Workforce solutions provider ManpowerGroup (NYSE: MAN) reported Q2 CY2025 results exceeding the market’s revenue expectations, but sales were flat year on year at $4.52 billion. Its GAAP loss of $1.44 per share was significantly below analysts’ consensus estimates.

Is now the time to buy ManpowerGroup? Find out by accessing our full research report, it’s free.

ManpowerGroup (MAN) Q2 CY2025 Highlights:

- Revenue: $4.52 billion vs analyst estimates of $4.36 billion (flat year on year, 3.6% beat)

- EPS (GAAP): -$1.44 vs analyst estimates of $0.70 (significant miss)

- Adjusted EBITDA: $4.6 million vs analyst estimates of $95.93 million (0.1% margin, 95.2% miss)

- EPS (GAAP) guidance for Q3 CY2025 is $0.82 at the midpoint, beating analyst estimates by 10.5%

- Operating Margin: -0.6%, down from 2.2% in the same quarter last year

- Free Cash Flow was -$207.2 million compared to -$149.8 million in the same quarter last year

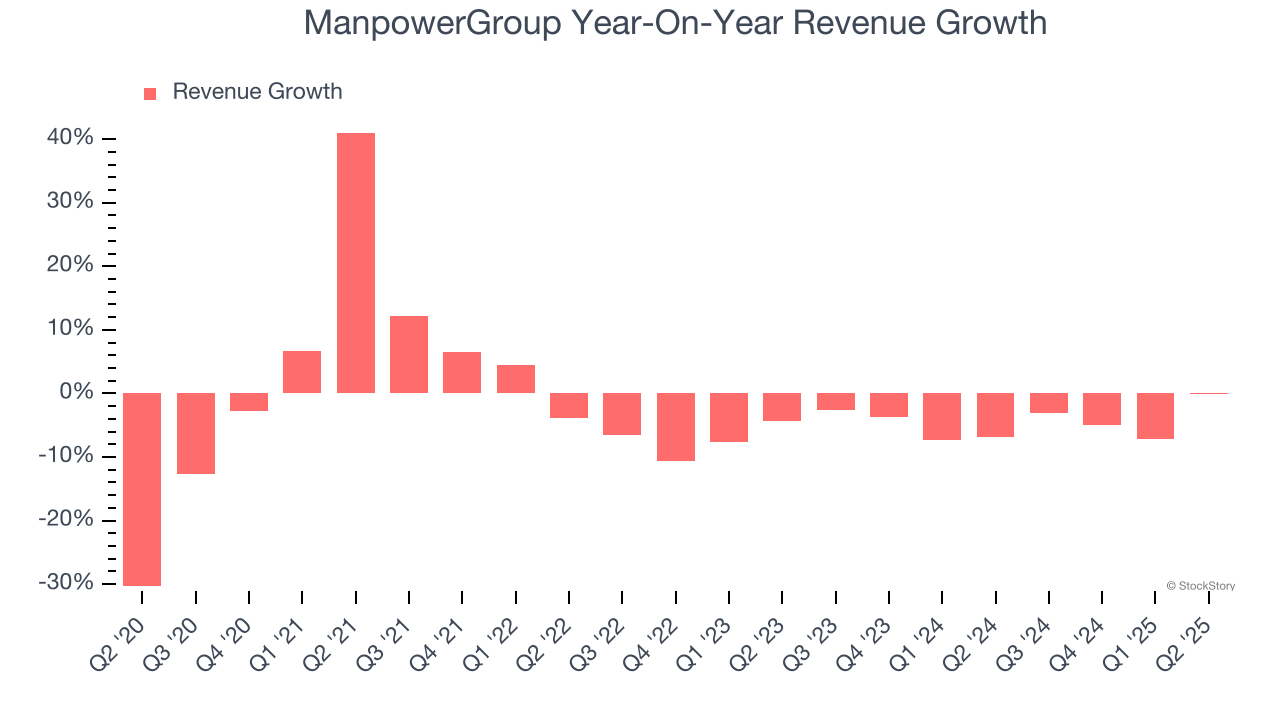

- Organic Revenue fell 1% year on year (-3.3% in the same quarter last year)

- Market Capitalization: $1.99 billion

Jonas Prising, ManpowerGroup Chair & CEO, said "During the quarter, we continued to make strong progress in executing our plans to Diversify, Digitize and Innovate – with a focus on expanding our role as the strategic workforce partner of choice for our clients as tech transformation gathers pace. Although demand remains mixed across our global markets as employers adapt to economic and geopolitical volatility, we are beginning to see positive signs of stabilization in the US and parts of Europe. We remain focused on achieving market share gains while we make further adjustments to our cost base. Our ongoing investments in strengthening our digital core to accelerate AI adoption will ensure we are well positioned to accelerate progress and provide even more value to clients and candidates in future quarters."

Company Overview

Founded during the post-World War II economic boom when businesses needed temporary workers, ManpowerGroup (NYSE: MAN) connects millions of people to employment opportunities through its global network of staffing, recruitment, and workforce management services.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $17.54 billion in revenue over the past 12 months, ManpowerGroup is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because finding new avenues for growth becomes difficult when you already have a substantial market presence. For ManpowerGroup to boost its sales, it likely needs to adjust its prices, launch new offerings, or lean into foreign markets.

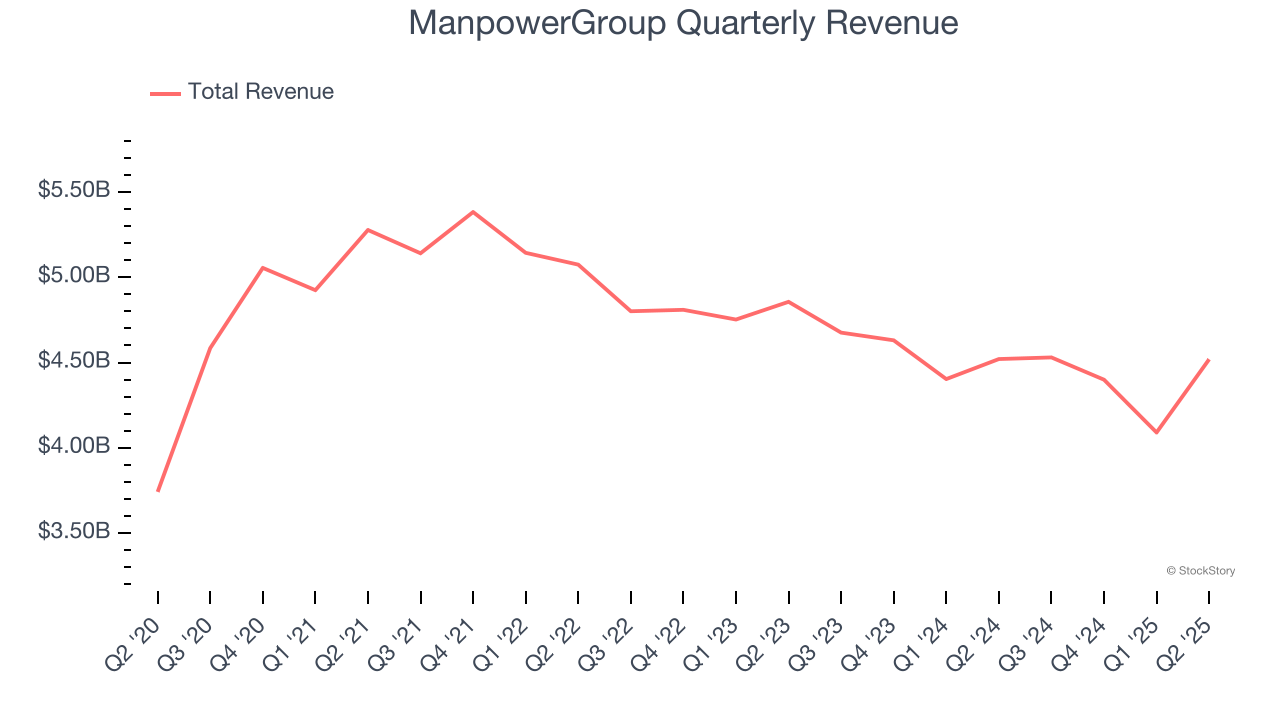

As you can see below, ManpowerGroup struggled to generate demand over the last five years. Its sales dropped by 1.4% annually, a rough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. ManpowerGroup’s recent performance shows its demand remained suppressed as its revenue has declined by 4.5% annually over the last two years.

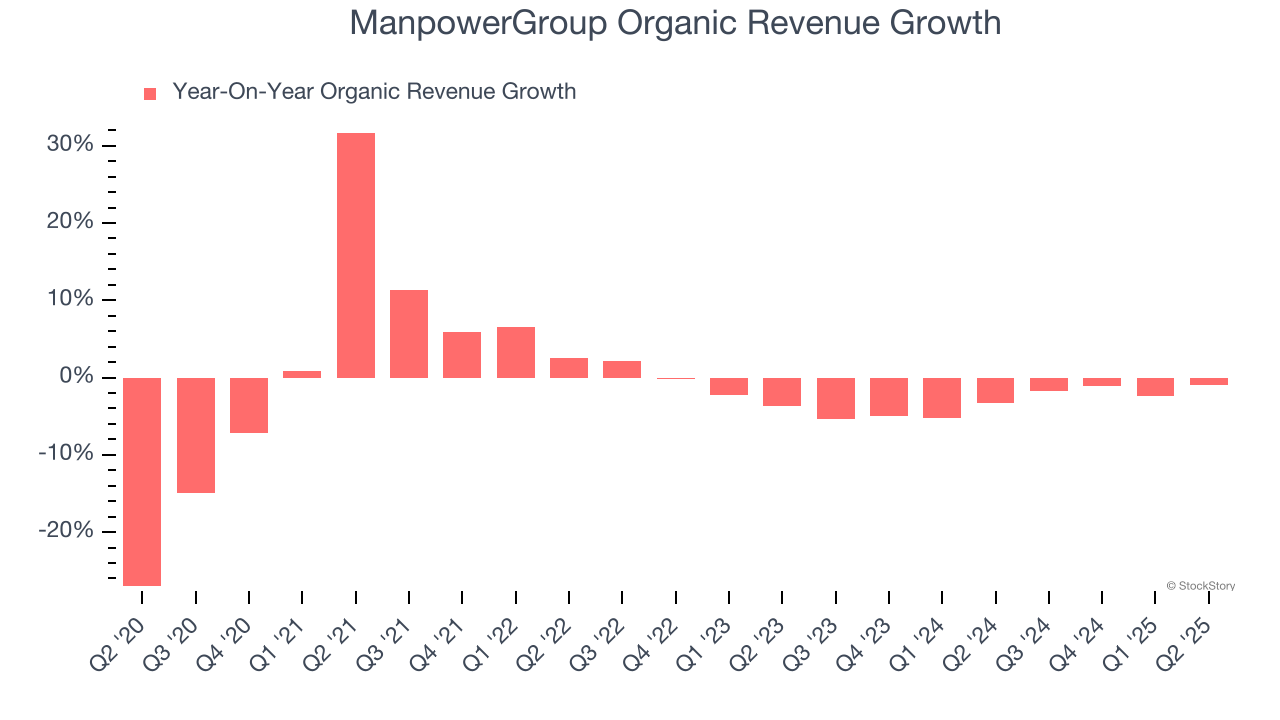

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, ManpowerGroup’s organic revenue averaged 3.1% year-on-year declines. Because this number aligns with its normal revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, ManpowerGroup’s $4.52 billion of revenue was flat year on year but beat Wall Street’s estimates by 3.6%.

Looking ahead, sell-side analysts expect revenue to decline by 1.4% over the next 12 months. While this projection is better than its two-year trend, it’s hard to get excited about a company that is struggling with demand.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

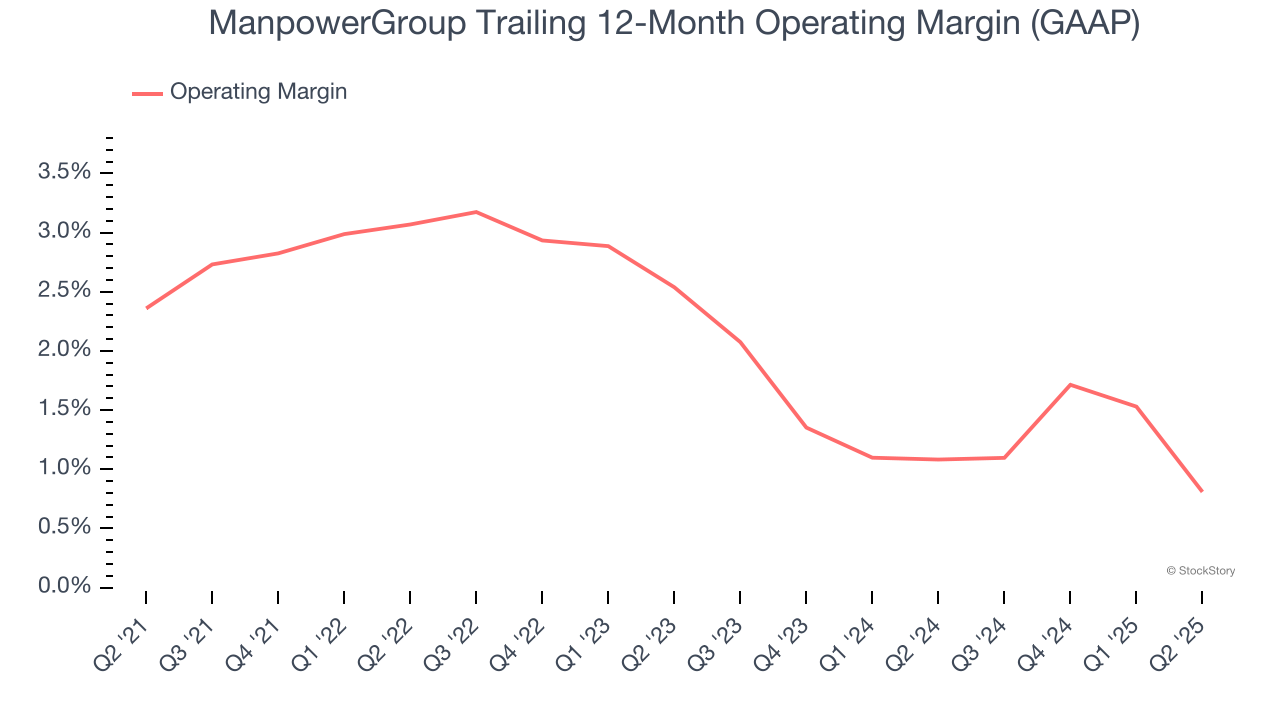

ManpowerGroup was profitable over the last five years but held back by its large cost base. Its average operating margin of 2% was weak for a business services business.

Looking at the trend in its profitability, ManpowerGroup’s operating margin decreased by 1.6 percentage points over the last five years. ManpowerGroup’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, ManpowerGroup’s breakeven margin was down 2.8 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

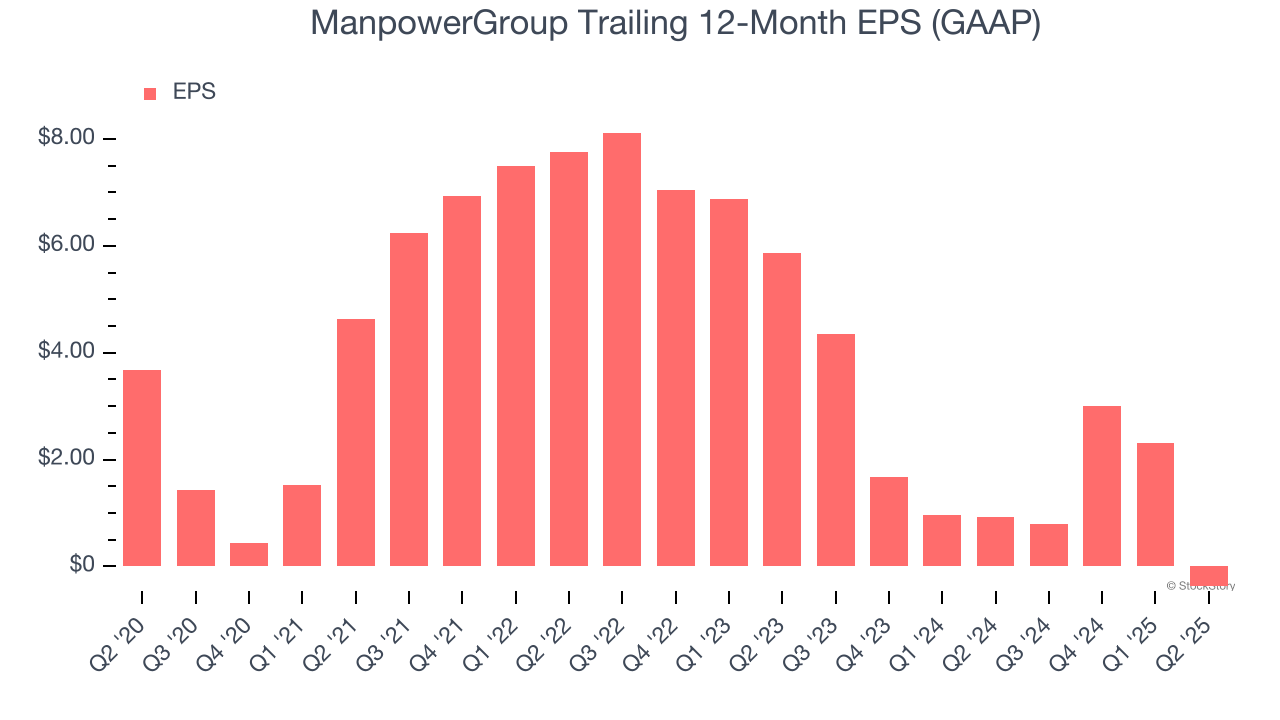

Sadly for ManpowerGroup, its EPS declined by 16% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

We can take a deeper look into ManpowerGroup’s earnings to better understand the drivers of its performance. As we mentioned earlier, ManpowerGroup’s operating margin declined by 1.6 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q2, ManpowerGroup reported EPS at negative $1.44, down from $1.24 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast ManpowerGroup’s full-year EPS of negative $0.38 will flip to positive $3.09.

Key Takeaways from ManpowerGroup’s Q2 Results

We were impressed by how significantly ManpowerGroup blew past analysts’ organic revenue expectations this quarter. We were also excited its EPS guidance for next quarter outperformed Wall Street’s estimates by a wide margin. On the other hand, its EPS missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 4.3% to $45 immediately after reporting.

Indeed, ManpowerGroup had a rock-solid quarterly earnings result, but is this stock a good investment here? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.