The end of the earnings season is always a good time to take a step back and see who shined (and who not so much). Let’s take a look at how payment processing stocks fared in Q4, starting with EVERTEC (NYSE: EVTC).

Payment processors facilitate transactions between merchants, consumers, and financial institutions. Growth comes from e-commerce expansion, declining cash usage globally, and value-added services beyond basic processing. Headwinds include margin pressure from merchant negotiating power, rapid technological change requiring investment, and emerging competition from technology companies entering the payments ecosystem.

The 4 payment processing stocks we track reported a satisfactory Q4. As a group, revenues beat analysts’ consensus estimates by 1.1% while next quarter’s revenue guidance was 49.7% below.

While some payment processing stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 2.1% since the latest earnings results.

Best Q4: EVERTEC (NYSE: EVTC)

Operating one of Latin America's leading PIN debit networks called ATH, EVERTEC (NYSE: EVTC) is a payment transaction processor and financial technology provider that enables merchants and financial institutions across Latin America and the Caribbean to accept and process electronic payments.

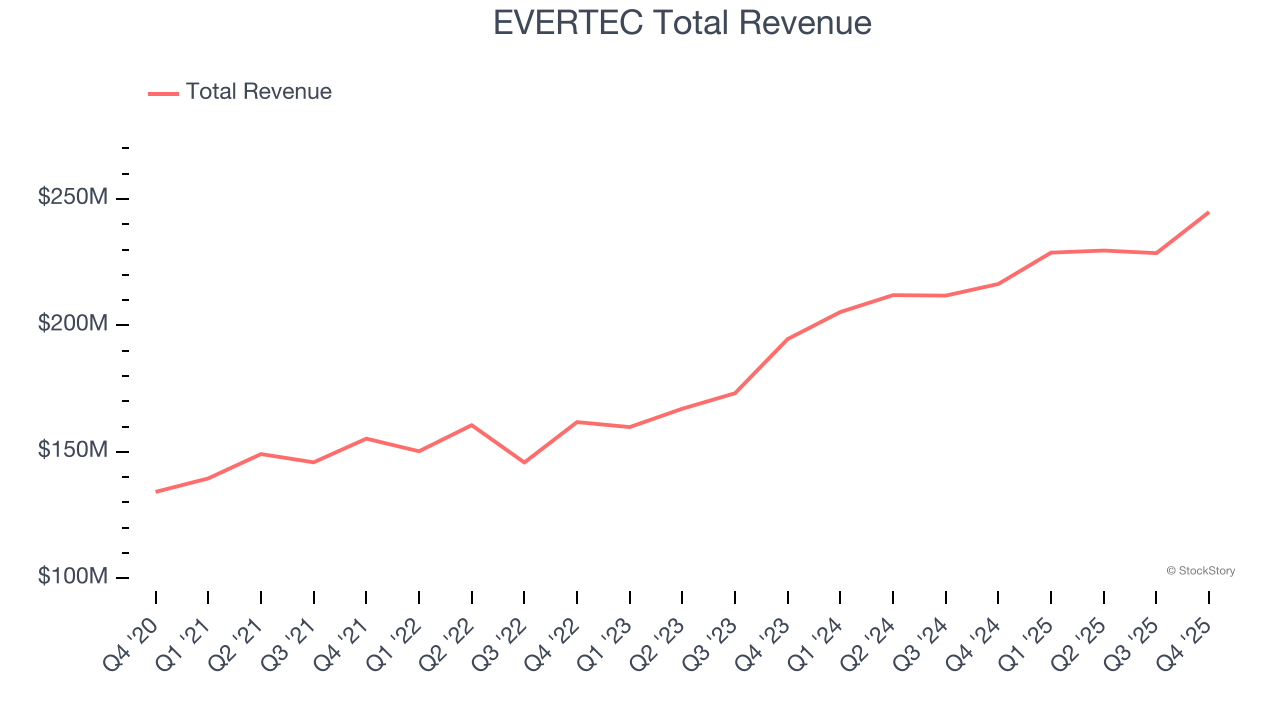

EVERTEC reported revenues of $244.8 million, up 13.1% year on year. This print exceeded analysts’ expectations by 3.3%. Overall, it was a very strong quarter for the company with full-year revenue guidance exceeding analysts’ expectations and full-year EPS guidance exceeding analysts’ expectations.

EVERTEC scored the biggest analyst estimates beat and highest full-year guidance raise of the whole group. Unsurprisingly, the stock is up 15% since reporting and currently trades at $29.65.

We think EVERTEC is a good business, but is it a buy today? Read our full report here, it’s free.

Jack Henry (NASDAQ: JKHY)

Founded in 1976 by two entrepreneurs who saw the need for specialized banking software in the early days of financial computing, Jack Henry & Associates (NASDAQ: JKHY) provides technology solutions that help banks and credit unions innovate, differentiate, and compete while serving the evolving needs of their accountholders.

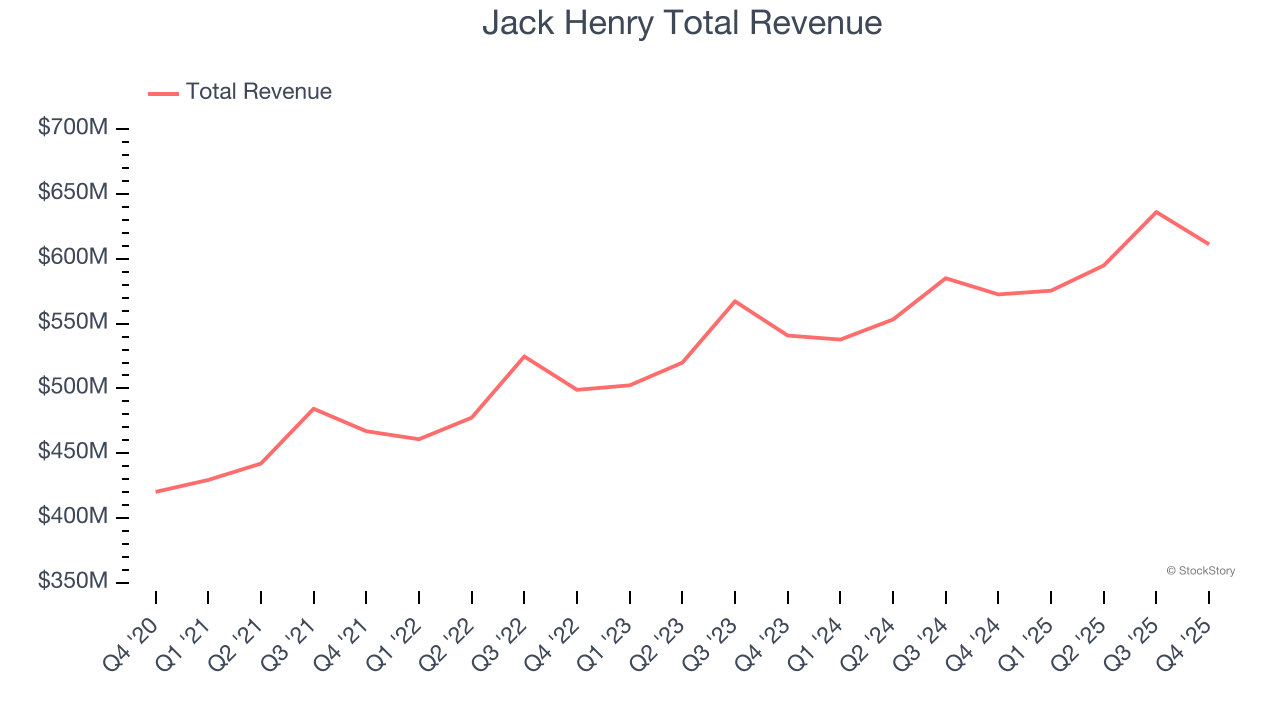

Jack Henry reported revenues of $611.2 million, up 6.7% year on year, outperforming analysts’ expectations by 1.3%. The business had a very strong quarter with a beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $166.63.

Is now the time to buy Jack Henry? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Shift4 (NYSE: FOUR)

Starting as a payment gateway provider in 1999 and now processing over $200 billion in annual payment volume, Shift4 Payments (NYSE: FOUR) provides integrated payment processing solutions and software that help businesses accept and manage transactions across in-store, online, and mobile channels.

Shift4 reported revenues of $1.19 billion, up 34% year on year, in line with analysts’ expectations. It was a softer quarter as it posted full-year revenue guidance missing analysts’ expectations significantly and full-year EPS guidance meeting analysts’ expectations.

Shift4 delivered the fastest revenue growth but had the weakest full-year guidance update in the group. As expected, the stock is down 20% since the results and currently trades at $45.91.

Read our full analysis of Shift4’s results here.

Fiserv (NASDAQ: FISV)

Powering over 1 billion accounts and processing more than 12,000 financial transactions per second globally, Fiserv (NASDAQ: FISV) provides payment processing and financial technology solutions that enable merchants, banks, and credit unions to accept payments and manage financial transactions.

Fiserv reported revenues of $4.9 billion, flat year on year. This print was in line with analysts’ expectations. More broadly, it was a mixed quarter as it also logged a decent beat of analysts’ EBITDA estimates but full-year EPS guidance meeting analysts’ expectations.

Fiserv had the weakest performance against analyst estimates and slowest revenue growth among its peers. The stock is down 3.6% since reporting and currently trades at $58.

Read our full, actionable report on Fiserv here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.