The global commodities market has reached a historic inflection point as of January 2026, with industrial manufacturers aggressively pivoting from copper to aluminum. This shift is no longer a matter of marginal cost-saving; it has become a structural necessity as the copper-to-aluminum price ratio has surged past 4.2, a level once considered an extreme outlier. Driven by a combination of copper supply deficits and breakthroughs in aluminum heat-exchange technology, the substitution trend is reshaping the balance sheets of major manufacturers and the valuations of the world’s largest mining firms.

The immediate implications are most visible in the cooling and electrical sectors, where the cost differential has become impossible to ignore. While copper prices have touched unprecedented highs of $13,000 per metric ton this month, aluminum—despite its own recent rallies—remains significantly more affordable on a per-volume basis. This divergence is forcing a re-evaluation of long-term material strategies, as the industrial world learns to trade the superior conductivity of copper for the economic resilience of aluminum.

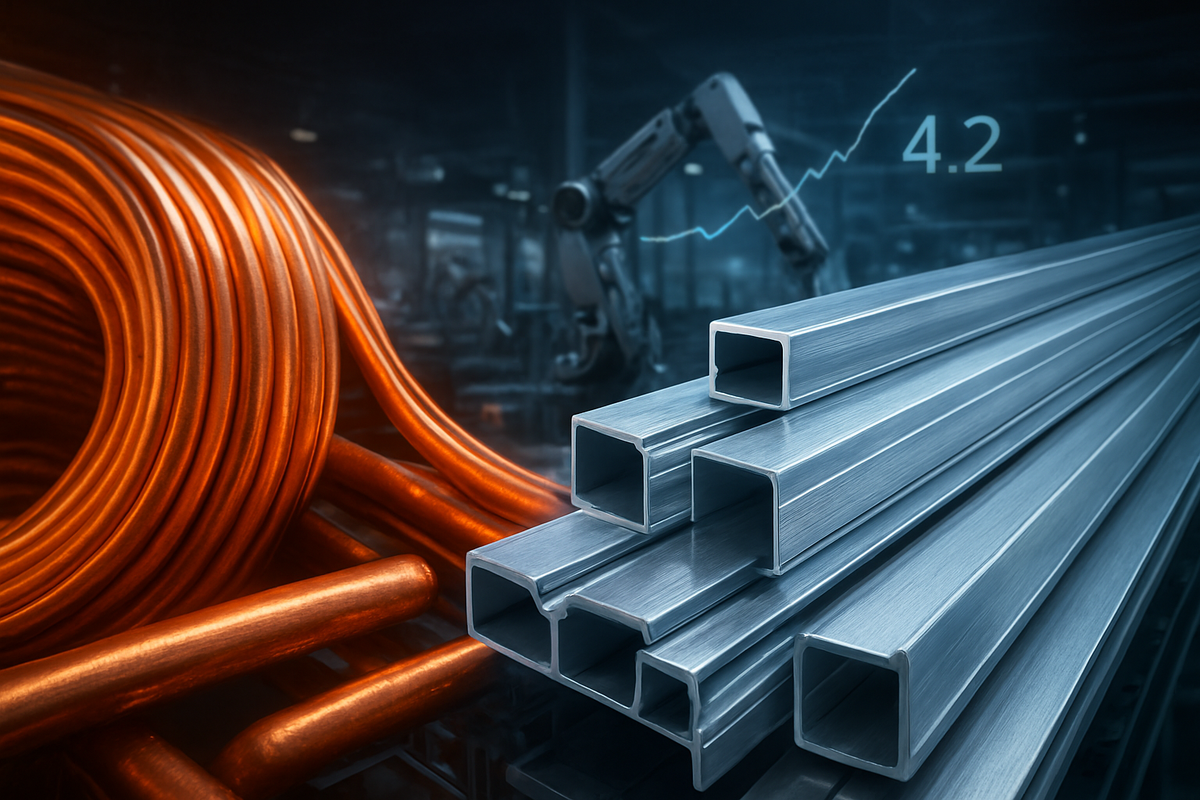

The Economic Tipping Point: A Ratio in Uncharted Territory

The current transition was catalyzed by a dramatic run-up in copper prices throughout late 2025, which culminated in the London Metal Exchange (LME) three-month futures breaching $13,000 per ton in early January 2026. This surge was primarily fueled by acute supply disruptions at major sites like the Grasberg mine in Indonesia and ongoing geopolitical instability in South America. Simultaneously, the copper-to-aluminum price ratio—a key metric for industrial procurement—climbed to a range of 4.2 to 4.4. Historically, analysts have viewed a ratio of 3.5 as the "tipping point" for mass substitution; at 4.2, the economic incentive to switch has moved from advantageous to overwhelming.

While copper faced supply-side shocks, aluminum prices in China reached record highs on the Shanghai Futures Exchange (SHFE), hitting 25,075 yuan per ton (approximately $3,592) this month. These Chinese price peaks have been driven by a "perfect storm" of domestic capacity caps and geopolitical sentiment. China is now effectively at its government-mandated 45 million metric ton annual capacity ceiling, leaving virtually no room for supply expansion within the world’s largest producer. Furthermore, a "flight to hard assets" was triggered earlier this month by geopolitical tensions in Venezuela, which spooked base metal markets and drove speculative capital into aluminum as a proxy for the broader copper rally.

The timeline of this transition accelerated in the final quarter of 2025. As the Global X Copper Miners ETF (NYSE: COPX) and the United States Copper Index Fund (NYSE: CPER) saw increased volatility due to tightening mine supply, manufacturers began finalizing multi-year retooling projects. By the time 2026 opened, the "Great Metal Migration" was well underway, with procurement officers at major conglomerates shifting billions in orders from copper cathode to aluminum ingot.

Winners and Losers: From Miners to AC Manufacturers

The impact of this shift is creating a clear divide between winners and losers in the equity markets. Alcoa Corp (NYSE: AA) has emerged as a primary beneficiary, with its stock price surging over 40% in the first weeks of 2026. As a vertically integrated producer with its own bauxite and alumina supply, Alcoa is uniquely shielded from rising raw material costs while benefiting from the surge in demand for aluminum as a copper substitute. Other diversified giants like Rio Tinto (NYSE: RIO) and the iShares MSCI Global Metals & Mining Producers ETF (BATS: PICK) are also seeing heightened interest as they balance portfolios between the two metals.

Conversely, copper-heavy producers like Freeport-McMoRan (NYSE: FCX) and Southern Copper (NYSE: SCCO) are facing a complex landscape. While high copper prices initially boosted their margins, the persistent high price ratio is now eroding their long-term demand base. Analysts warn that if the substitution trend becomes permanent in high-volume sectors, copper miners may find themselves with a "demand hole" once current supply disruptions are resolved.

The air-conditioning manufacturing sector provides the most vivid example of this corporate divide. Daikin Industries (OTC: DKILY) has successfully executed a strategy to halve its copper usage, leaning heavily on aluminum heat exchangers to maintain price competitiveness. In late 2025, a partnership between Chinese manufacturers and JD.com led to the launch of the first "all-aluminum" air conditioning units, which are priced nearly 20% lower than traditional copper-based models. However, some players remain resistant; Gree Electric Appliances Inc. of Zhuhai (SZSE: 000651) continues to prioritize copper in its high-end units, betting that consumer perception of copper's durability will outweigh the current 40% material cost disadvantage.

Industry Significance and Historical Precedents

This event fits into a broader industry trend toward "thrifting" and material efficiency that has been building for a decade. Historically, the last major wave of copper-to-aluminum substitution occurred during the commodity super-cycle of the mid-2000s, but it was often hampered by technical limitations, such as aluminum's susceptibility to corrosion and more difficult welding requirements. The 2026 pivot is different because of technological advancements like microchannel extrusion, which allows aluminum to match copper's thermal performance in a smaller, lighter footprint.

The geopolitical dimension cannot be understated. China’s 45-million-ton "hard ceiling" on aluminum production is a climate-driven policy designed to limit the energy-intensive smelting process. This regulatory cap, combined with the "Venezuela Factor" and US-China trade tensions, has turned aluminum into a strategic asset. The ripple effects are extending into the electric vehicle (EV) sector, where manufacturers are increasingly using aluminum wiring harnesses to reduce both cost and vehicle weight, further accelerating the move away from copper.

Comparisons are being drawn to the permanent shift seen in the high-voltage power transmission industry decades ago, where aluminum completely replaced copper. Market observers suggest that the HVAC and automotive sectors may be undergoing a similar permanent structural change, meaning that even if copper prices eventually soften, many manufacturers will not go through the expensive process of switching back.

The 2026 Outlook: Supply Surpluses and Strategic Pivots

Looking ahead, the market is bracing for a potential "decoupling" of aluminum and copper prices. While the current price ratio of 4.2 is driving substitution, global aluminum stocks are expected to improve significantly by the second half of 2026. A massive wave of new smelting capacity in Indonesia, largely backed by Chinese investment, is slated to bring nearly 2 million tons of new supply online. Goldman Sachs analysts project that this will push the global aluminum market into a surplus of 1.5 million tons by year-end, potentially dragging aluminum prices back down toward $2,350 per ton.

For manufacturers, the short-term challenge will be managing the volatility of the transition. Strategic pivots are required not just in procurement, but in engineering and supply chain logistics. Companies that have not yet invested in aluminum-compatible welding and assembly lines may find themselves at a severe price disadvantage against competitors who moved earlier. In the long term, this may lead to a more bifurcated market where copper is reserved for "mission-critical" high-conductivity applications, while aluminum becomes the standard for general heat exchange and mid-range electrical components.

Market Wrap-Up and Investor Considerations

The shift from copper to aluminum represents one of the most significant material transitions in modern manufacturing history. The crossing of the 4.2 price ratio threshold has acted as a catalyst, turning a gradual trend into a rapid migration. While record-high Chinese prices and geopolitical tensions have dominated the headlines in early 2026, the underlying story is one of industrial adaptation and the relentless search for cost efficiency in an era of high commodity prices.

Moving forward, the market will be characterized by a tug-of-war between high current demand and the looming supply glut from Southeast Asia. For investors, the focus should remain on the "substitution tailwind" benefiting companies like Alcoa Corp (NYSE: AA), while monitoring the potential for a price correction as Indonesian supply hits the market later this year.

Key indicators to watch in the coming months include the monthly inventory data from the Shanghai Futures Exchange and any shifts in the stance of "copper holdouts" like Gree Electric. If the ratio remains above 4.0 for the duration of Q1 2026, the structural shift to aluminum may become an irreversible feature of the global industrial landscape.

This content is intended for informational purposes only and is not financial advice.