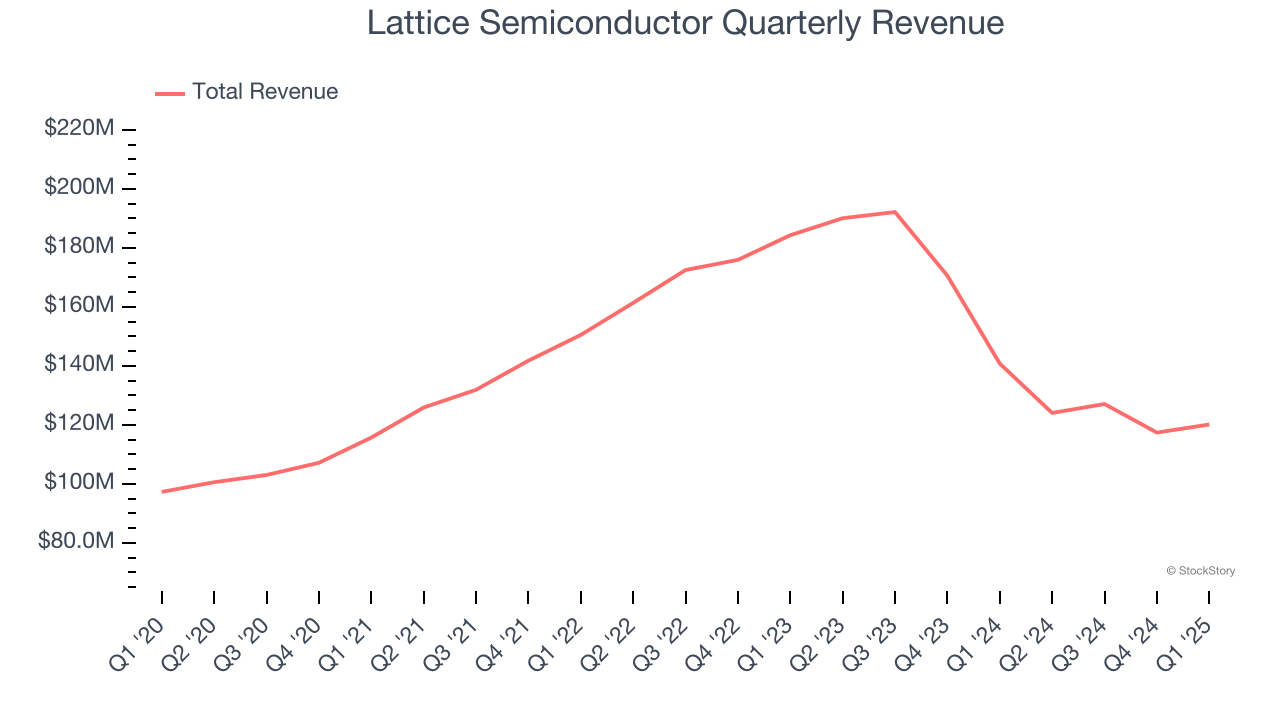

Semiconductor designer Lattice Semiconductor (NASDAQ: LSCC) met Wall Street’s revenue expectations in Q1 CY2025, but sales fell by 14.7% year on year to $120.2 million. The company expects next quarter’s revenue to be around $123.5 million, close to analysts’ estimates. Its non-GAAP profit of $0.22 per share was in line with analysts’ consensus estimates.

Is now the time to buy Lattice Semiconductor? Find out by accessing our full research report, it’s free.

Lattice Semiconductor (LSCC) Q1 CY2025 Highlights:

- Revenue: $120.2 million vs analyst estimates of $120.1 million (14.7% year-on-year decline, in line)

- Adjusted EPS: $0.22 vs analyst estimates of $0.22 (in line)

- Adjusted EBITDA: $40.08 million vs analyst estimates of $37.25 million (33.4% margin, 7.6% beat)

- Revenue Guidance for Q2 CY2025 is $123.5 million at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for Q2 CY2025 is $0.24 at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: 5.8%, down from 11.8% in the same quarter last year

- Free Cash Flow Margin: 19.4%, similar to the same quarter last year

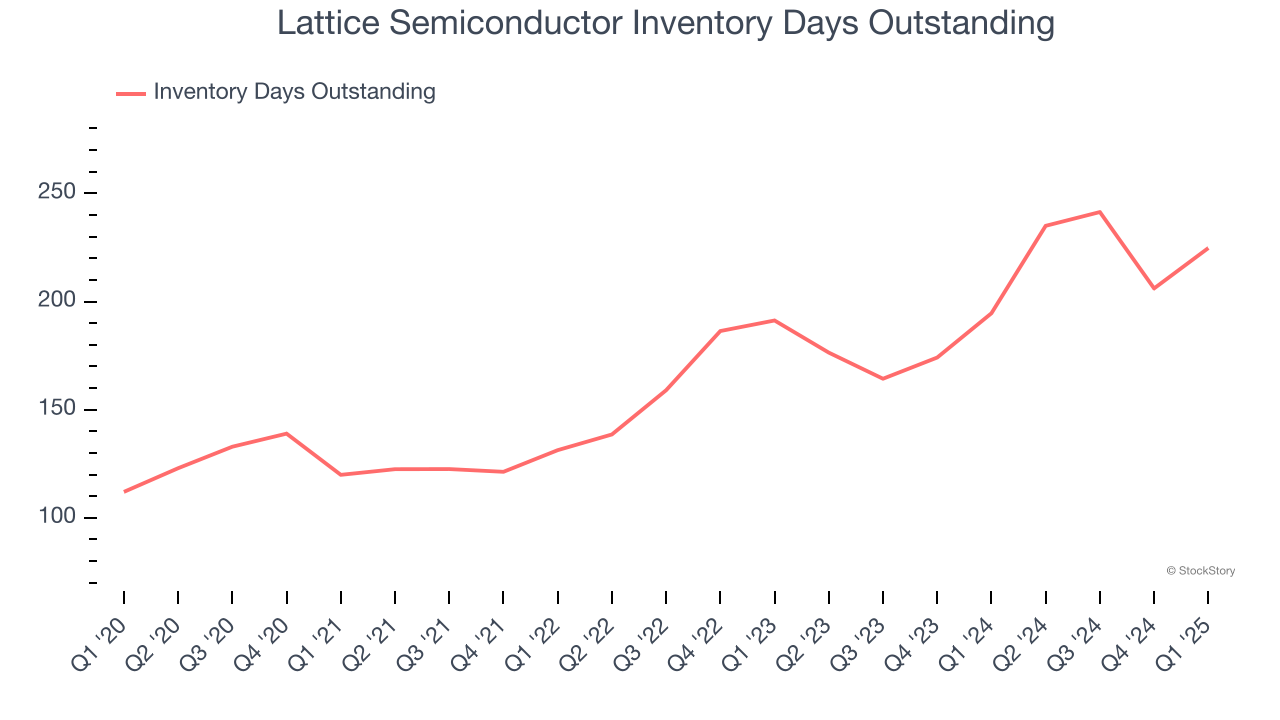

- Inventory Days Outstanding: 225, up from 206 in the previous quarter

- Market Capitalization: $7.14 billion

Ford Tamer, Chief Executive Officer, said, "The first quarter of 2025 developed as expected, with sequential revenue growth, a record level of design wins, and a further expansion of our operating margins. Revenue and design win growth are being led by new applications, notably in generative AI in the datacenter, robotics in industrial, in-cabin and ADAS in automotive, AR/VR in consumer, security, including post-quantum cryptography, and far edge AI for lower power applications. While we are encouraged by our progress, we are monitoring the market environment, along with the broader industry, as it could have an impact on our outlook. "

Company Overview

A global leader in its category, Lattice Semiconductor (NASDAQ: LSCC) is a semiconductor designer specializing in customer-programmable chips that enhance CPU performance for intensive tasks such as machine learning.

Sales Growth

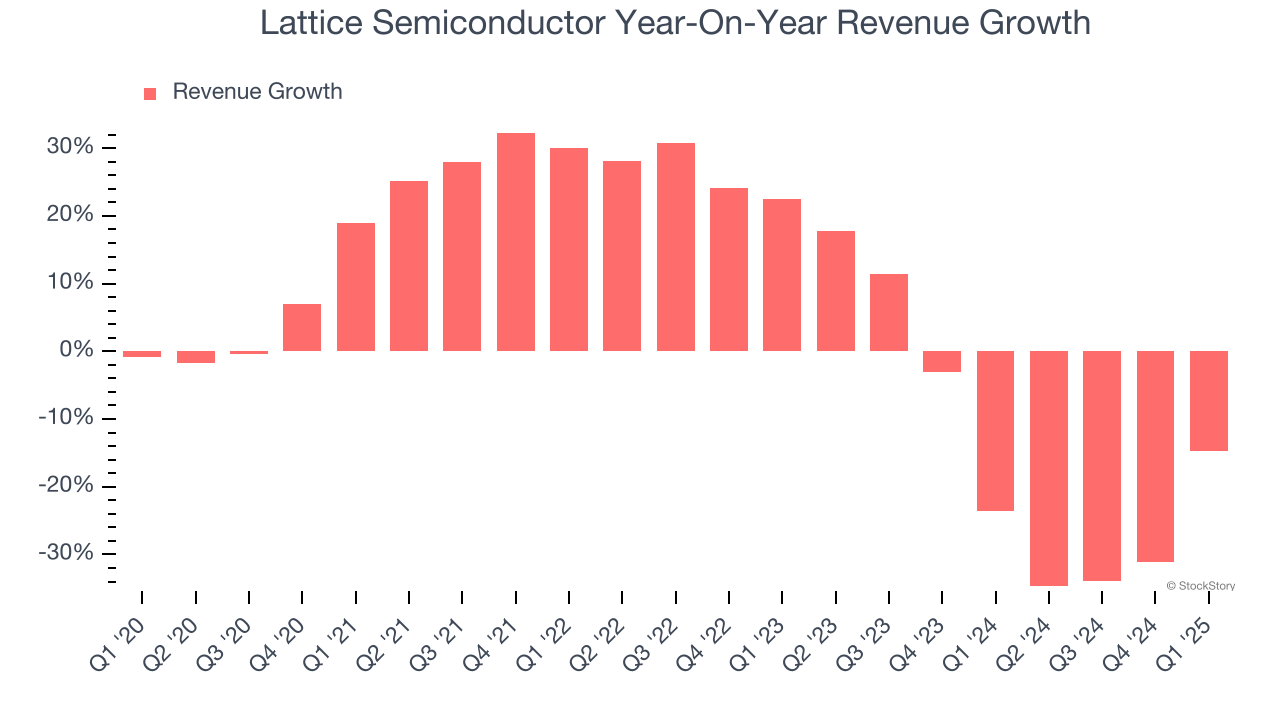

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Lattice Semiconductor grew its sales at a sluggish 3.9% compounded annual growth rate. This was below our standard for the semiconductor sector and is a tough starting point for our analysis. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

We at StockStory place the most emphasis on long-term growth, but within semiconductors, a half-decade historical view may miss new demand cycles or industry trends like AI. Lattice Semiconductor’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 16.1% annually.

This quarter, Lattice Semiconductor reported a rather uninspiring 14.7% year-on-year revenue decline to $120.2 million of revenue, in line with Wall Street’s estimates. Despite meeting estimates, the drop in sales could mean that the current downcycle is deepening. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 12.6% over the next 12 months, an improvement versus the last two years. This projection is healthy and suggests its newer products and services will fuel better top-line performance.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Lattice Semiconductor’s DIO came in at 225, which is 60 days above its five-year average, suggesting that the company’s inventory has grown to higher levels than we’ve seen in the past.

Key Takeaways from Lattice Semiconductor’s Q1 Results

This was a quarter without many surprises. Revenue and adjusted EPS in the quarter roughly met Wall Street's expectations, as did Q2 guidance for those same two metrics. One negative was that Lattice's inventory levels increased. Management stated that the company is "monitoring the market environment, along with the broader industry, as it could have an impact on our outlook", likely referring to tariffs and overall global GDP and industrial production. Overall, this was an unexciting quarter. The stock traded down 3.3% to $51.30 immediately after reporting.

Lattice Semiconductor may have had a tough quarter, but does that actually create an opportunity to invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.