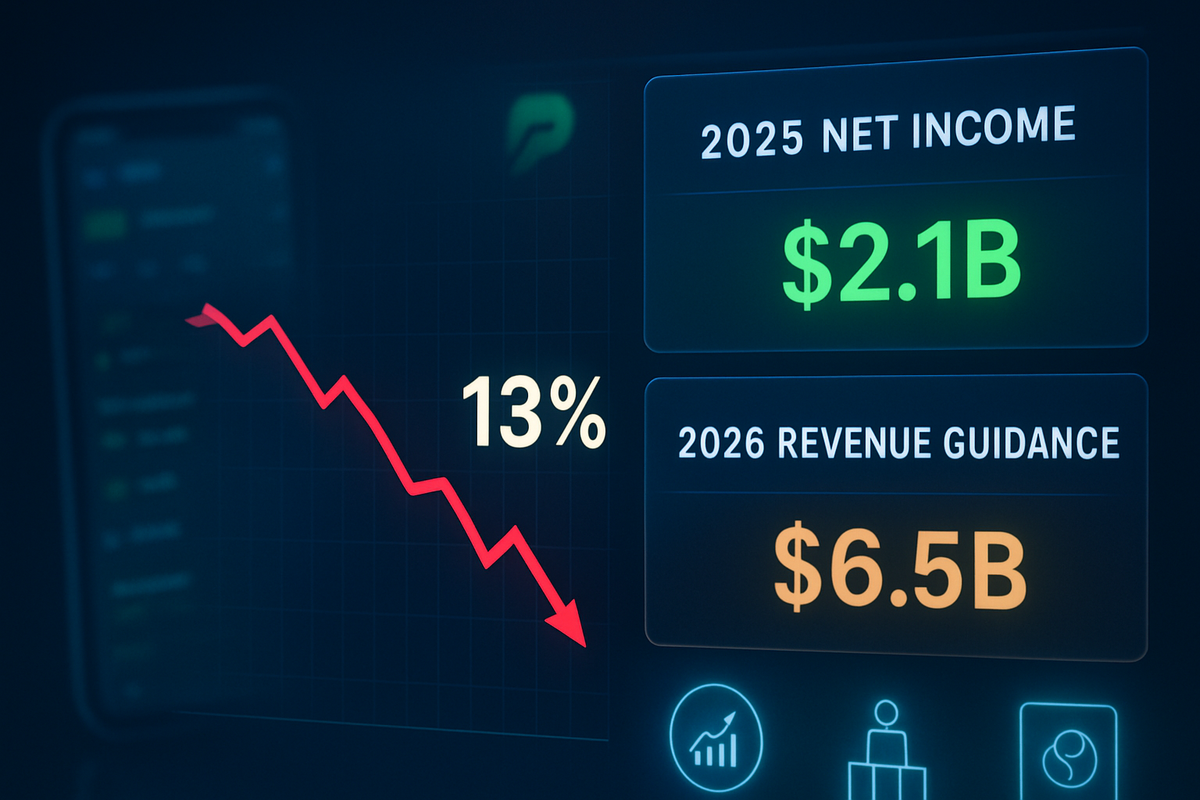

The high-stakes world of online gaming met a harsh reality check on Friday as shares of DraftKings Inc. (Nasdaq: DKNG) plummeted 13.4%, wiping out billions in market capitalization in a single trading session. The sell-off came despite the Boston-based operator reporting its first-ever year of positive net income in 2025 and beating fourth-quarter analyst expectations. The culprit was not the company's past performance, but its future: a 2026 revenue guidance range that fell significantly short of Wall Street’s lofty expectations, signaling a strategic "spending year" ahead.

Investors, who had driven the stock to multi-year highs in anticipation of a massive 2026 breakout, were caught off guard by management’s conservative forecast. While the company achieved the long-awaited milestone of GAAP profitability in 2025, the market’s reaction highlights a shifting sentiment where short-term fiscal discipline is being weighed heavily against the costs of entering new verticals—specifically the burgeoning, federally regulated prediction markets.

A Milestone Overshadowed by a 'Spending Year'

The earnings call on the evening of February 12, 2026, began with a celebratory tone. DraftKings reported Q4 2025 revenue of $1.99 billion, a 43% increase year-over-year, and a quarterly net income of $136.4 million. For the full year of 2025, the company officially moved into the black, marking a historic turning point for a firm that was once the poster child for "growth at any cost" losses. Key metrics showed a maturing business model, with Average Revenue per Monthly Unique Payer (ARPMUP) surging to $139, suggesting that DraftKings is successfully extracting more value from its existing user base.

However, the mood soured when Chief Financial Officer Alan Kelly issued the 2026 revenue guidance. DraftKings projected 2026 revenue between $6.5 billion and $6.9 billion, a figure that sits well below the $7.3 billion consensus among analysts. Furthermore, the company’s EBITDA guidance of $700 million to $900 million trailed the expected $998 million. Management clarified that these figures deliberately exclude potential revenue from the newly launched "DraftKings Predictions" platform while fully accounting for the massive customer acquisition costs and infrastructure investments required to scale the new vertical. This disconnect—the presence of costs without the immediate promise of offsetting revenue—triggered the sharp 13% decline as the market repriced the company’s near-term growth trajectory.

Winners and Losers in the Gaming Sector

The DraftKings slump sent ripples through the gaming and leisure sector, creating a stark contrast between operators. While DraftKings struggled, MGM Resorts International (NYSE: MGM) and its partner Entain saw their joint venture, BetMGM, report a record-breaking 2025 with $2.8 billion in revenue. Following their own report on February 5, MGM shares rose 12%, bolstered by the news that BetMGM had begun returning cash to its parent companies for the first time. The divergence suggests that investors are currently rewarding realized cash flow and dividends over the "investment-heavy" strategy currently favored by DraftKings.

Meanwhile, Flutter Entertainment plc (NYSE: FLUT), the parent company of FanDuel, saw its stock experience a more moderate 4% decline. While FanDuel is also investing heavily in the "FanDuel Predict" vertical to compete in the prediction market space, its dominant 43% share of the U.S. Gross Gaming Revenue (GGR) and more diversified international holdings provided a buffer that DraftKings lacked. Conversely, Penn Entertainment (Nasdaq: PENN) remains in a state of flux; after terminating its high-profile ESPN BET partnership in late 2025, the company is currently rebranding its U.S. operations to "theScore Bet" in an attempt to leverage its media ecosystem in new markets like Missouri.

The Shift to Prediction Markets and Regulatory Headwinds

The market’s reaction to DraftKings’ guidance is deeply tied to the broader evolution of the industry in 2026. The online sports betting (OSB) market has entered a "maturity phase," where traditional user growth is slowing, and the frontier has shifted toward CFTC-regulated event-contract markets—often called prediction markets. DraftKings’ aggressive pivot into this space is an attempt to stay ahead of the curve, but it comes at a time when the regulatory and tax environment is becoming increasingly hostile for operators.

In early 2026, several key states, including Illinois, New Jersey, and Maryland, implemented higher, tiered tax rates on sports betting revenue, with Illinois’ top bracket reaching 40%. Additionally, a 2025 federal tax overhaul capped gambling loss deductions at 90%, a move that has effectively increased the "cost" of betting for high-volume users. These headwinds, combined with the expensive race to dominate the prediction market space, have forced companies to choose between short-term margin protection and long-term market share. DraftKings has clearly chosen the latter, even at the expense of its share price in the immediate term.

The Road Ahead: 2026 and Beyond

Looking forward, the remainder of 2026 will be a critical testing ground for DraftKings' strategic pivot. The company is banking on the launch of "DraftKings Predictions" to create a new, high-margin revenue stream that appeals to a different demographic than traditional sports bettors. If the platform gains traction in the first half of the year, the "conservative" guidance provided this week may prove to have been a "beat-and-raise" setup, potentially allowing the stock to recover its losses as the revenue from prediction markets begins to materialize on the balance sheet.

Furthermore, expansion into new territories like Alberta, Canada, which opened its regulated market in January 2026, provides a fresh runway for growth. The key for DraftKings will be demonstrating that it can manage the dual burden of high tax rates in established states and high investment costs in new verticals without eroding the profitability it worked so hard to achieve in 2025. Market observers will be watching the Monthly Unique Payer (MUP) count closely in the coming quarters; if user growth remains stagnant despite heavy spending, the pressure on management to pivot toward a more conservative, profit-first model will intensify.

Investor Outlook and Final Thoughts

The 13% drop in DraftKings stock is a classic example of a "good news, bad outlook" scenario. While the company has proven it can be profitable, the market is currently unwilling to grant a premium valuation to a business that is entering another heavy investment cycle. The 2026 guidance miss highlights the friction between a company’s long-term strategic goals and the stock market’s quarterly demands for perfection.

For investors, the coming months will be defined by execution. The primary metrics to watch will be the adoption rates of prediction markets and the company's ability to maintain its ARPMUP levels in the face of federal tax changes. While the immediate hit to the stock is painful, the fundamental story of DraftKings has shifted from a question of "if" it can be profitable to "how much" it is willing to spend to remain the market leader. In the volatile world of 2026 gaming, the house may always win, but for DraftKings shareholders, the payout remains deferred.

This content is intended for informational purposes only and is not financial advice.