As the semiconductor sector enters a pivotal earnings season, Wall Street sentiment around Advanced Micro Devices (AMD) is turning incrementally more bullish. In a notable move, Stifel raised its price target on AMD by 14.3%, signaling growing confidence in the chipmaker’s positioning at the center of the artificial intelligence (AI) infrastructure buildout.

The upgrade from $280 to $320, while maintaining a “Buy” rating, reflects significant optimism. Stifel’s revised outlook is anchored in a convergence of structural tailwinds accelerating demand for AI compute, deepening relationships with major customers such as Meta Platforms (META) and OpenAI, and a robust product roadmap that includes next-generation data center solutions with the anticipated launch of the MI450/Helios ahead.

Crucially, the timing of the price target hike, just as tech earnings begin to unfold, underscores a broader market narrative as expectations for AI-driven semiconductor demand is potentially accelerating. With compute demand running strong and new product cycles on the horizon, AMD is increasingly viewed as one of the primary beneficiaries of the next leg of the AI investment cycle while reinforcing confidence in AMD’s long-term earnings potential.

About Advanced Micro Devices Stock

Advanced Micro Devices is a Santa Clara, California–based fabless semiconductor firm, known for high-performance computing solutions including its Ryzen, EPYC, Threadripper, Radeon, and Instinct product lines. Since its founding, AMD has evolved into a major player in CPUs, GPUs, adaptive SoCs, FPGAs, and AI accelerators. AMD’s market cap currently stands at $463.8 billion, placing it among the top semiconductor firms globally.

AMD has delivered an exceptionally strong price performance, reinforcing its position as one of the leading beneficiaries of the AI-driven growth.

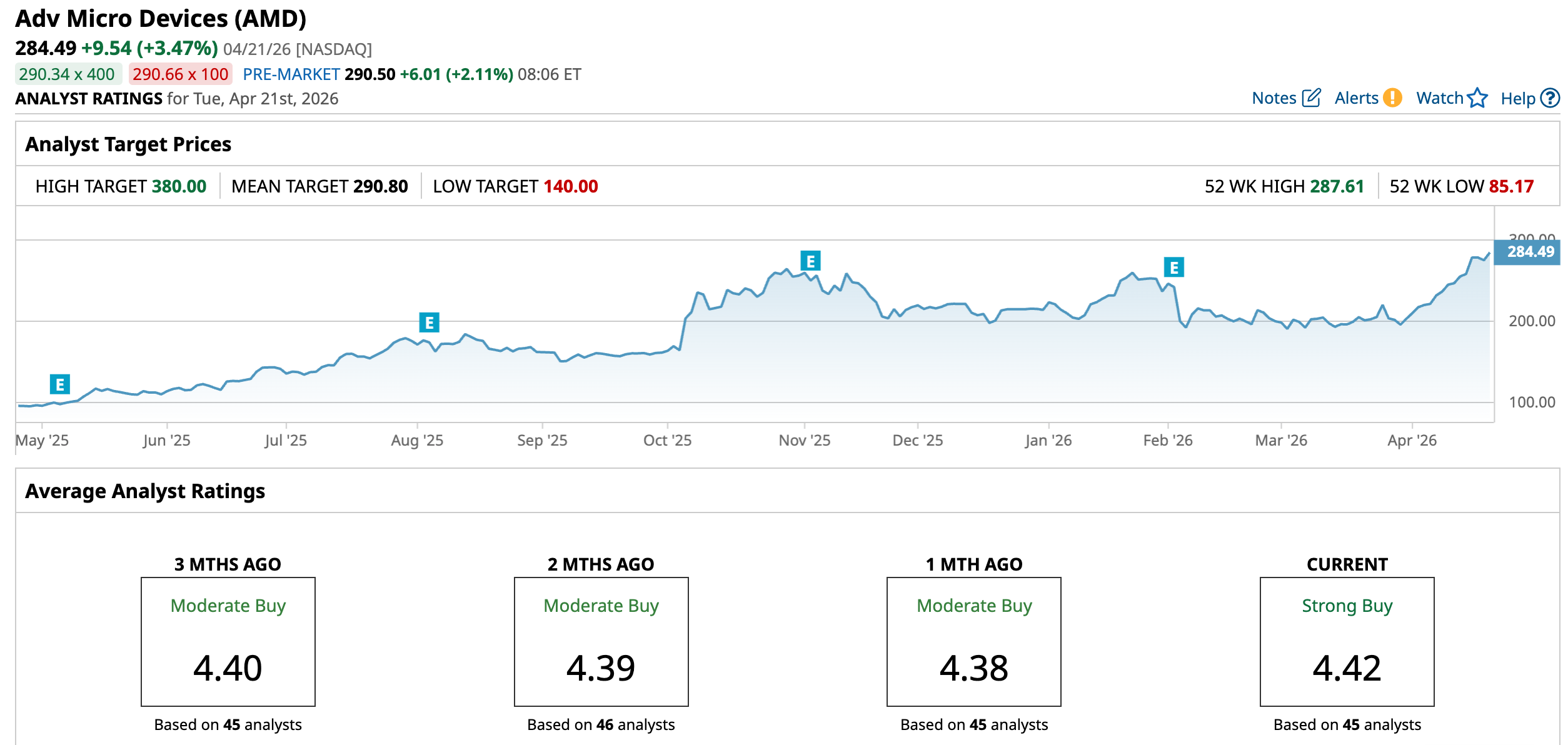

Year-to-date (YTD), AMD stock is up 32.84%, building on an already extraordinary 232.5% return over the past 52 weeks, driven by data center growth and AI demand tailwinds.

Momentum has accelerated meaningfully in recent sessions, with the stock extending a multi-day rally and posting strong gains of 11.53% over the past five trading days, part of a broader winning streak that has driven 41.31% upside over the past month. This near-term surge has been fueled by a combination of earnings optimism, analyst upgrades, and continued AI growth.

This strength culminated in AMD hitting a new 52-week high of $287.61 on April 20. Investors have responded to surging AI and data center demand, especially for EPYC server CPUs and AI accelerators, alongside optimism around upcoming product cycles such as next-generation GPUs.

AMD stock is currently priced at 48.42 times forward earnings, trading at a lofty valuation compared to the sector median and its historical average.

Better-Than-Expected Financial Performance

Advanced Micro Devices reported its fourth quarter and full-year 2025 financial results on Feb. 3, 2026. For the fourth quarter of 2025, AMD posted record revenue of $10.3 billion, representing a 34% year-over-year (YOY) increase, driven primarily by strong demand in its data center segment, including EPYC CPUs and Instinct AI accelerators.

Non-GAAP net income reached to $2.5 billion, marking a 42% YOY increase, while non-GAAP EPS came in at $1.53, up 40% YOY and exceeded expectations. Profitability also improved meaningfully, with operating margin expanding to 17% from 11% a year earlier. Also, non-GAAP gross margin stood at 57%, compared to the prior-year quarter’s 54%.

Segmentally, the data center business emerged as the primary growth engine, with Q4 revenue of $5.4 billion, up 39% YOY, supported by accelerating adoption of AI GPUs and server CPUs. This structural shift toward AI and high-performance computing has been central to AMD’s financial outperformance throughout 2025.

For the full year 2025, AMD delivered record revenue of $34.6 billion, representing 34% YOY growth, highlighting broad-based strength across its portfolio. Non-GAAP EPS rose 26% to $4.17, underscoring strong earnings expansion. Margins remained resilient, with non-GAAP gross margin at 52%.

Furthermore, AMD provided Q1 2026 revenue guidance of around $9.8 billion (plus or minus $300 million), implying continued strong growth of 32% YOY at the midpoint, along with non-GAAP gross margin guidance of 55%, indicating sustained margin expansion.

Analysts covering AMD predict its EPS to rise by 33.3% YOY to $1.04 in the first quarter (about to be reported on May 5). Its EPS is expected to rise by 76.76% YOY to $5.78 in fiscal 2026, before improving by around 59% annually to reach $9.20 in fiscal 2027.

Analysts Are Optimistic About AMD Stock

In addition to Stifel’s price target upgrade, some other analysts have shown confidence about AMD’s prospects. Earlier this month, Erste Group upgraded AMD to “Buy” from “Hold,” citing strong data center demand, improving profitability, and a compelling product roadmap.

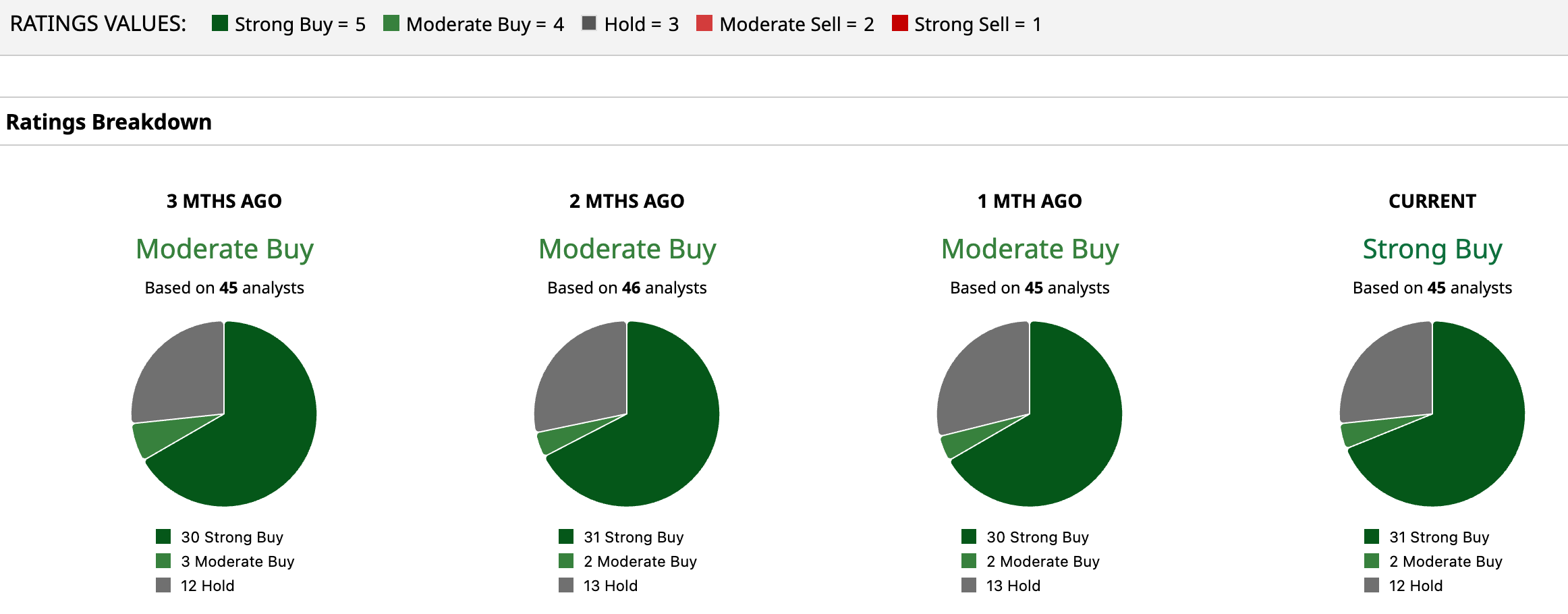

AMD stock has a consensus “Strong Buy” rating overall. Out of 45 analysts covering the semiconductor stock, 31 recommend a “Strong Buy,” two give a “Moderate Buy,” and 12 analysts stay cautious with a “Hold” rating.

Its average analyst price target of $290.80 suggests an upside of 2.2%. The Street-high target price of $380 indicates as much as 33.6% upside ahead.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart