The end of the earnings season is always a good time to take a step back and see who shined (and who didn’t). Let’s take a look at how diversified upstream e&p stocks fared in Q1, starting with ConocoPhillips (NYSE: COP).

Large cap diversified exploration and production (E&P) companies operate global portfolios spanning multiple basins and resource types, providing geographic and commodity diversification. Scale enables operational efficiencies, capital market access, and investment in advanced technologies. Tailwinds include disciplined capital allocation improving shareholder returns, diversified production bases reducing single-asset risk, and strong balance sheets supporting dividend programs. Headwinds include commodity price volatility affecting earnings, regulatory and geopolitical risks across operating regions, and ESG pressures challenging long-term investment theses. The energy transition creates strategic uncertainty around reserve life and future demand trajectories.

The 5 diversified upstream e&p stocks we track reported a very strong Q1. As a group, revenues beat analysts’ consensus estimates by 3.7%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 7.7% since the latest earnings results.

ConocoPhillips (NYSE: COP)

Operating the famous Prudhoe Bay field discovered in 1968 that transformed Alaska's economy, ConocoPhillips (NYSE: COP) explores for and produces crude oil, natural gas, and liquefied natural gas across North America, Europe, Asia, and Africa.

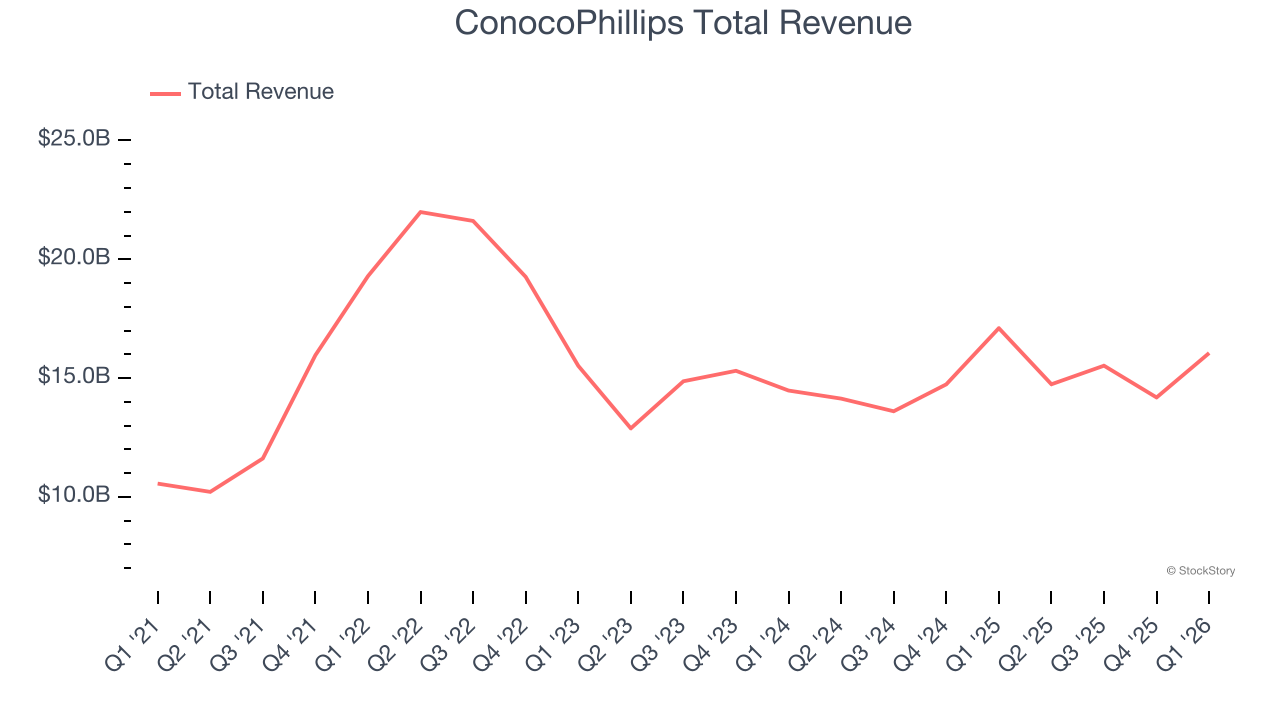

ConocoPhillips reported revenues of $16.05 billion, down 6.1% year on year. This print exceeded analysts’ expectations by 12.1%. Overall, it was a strong quarter for the company with a beat of analysts’ EPS estimates.

ConocoPhillips pulled off the biggest analyst estimate beat of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 10.5% since reporting and currently trades at $114.79.

Best Q1: ExxonMobil (NYSE: XOM)

One of the successor companies to John D. Rockefeller's Standard Oil monopoly that was broken up in 1911, ExxonMobil (NYSE: XOM) explores for and produces crude oil and natural gas, refines and sells petroleum products, and manufactures petrochemicals.

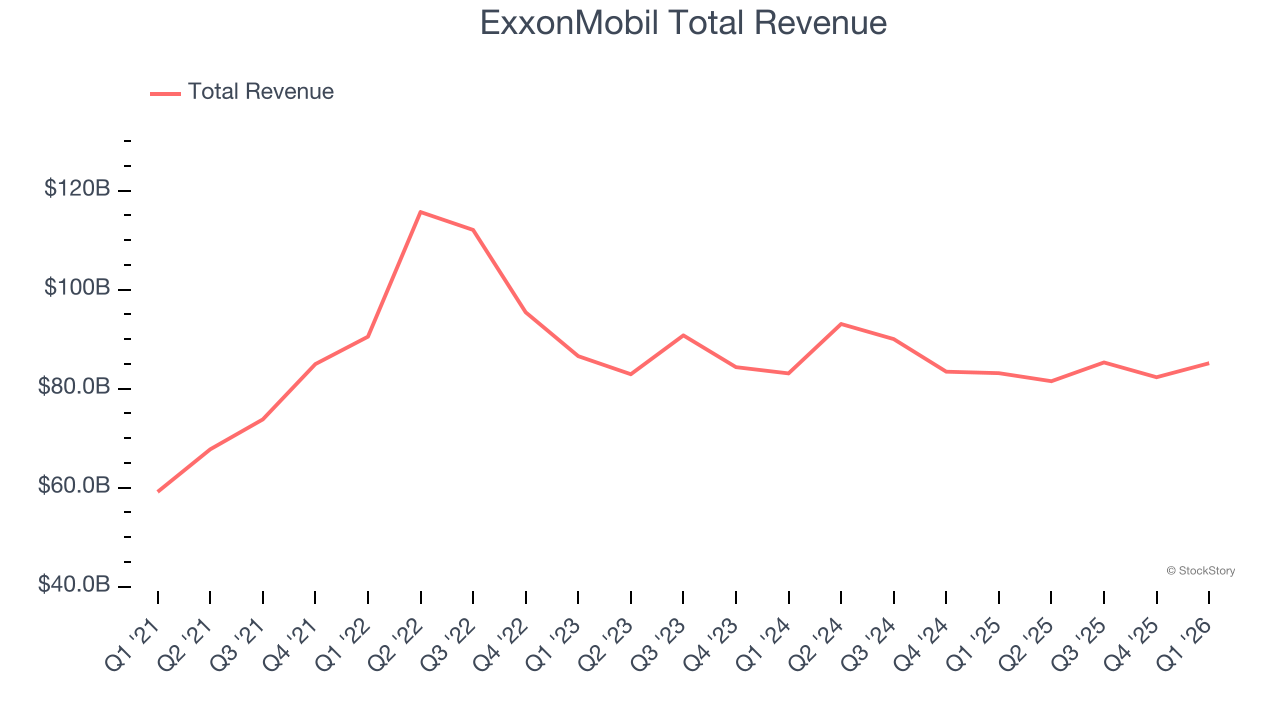

ExxonMobil reported revenues of $85.14 billion, up 2.4% year on year, outperforming analysts’ expectations by 6.7%. The business had an exceptional quarter with a beat of analysts’ EPS and EBITDA estimates.

ExxonMobil delivered the fastest revenue growth among its peers. Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 4.9% since reporting. It currently trades at $146.75.

Is now the time to buy ExxonMobil? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Devon Energy (NYSE: DVN)

With operations spanning from the oil-rich Delaware Basin to the Bakken formation of North Dakota, Devon Energy (NYSE: DVN) explores for and produces oil, natural gas, and natural gas liquids from wells drilled across the United States.

Devon Energy reported revenues of $4.45 billion, down 2% year on year, exceeding analysts’ expectations by 5%. Still, it was a mixed quarter as it posted a miss of analysts’ EBITDA estimates.

As expected, the stock is down 13.6% since the results and currently trades at $44.08.

Read our full analysis of Devon Energy’s results here.

Occidental Petroleum (NYSE: OXY)

Backed by Warren Buffett's Berkshire Hathaway as a major shareholder, Occidental Petroleum (NYSE: OXY) explores for, develops, and produces oil, natural gas liquids, and natural gas, primarily in the United States and Middle East.

Occidental Petroleum reported revenues of $5.11 billion, down 11% year on year. This print lagged analysts’ expectations by 7.5%. Zooming out, it was actually a very strong quarter as it logged a beat of analysts’ EPS and EBITDA estimates.

Occidental Petroleum had the weakest performance against analyst estimates and slowest revenue growth among its peers. The stock is down 3.9% since reporting and currently trades at $57.03.

Read our full, actionable report on Occidental Petroleum here, it’s free.

Chevron (NYSE: CVX)

Operating everything from deepwater drilling rigs to corner gas stations, Chevron (NYSE: CVX) explores for, produces, and transports crude oil and natural gas, then refines that crude oil into gasoline, diesel, and other petroleum products.

Chevron reported revenues of $48.61 billion, up 2.1% year on year. This number beat analysts’ expectations by 2.3%. It was a very strong quarter as it also logged a beat of analysts’ EPS and EBITDA estimates.

The stock is down 5.5% since reporting and currently trades at $182.61.

Read our full, actionable report on Chevron here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.