For most of its history, Advanced Micro Devices (AMD) has lived in the shadow of its rival Intel (INTC). There’s a good reason for this. AMD’s x86 foundation exists because Intel allowed it. Back in the 1970s, customers like IBM (IBM) did not want to rely on a single customer for their chips. So Intel licensed its x86 designs to AMD, making it a second-source manufacturer.

A couple of decades later, Intel stopped sharing its designs with AMD, forcing it to come up with its own designs after obtaining permission to continue using x86 architecture through a complicated legal battle. The forced innovation led to AMD disrupting Intel for the first time in the early 2000s, when it introduced 64-bit computing, seriously threatening Intel’s server market share.

Since then, AMD’s products have performed better than Intel's through various phases of development. Most recently, AMD’s EPYC server CPUs gave it a technological lead over Intel. Up until this point, AMD’s lead had always been short-lived. Wall Street always backed Intel to come back stronger, meaning AMD was hardly ever able to translate its technological lead into market share. This is also what happened when EPYC came out. AMD’s server market share at this point was a disappointing 1%, even though it had the better product!

For two years after a clear lead on various benchmarks, EPYC CPUs were unable to gain traction. Wall Street, enterprises, and OEMs did not want to shift away from Intel, as they’d have to change years of development carried out on Intel’s CPU ecosystem. This switching cost was AMD's biggest barrier until Intel stumbled, unable to move to the 7nm process when AMD successfully executed it. Now, AMD was clearly ahead, and hyperscalers like Oracle (ORCL) and Alphabet (GOOG) (GOOGL) started deploying AMD CPUs at scale.

The common theme through AMD’s history was the lack of respect from Wall Street. However, for shrewd investors, this lack of attention also allowed them to buy the company’s stock at great prices, helping make the stock a multibagger over the last 10 years.

Today, the stock stands at a similar point. The era of increased CPU demand due to AI inference is upon us. AMD has a clear lead over Intel and has been gaining market share steadily. While it still only commands a 30% market share by volume, the percentage is increasing steadily, thanks mainly to modern hyperscalers preferring AMD while traditional enterprises still opt for Intel due to high switching costs. It is staggering to think that Intel still owns 70% of the market despite disappointing its customers for a decade. Looking at this from AMD shareholders’ perspective, there’s still a big piece of the pie to be had, and as long as the market continues to discount AMD’s potential, investors can get in at great prices. At the beginning of another CPU revolution, investors who know this context will have an easier time holding the stock for the massive upside it can still have.

About Advanced Micro Devices Stock

Advanced Micro Devices is a leading semiconductor company specializing in high-performance computing and graphics solutions. The company operates through the Embedded, Data Center, Client & Gaming segments. Its broad product portfolio includes microprocessors, graphics processors, and system-on-chip (SoC) solutions designed for data centers, gaming, and embedded systems.

AMD stock has been on a tear since the beginning of April, up over 70%. The iShares Semiconductor ETF (SOXX) is up 40% during the same period. While the rally has been spread across the whole semiconductor industry, AMD has clearly outperformed the rest.

An 80% gain in less than a month would mess up the valuation of any stock, right? Not AMD! Wall Street continues to ignore the stock, as evidenced by a 77x forward P/E ratio, which is 18% below the firm’s five-year average forward P/E. For a company that is expected to grow its earnings by 60% by December 2026, 64% in 2027, and 35% in 2028, the valuation doesn’t make sense. That’s why investors buying after an 80% rally are still getting the stock at a great price!

AMD Continues to Grow

The company posted its fourth-quarter FY 2025 results on Feb. 3, with revenue reaching a record $10.3 billion. This reflects 34% year-over-year (YoY) growth, which was driven by strong performance in the Data Center and Client and Gaming segments. The figure also included around $390 million in MI308 sales to China, which was not part of the company’s initial guidance. Non-GAAP earnings for the quarter were $1.53 per share, exceeding market expectations by $0.21.

Going forward, the company expects first-quarter fiscal 2026 revenue to be around $9.8 billion, with a range of plus or minus $300 million. This includes approximately $100 million of MI308 sales to China. At the midpoint, this represents 32% YoY growth. However, on a sequential basis, revenue is projected to decline by roughly 5%. This is mainly due to seasonal weakness in Embedded, Client, and Gaming, partly offset by continued strength in Data Center. Chair, President & CEO Lisa Su reaffirmed the long-term outlook, highlighting a path to deliver over 35% revenue CAGR over the next three to five years.

What Are Analysts Saying About AMD Stock?

On April 24, DA Davidson upgraded Advanced Micro Devices from “Neutral” to “Buy.” The firm also raised its price target on the stock from $220 to $375. It pointed to increasing CPU demand and better visibility into the company’s role in data center expansion. DA Davidson expects meaningful upside to estimates ahead of its May 5 earnings.

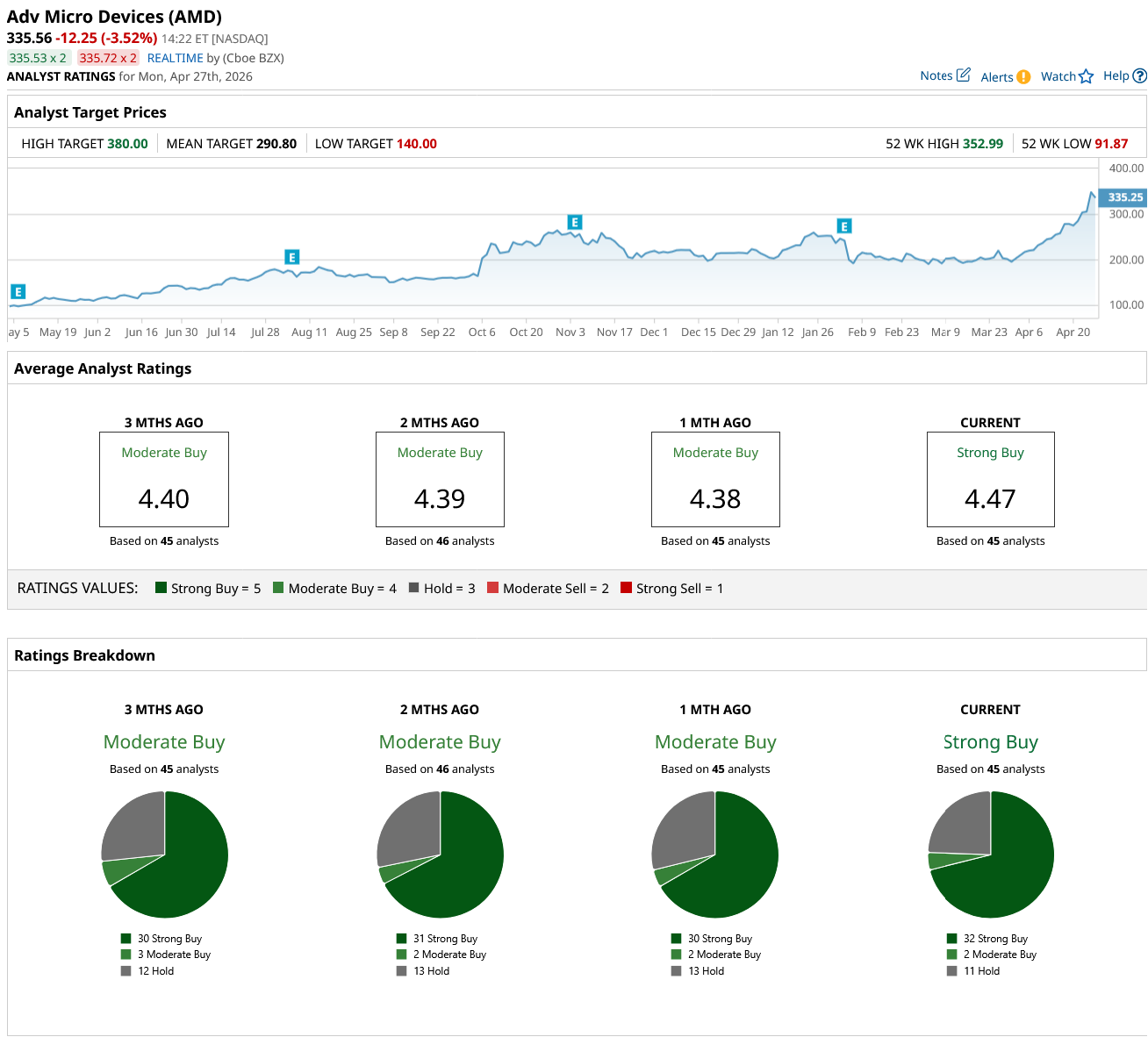

AMD stock carries a consensus “Strong Buy” rating as per 45 Wall Street analysts covering it. This extremely positive rating indicates strong analyst support, which is strengthening investor confidence. The stock has a mean price target of $290.80, which has already been achieved. However, considering the changing AI dynamics, expect multiple analysts to update their financial models very soon.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart