As the Q4 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the data infrastructure industry, including Elastic (NYSE: ESTC) and its peers.

Generating insights from system level data is an increasing priority for most businesses, but to do so requires connecting and analyzing piles of data stored and siloed in separate databases. This is the demand driver for cloud based data infrastructure software providers, who can more readily integrate, distribute and process information vs. legacy on-premise software providers.

The 4 data infrastructure stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 1% while next quarter’s revenue guidance was 0.7% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 27.6% since the latest earnings results.

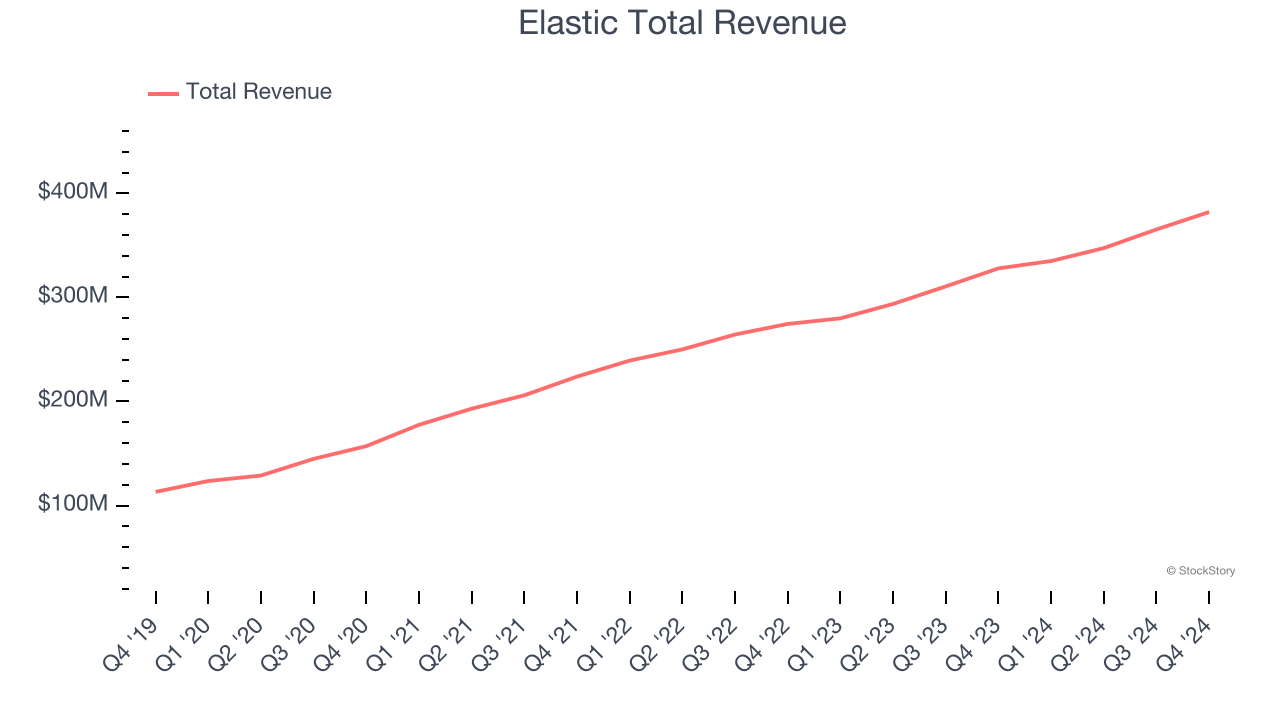

Best Q4: Elastic (NYSE: ESTC)

Started by Shay Banon as a search engine for his wife's growing list of recipes at Le Cordon Bleu cooking school in Paris, Elastic (NYSE: ESTC) helps companies integrate search into their products and monitor their cloud infrastructure.

Elastic reported revenues of $382.1 million, up 16.5% year on year. This print exceeded analysts’ expectations by 3.5%. Overall, it was a strong quarter for the company with a solid beat of analysts’ billings estimates and EPS guidance for next quarter exceeding analysts’ expectations.

“We exceeded guidance across all revenue and profitability metrics in the third quarter. Our results reflect ongoing momentum across all aspects of our business, led by our strong sales execution, continued market demand for our products, and our relentless pace of innovation, reinforcing Elastic as the leader in Search AI,” said Ash Kulkarni, Chief Executive Officer, Elastic.

Elastic achieved the biggest analyst estimates beat and highest full-year guidance raise of the whole group. The company added 40 enterprise customers paying more than $100,000 annually to reach a total of 1,460. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 23.1% since reporting and currently trades at $78.

Is now the time to buy Elastic? Access our full analysis of the earnings results here, it’s free.

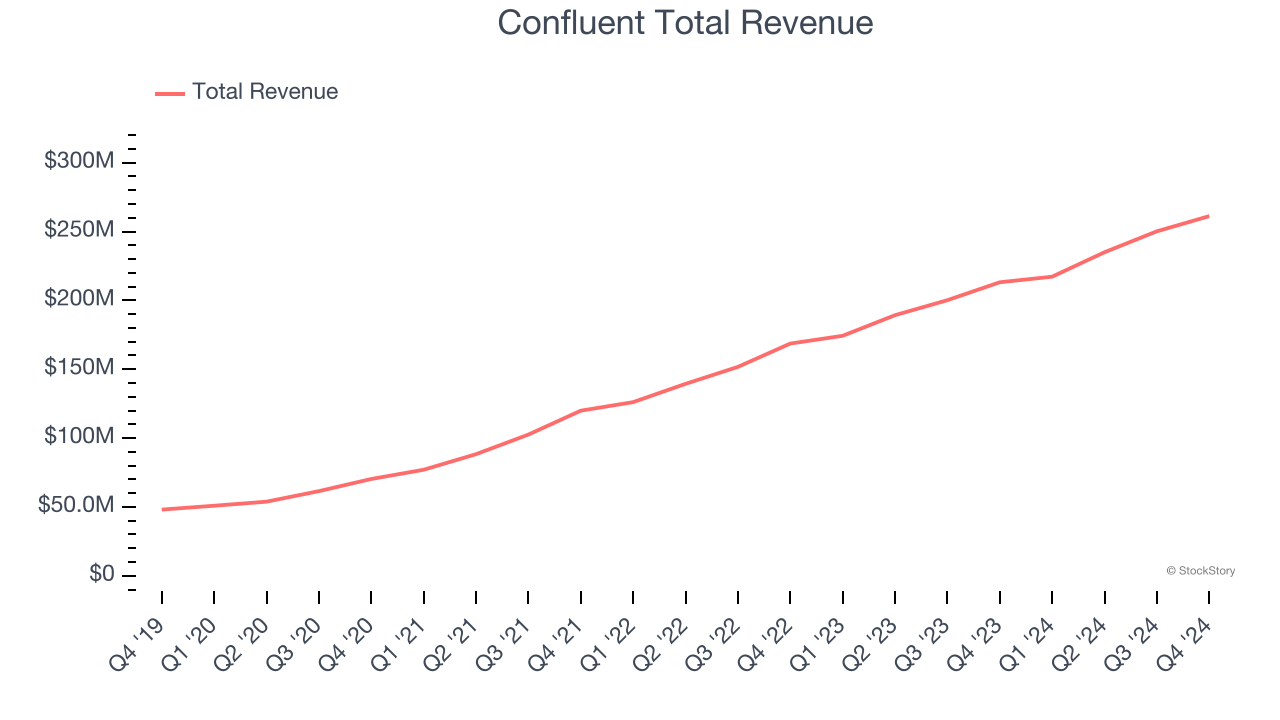

Confluent (NASDAQ: CFLT)

Started in 2014 by the team of engineers at LinkedIn who originally built it as an internal tool, Confluent (NASDAQ: CFLT) provides infrastructure software for organizations that makes it easy and fast to collect and move large amounts of data between different systems.

Confluent reported revenues of $261.2 million, up 22.5% year on year, outperforming analysts’ expectations by 1.7%. The business had a satisfactory quarter with a solid beat of analysts’ billings estimates.

The stock is down 30.6% since reporting. It currently trades at $20.91.

Is now the time to buy Confluent? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Teradata (NYSE: TDC)

Part of point-of-sale and ATM company NCR from 1991 to 2007, Teradata (NYSE: TDC) offers a software-as-service platform that helps organizations manage and analyze their data across multiple storages.

Teradata reported revenues of $409 million, down 10.5% year on year, falling short of analysts’ expectations by 1.5%. It was a disappointing quarter as it posted full-year EPS guidance missing analysts’ expectations.

Teradata delivered the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 33.2% since the results and currently trades at $20.62.

Read our full analysis of Teradata’s results here.

C3.ai (NYSE: AI)

Founded in 2009 by enterprise software veteran Tom Seibel, C3.ai (NYSE: AI) provides software that makes it easy for organizations to add artificial intelligence technology to their applications.

C3.ai reported revenues of $98.78 million, up 26% year on year. This result topped analysts’ expectations by 0.5%. Aside from that, it was a mixed quarter as it also recorded a solid beat of analysts’ EBITDA estimates but a significant miss of analysts’ billings estimates.

C3.ai achieved the fastest revenue growth among its peers. The stock is down 23.5% since reporting and currently trades at $20.26.

Read our full, actionable report on C3.ai here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.