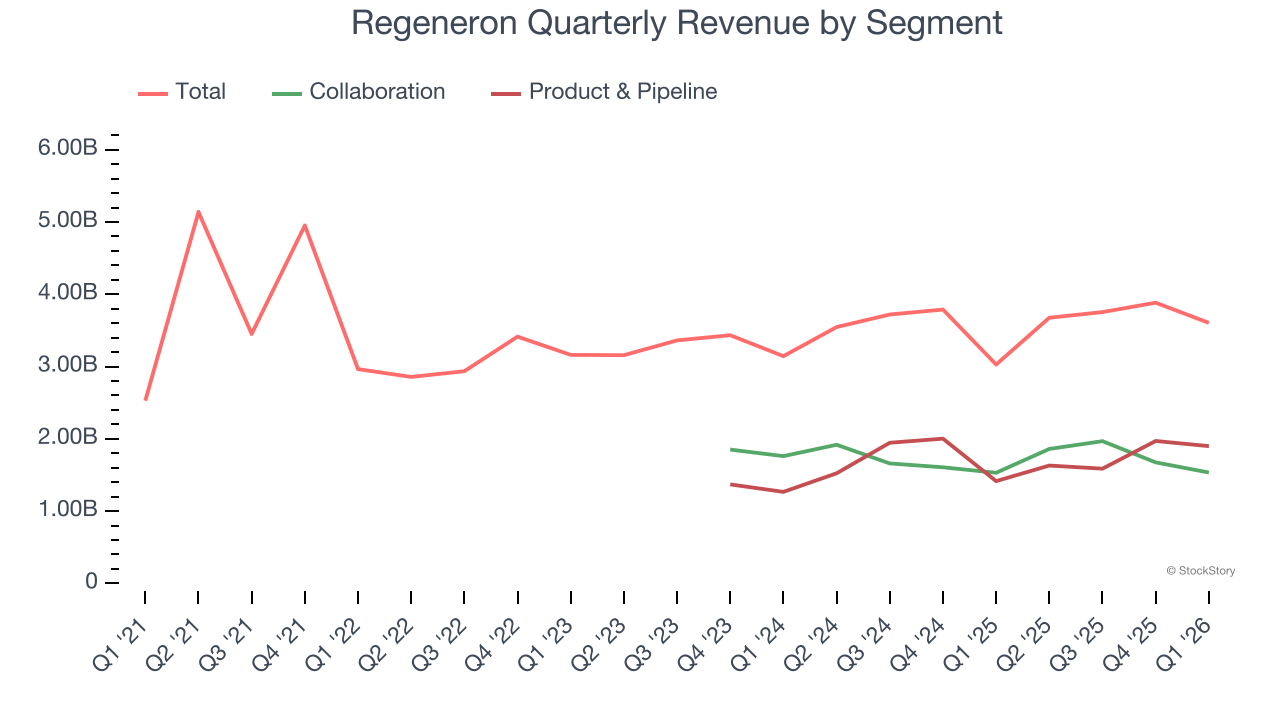

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Collaboration and Product & Pipeline, which are 42.6% and 52.7% of revenue. Over the last two years, Regeneron’s Collaboration revenue averaged 1% year-on-year declines. On the other hand, its Product & Pipeline revenue averaged 13.2% growth.

This quarter, Regeneron reported year-on-year revenue growth of 19%, and its $3.61 billion of revenue exceeded Wall Street’s estimates by 3.8%.

Looking ahead, sell-side analysts expect revenue to grow 9.5% over the next 12 months, an improvement versus the last two years. This projection is particularly healthy for a company of its scale and indicates its newer products and services will fuel better top-line performance.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Adjusted Operating Margin

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

Regeneron has been a well-oiled machine over the last five years. It demonstrated elite profitability for a healthcare business, boasting an average adjusted operating margin of 42.4%.

Looking at the trend in its profitability, Regeneron’s adjusted operating margin decreased by 29.6 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 6.7 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Regeneron generated an adjusted operating margin profit margin of 17.8%, down 11.1 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

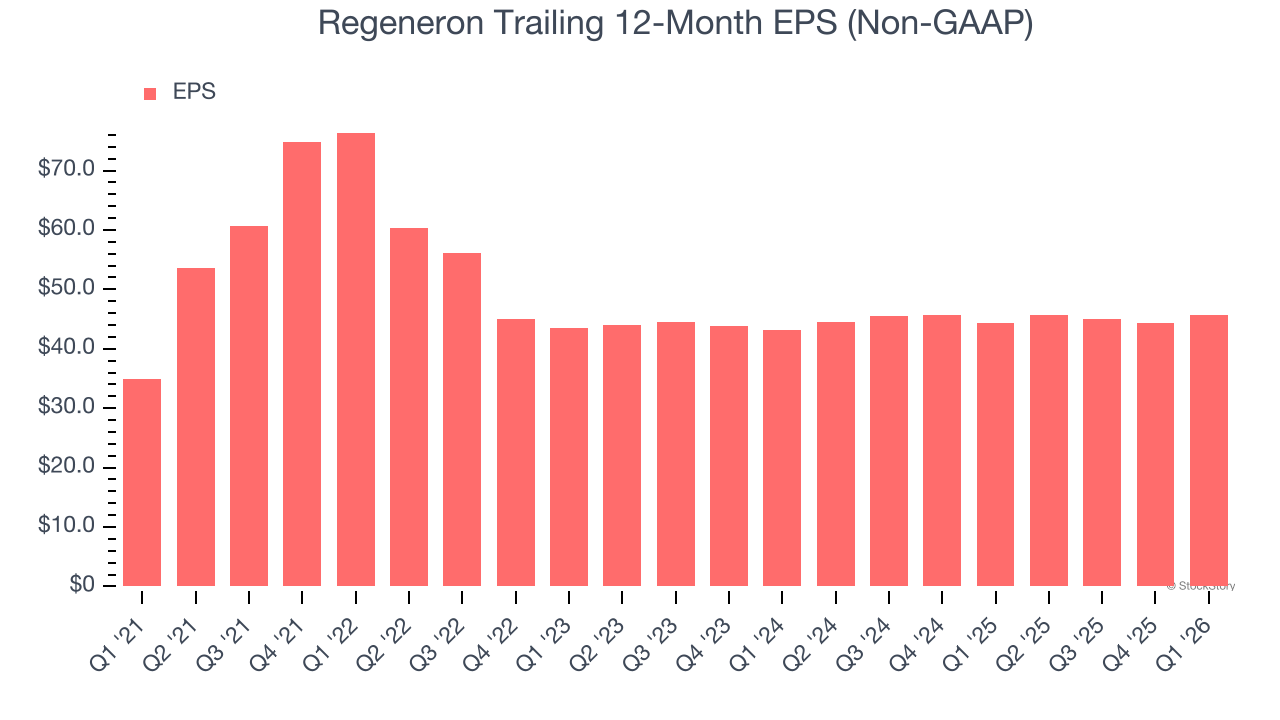

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Regeneron’s EPS grew at a decent 5.5% compounded annual growth rate over the last five years. However, this performance was lower than its 10.2% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

We can take a deeper look into Regeneron’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Regeneron’s adjusted operating margin declined by 29.6 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, Regeneron reported adjusted EPS of $9.47, up from $8.22 in the same quarter last year. This print beat analysts’ estimates by 6.4%. Over the next 12 months, Wall Street expects Regeneron’s full-year EPS of $45.63 to grow 6.6%.

Key Takeaways from Regeneron’s Q1 Results

We enjoyed seeing Regeneron beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock remained flat at $737.15 immediately following the results.

Indeed, Regeneron had a rock-solid quarterly earnings result, but is this stock a good investment here? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).