As the curtain closes on 2025, the exuberant "risk-on" sentiment that defined the early years of the artificial intelligence boom has been replaced by a somber, calculated retreat. On this final day of the year, December 31, 2025, financial markets are grappling with a stark reality: the American consumer is pulling back. A multi-month slide in confidence has triggered a massive sector rotation, stripping capital from high-flying technology giants and funneling it into the sturdy, if unglamorous, coffers of defensive large-cap value funds.

The implications are immediate and visible across trading desks. The "Santa Claus Rally" many expected to cap off a volatile year failed to materialize, replaced instead by a "Great Rebalancing." Investors are no longer chasing 30% year-over-year growth in software-as-a-service; they are seeking the 3.5% dividend yields and recession-resistant earnings of consumer staples, healthcare, and utilities. This shift marks a fundamental change in market leadership, signaling that the "higher for longer" interest rate environment and geopolitical trade tensions have finally begun to weigh on the domestic economy’s primary engine: consumer spending.

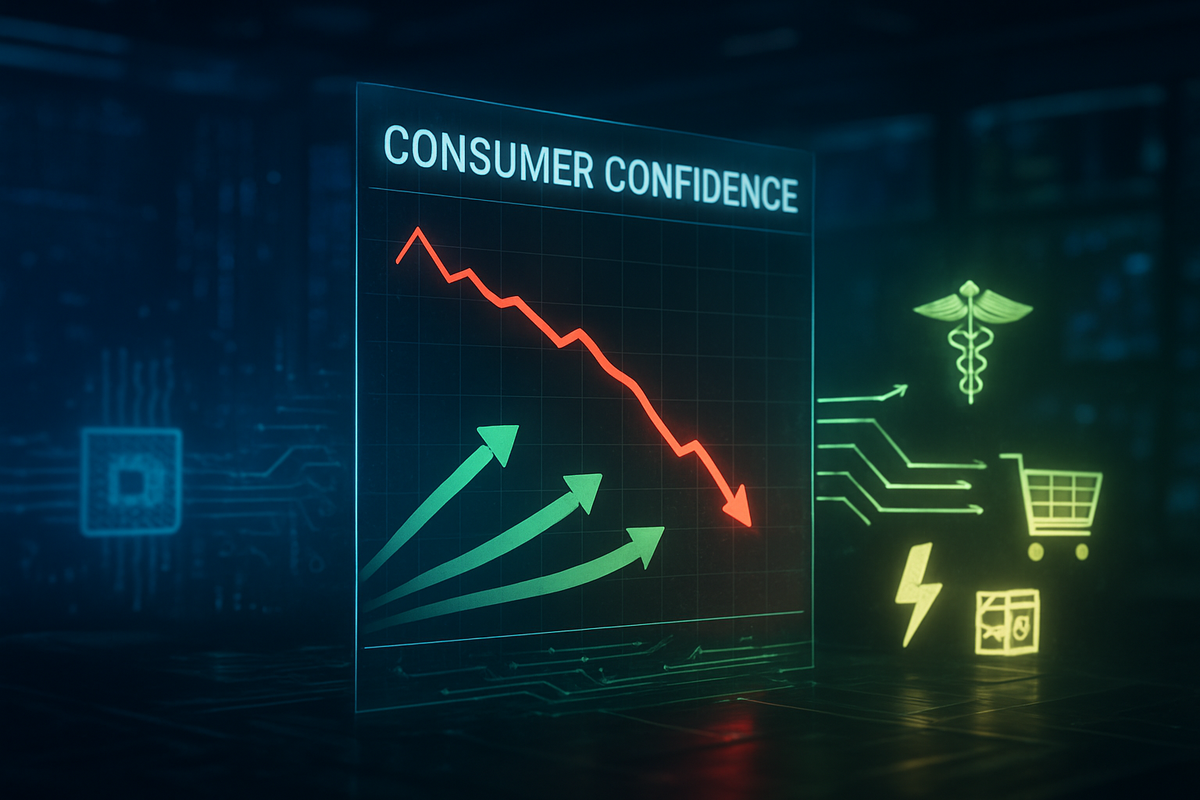

The Cracks in the Consumer Foundation

The current malaise did not emerge overnight but is the culmination of a bruising 2025. The Conference Board’s Consumer Confidence Index fell for its fifth consecutive month in December, settling at a dismal 89.1. More alarming to economists is the Expectations Index, which has remained below the critical 80-point threshold for nearly a year. Historically, a sustained dip below this level has been a reliable harbinger of a recession within the following six to twelve months. The decline can be traced back to the "tariff shock" of April 2025, which reignited inflationary pressures on imported goods, and a disruptive federal government shutdown in the autumn that shook public trust in fiscal stability.

Throughout the fourth quarter, the labor market—long the bedrock of the post-pandemic recovery—began to show visible signs of cooling. The "jobs plentiful" differential, a key metric measuring how easy consumers find it to secure employment, has narrowed significantly. As a result, households have pivoted from discretionary "big-ticket" purchases to a "survivalist" spending mode. This shift was underscored by a lackluster holiday shopping season where consumers prioritized essentials over electronics and luxury goods, forcing retailers to lean heavily on deep discounting to clear inventories.

The market’s reaction has been swift and decisive. Institutional investors, sensing the end of the growth cycle, have aggressively liquidated positions in overextended tech names. The capital has not left the market entirely but has moved into "quality" and "value" factors. Funds like the Vanguard Value ETF (NYSE: VTV) and the Schwab U.S. Dividend Equity ETF (NYSE: SCHD) have seen record inflows in December, as they offer exposure to companies with strong balance sheets and consistent cash flows that can withstand a potential 2026 downturn.

Winners and Losers in the Defensive Pivot

In this new landscape, the hierarchy of corporate America is being reshuffled. The clear winners are the "Value Titans"—companies that provide the goods and services consumers cannot live without, regardless of the economic climate. Walmart Inc. (NYSE: WMT) has emerged as a primary beneficiary, with its stock up over 23% this year as it successfully captured "trade-down" traffic from middle- and upper-income households. Similarly, Procter & Gamble Co. (NYSE: PG) has seen a resurgence in its stock price, as its portfolio of household essentials is viewed as a safe harbor against market volatility.

The healthcare sector has also reclaimed its status as a market leader. Eli Lilly and Company (NYSE: LLY) has maintained its momentum, not through speculative growth, but through the essential nature of its GLP-1 medications and new federal contracts for Medicare access. Other defensive stalwarts like Gilead Sciences, Inc. (NASDAQ: GILD) and AbbVie Inc. (NYSE: ABBV) have outperformed the broader S&P 500 significantly in the second half of 2025, as investors prize their high dividend yields and low correlation to the broader economic cycle. Even the utility sector, often ignored during tech bull markets, has seen a revival; NextEra Energy, Inc. (NYSE: NEE) and Constellation Energy Corp. (NASDAQ: CEG) are being bought both for their defensive qualities and their role in powering the energy-hungry AI data centers that remain in operation.

Conversely, the "losers" of this rotation are the high-multiple growth stocks that dominated the 2023-2024 period. Microsoft Corp. (NASDAQ: MSFT) and Broadcom Inc. (NASDAQ: AVGO), while still fundamentally strong, have faced significant selling pressure as their price-to-earnings multiples were deemed unsustainable in a slowing economy. The Technology Select Sector SPDR Fund (NYSEARCA:XLK) has lagged behind the defensive sectors for three consecutive months, marking a stark departure from the AI-driven mania of previous years. Companies reliant on discretionary spending, such as Tesla, Inc. (NASDAQ: TSLA) and Amazon.com, Inc. (NASDAQ: AMZN), have also faced headwinds as consumers defer vehicle purchases and tighten their e-commerce budgets.

The "Great Rotation" in Historical Context

This shift from growth to value fits into a broader historical pattern often seen at the tail end of a prolonged expansion. Much like the "dot-com" bust of 2000 or the pre-recession jitters of 2007, the market is currently undergoing a "flight to quality." However, the 2025 version has a unique modern twist: the transition from AI "picks and shovels" to AI "adopters." Investors are moving away from the companies that build AI hardware and toward those—like healthcare and industrial firms—that use AI to squeeze out higher margins and operational efficiencies.

The wider significance of this event lies in the "S&P 493" finally catching up to the "Magnificent Seven." For years, market breadth was dangerously narrow, with a handful of tech stocks carrying the entire index. The current rotation is, in many ways, a healthy normalization. By diversifying into value and defensive sectors, the market is building a more resilient foundation, even if it means lower headline returns for the major indices in the short term. This rebalancing also reflects a growing consensus that the era of "easy money" and zero-interest rates is firmly in the past, forcing a return to fundamental valuation metrics.

From a policy perspective, the dipping consumer confidence puts the Federal Reserve in a difficult position. While inflation has cooled from its 2022 peaks, it remains "sticky" due to the 2025 tariff environment. The Fed must now decide whether to cut rates to stimulate the flagging consumer or keep them elevated to prevent an inflationary rebound. This "stagflationary" shadow is precisely what is driving investors toward the iShares MSCI USA Quality Factor ETF (NYSEARCA:QUAL) and other funds that prioritize companies with low debt and high profitability.

What Lies Ahead for 2026

Looking into the first half of 2026, the primary question is whether this sector rotation is a temporary defensive crouch or the beginning of a prolonged bear market. Short-term, we expect defensive sectors like healthcare and utilities to continue their outperformance as long as consumer confidence remains below the 90-point mark. Strategic pivots will be required for growth-oriented funds, which may need to increase their weightings in "defensive tech"—companies with massive cash reserves and essential enterprise contracts—to stem outflows.

A potential scenario for 2026 involves a "soft landing" that finally turns "hard" as the cumulative effects of high interest rates and reduced consumer demand take hold. If a recession is officially declared in the coming months, the rotation into large-cap value will likely accelerate, turning funds like the Invesco S&P 500 Low Volatility ETF (NYSEARCA:SPLV) into the most sought-after assets on Wall Street. However, if the Fed manages to navigate a series of precise rate cuts without reigniting inflation, we could see a "relief rally" in growth stocks by mid-year.

The challenge for investors will be timing. The transition from a growth-led market to a value-led one is often volatile and marked by false starts. Market opportunities will emerge in "beaten-down" quality growth stocks that have been unfairly punished in the general exodus from tech, but for now, the momentum remains firmly with the "boring" sectors of the economy.

A Final Assessment of the Market Shift

As we conclude 2025, the key takeaway is that the "AI premium" is no longer enough to insulate the market from macroeconomic gravity. The decline in consumer confidence has served as a wake-up call, reminding participants that the U.S. economy is still 70% driven by household spending. The rotation into defensive large-cap value is not just a trend; it is a rational response to a changing risk profile.

Moving forward, the market is likely to be characterized by lower volatility but also lower overall returns compared to the explosive growth of the mid-2020s. This "new normalcy" prizes dividends, earnings stability, and balance sheet strength over visionary promises. Investors should watch the monthly consumer confidence prints and the unemployment rate with eagle eyes in the coming months; any further deterioration there will likely cement the dominance of the defensive trade for the foreseeable future.

The "Great Rebalancing" of late 2025 may eventually be seen as the moment the market matured, moving past the speculative excesses of the AI boom and returning to the fundamental principles of value investing. For the savvy investor, the message is clear: in a world of uncertainty, there is no substitute for quality.

This content is intended for informational purposes only and is not financial advice.