Central Garden & Pet trades at $39.25 per share and has stayed right on track with the overall market, gaining 8.5% over the last six months. At the same time, the S&P 500 has returned 7.2%.

Is now the time to buy Central Garden & Pet, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Central Garden & Pet Will Underperform?

We don't have much confidence in Central Garden & Pet. Here are three reasons we avoid CENT and a stock we'd rather own.

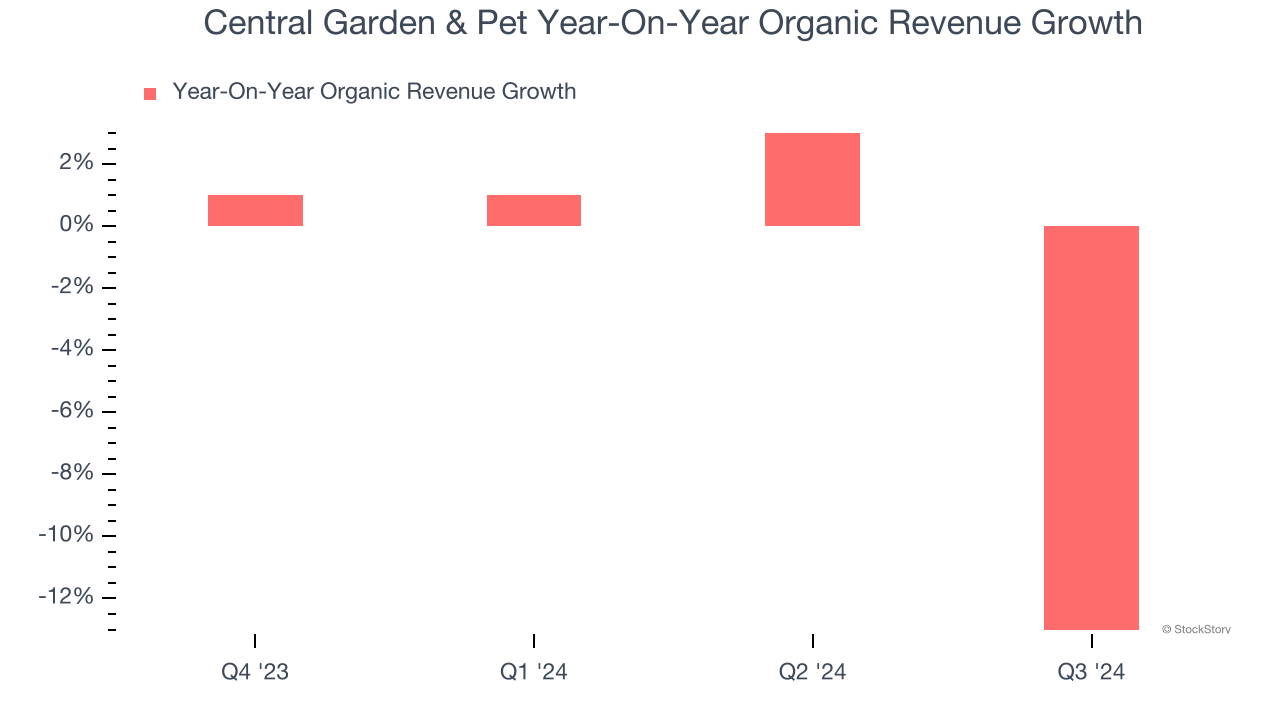

1. Core Business Falling Behind as Organic Sales Decline

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

Central Garden & Pet’s demand has been falling over the last eight quarters, and on average, its organic sales have declined by 3% year on year.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Central Garden & Pet’s revenue to rise by 1.1%. Although this projection indicates its newer products will spur better top-line performance, it is still below the sector average.

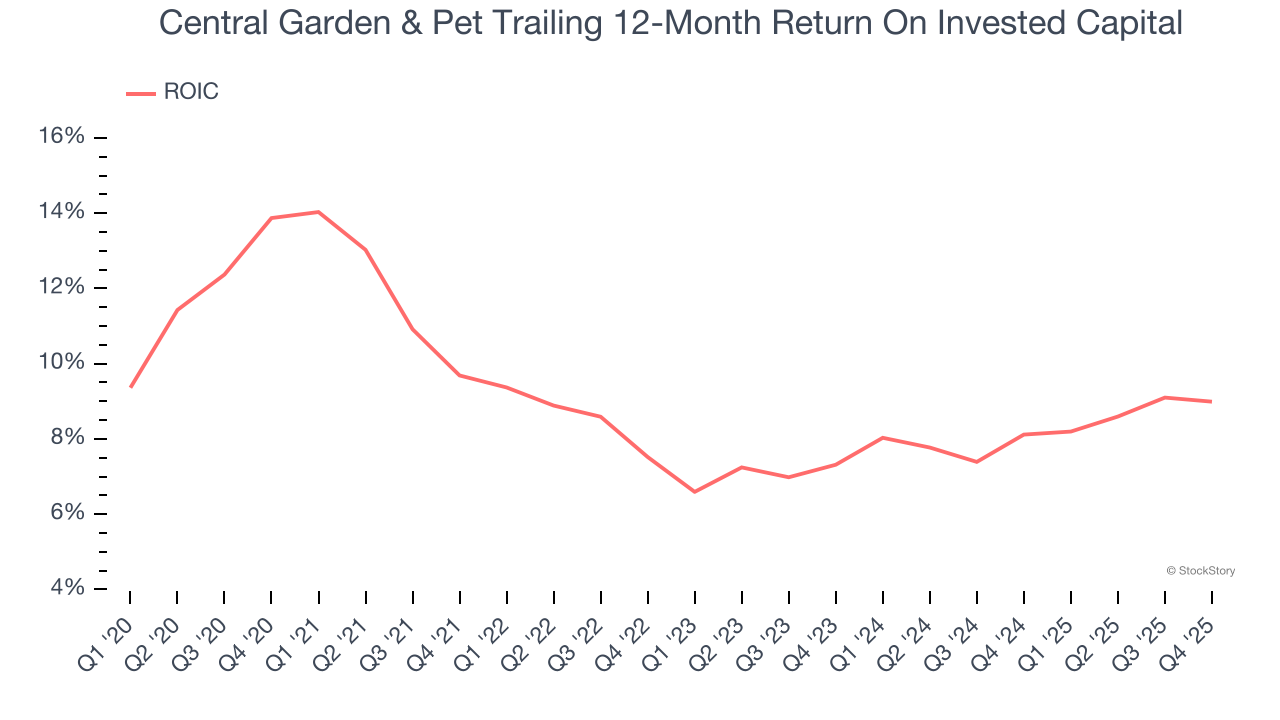

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Central Garden & Pet historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 8.3%, somewhat low compared to the best consumer staples companies that consistently pump out 20%+.

Final Judgment

Central Garden & Pet doesn’t pass our quality test. That said, the stock currently trades at 14.1× forward P/E (or $39.25 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are better stocks to buy right now. We’d recommend looking at an all-weather company that owns household favorite Taco Bell.

Stocks We Like More Than Central Garden & Pet

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.