Retirement solutions provider Jackson Financial (NYSE: JXN) missed Wall Street’s revenue expectations in Q2 CY2025, with sales falling 127% year on year to -$471 million due to large losses on derivatives and investments. Its non-GAAP profit of $4.87 per share was 5% above analysts’ consensus estimates.

Is now the time to buy Jackson Financial? Find out by accessing our full research report, it’s free.

Jackson Financial (JXN) Q2 CY2025 Highlights:

- Net Premiums Earned: $40 million (98% year-on-year decline)

- Revenue: -$471 million vs analyst estimates of $1.75 billion (127% year-on-year decline due to large losses on derivatives and investments, 127% miss)

- Pre-Tax Profit Margin: -40.1% (58.5 percentage point year-on-year decrease)

- Adjusted EPS: $4.87 vs analyst estimates of $4.64 (5% beat)

- Market Capitalization: $6.05 billion

Laura Prieskorn, President and Chief Executive Officer of Jackson, stated, “Our second quarter results underscore the continued strength of our business and our steady progress toward achieving strategic objectives. We delivered another quarter of year-over-year growth in retail annuity sales, driven by our well-diversified product portfolio which now includes our recently launched Jackson Market Link Pro® III and Jackson Market Link Pro Advisory® III. Our robust in-force book generated free cash flow of $290 million for the quarter—significantly surpassing the $229 million generated during the second quarter of 2024—and exceeded $1 billion over the twelve months ended June 30, 2025. We also returned $216 million to common shareholders, maintained an estimated RBC ratio well above our target, and further strengthened our already substantial excess cash position at the holding company. We are confident in our ability to sustain this positive momentum throughout 2025 as we continue to help Americans secure their financial futures.”

Company Overview

Spun off from British insurer Prudential plc in 2021 after more than 60 years as its U.S. subsidiary, Jackson Financial (NYSE: JXN) offers annuity products and retirement solutions that help Americans grow and protect their retirement savings and income.

Revenue Growth

Big picture, insurers generate revenue from three key sources. The first is the core business of underwriting policies. The second source is income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities. The third is fees from various sources such as policy administration, annuities, or other value-added services.

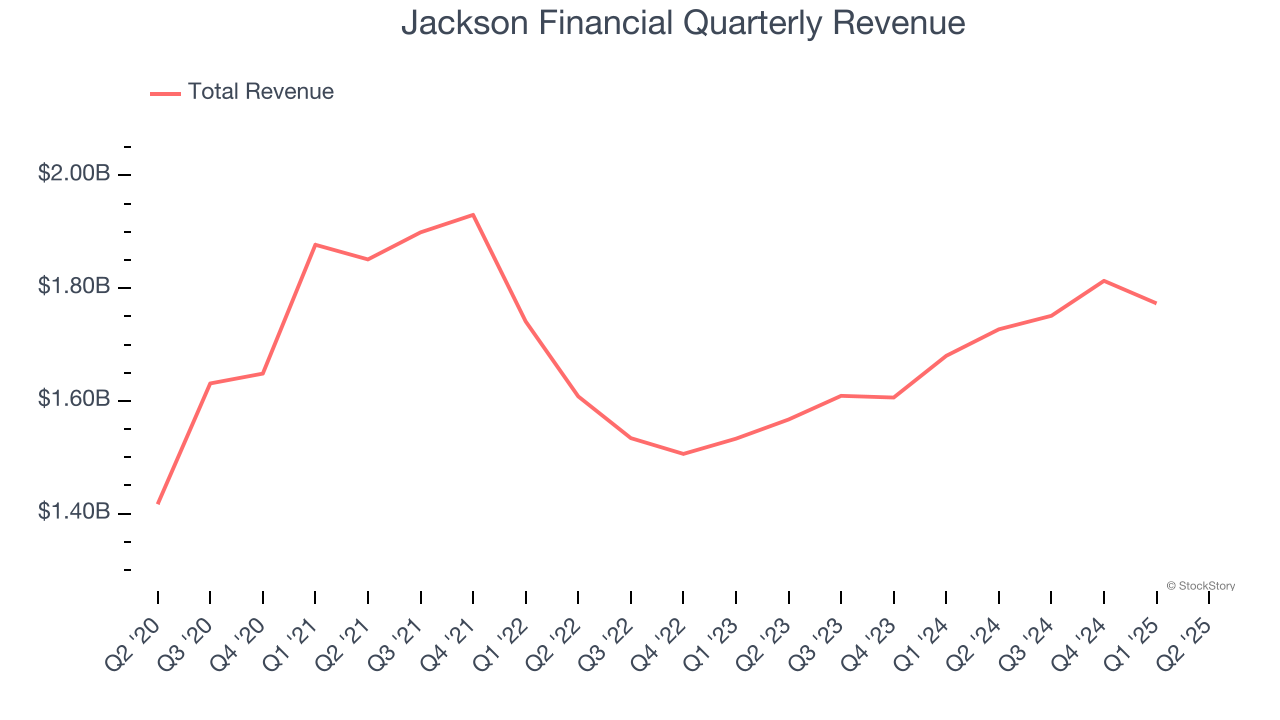

Unfortunately, Jackson Financial struggled to consistently increase demand as its $4.87 billion of revenue for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and suggests it’s a lower quality business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

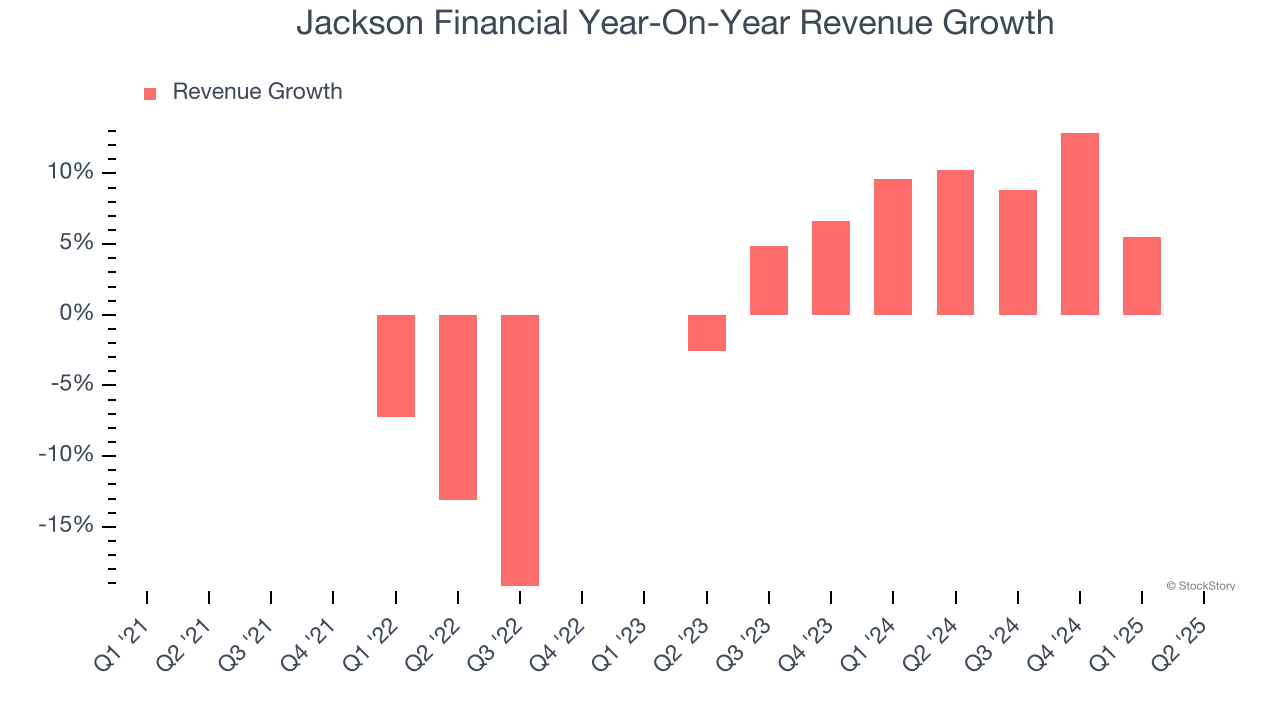

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Jackson Financial’s annualized revenue growth of 8% over the last two years is above its five-year trend, suggesting some bright spots.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Jackson Financial missed Wall Street’s estimates and reported a rather uninspiring 127% year-on-year revenue decline, generating -$471 million of revenue.

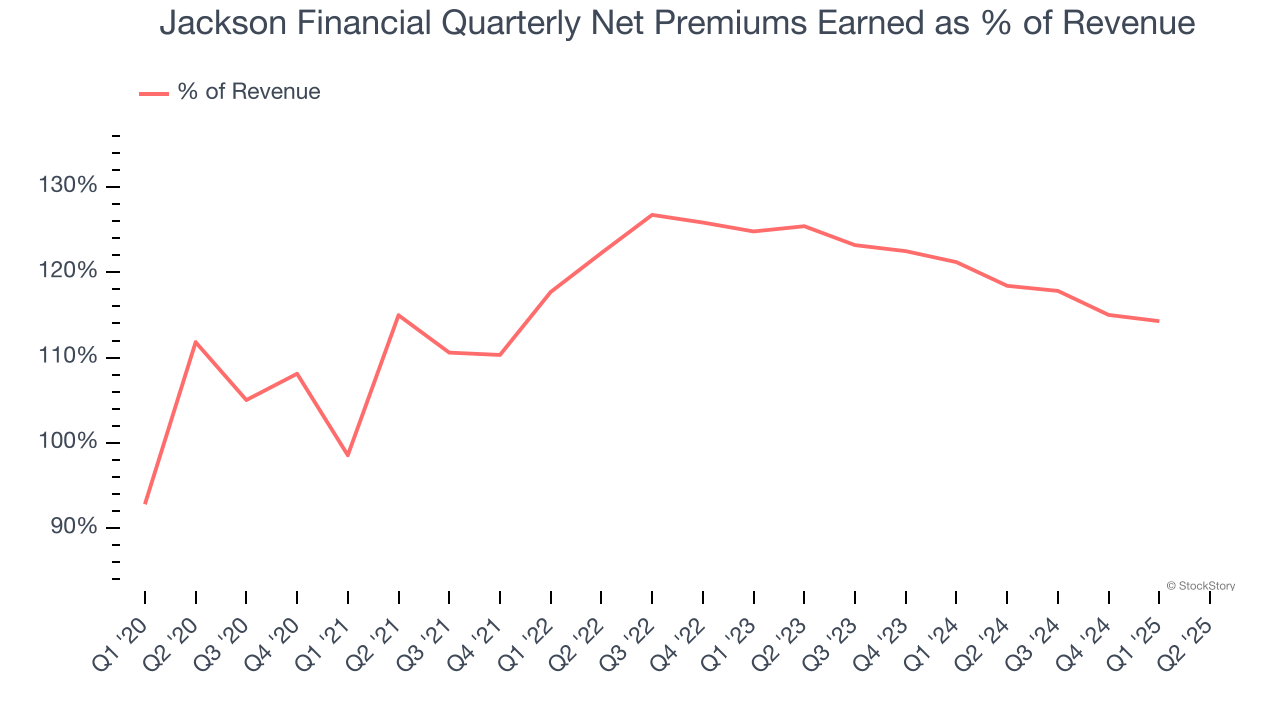

Since the company recorded losses on certain securities, it generated more net premiums earned than revenue (a 1.2x multiple of its revenue to be exact) during the last five years, meaning Jackson Financial lives and dies by its underwriting activities because non-insurance operations barely move the needle.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.Net premiums earned commands greater market attention due to its reliability and consistency, whereas investment and fee income are often seen as more volatile revenue streams that fluctuate with market conditions.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Net Premiums Earned

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are therefore net of what’s ceded to reinsurers as a risk mitigation and transfer strategy.

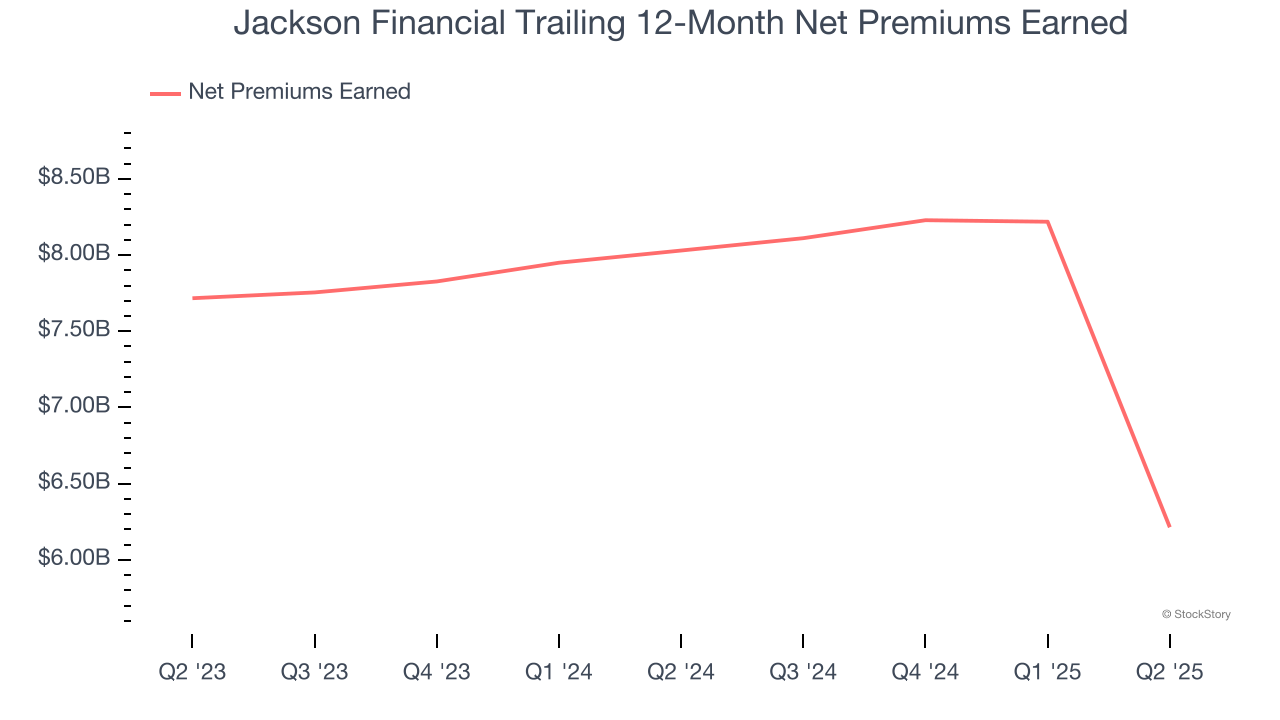

Jackson Financial’s net premiums earned has declined by 8.8% annually over the last five years, much worse than the broader insurance industry. This shows that policy underwriting underperformed its other business lines.

When analyzing Jackson Financial’s net premiums earned over the last two years, we can see its woes have continued as income dropped by 10.3% annually. Since two-year net premiums earned underperformed total revenue over this period, it’s implied that insurance policies were a detractor of consolidated growth.

In Q2, Jackson Financial produced $40 million of net premiums earned, down 98% year on year.

Key Takeaways from Jackson Financial’s Q2 Results

We struggled to find many positives in these results. Overall, this was a weaker quarter. The stock remained flat at $86.33 immediately following the results.

Jackson Financial didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.