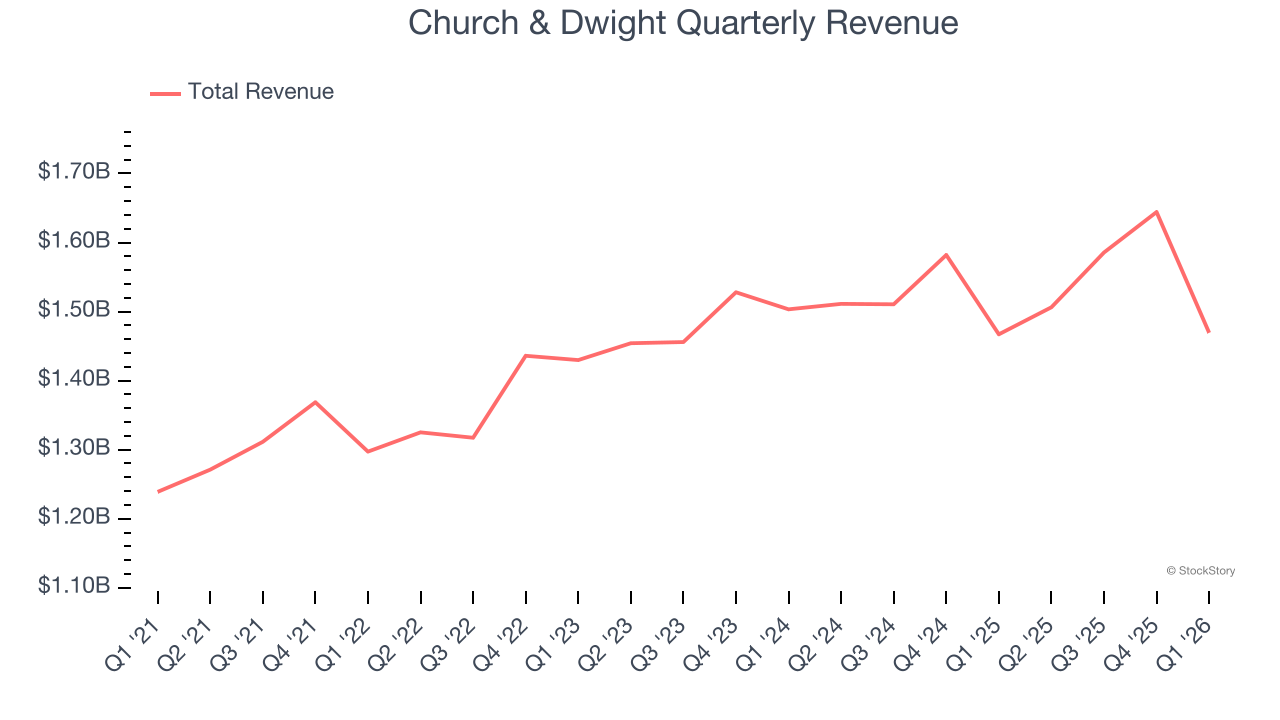

Household products company Church & Dwight (NYSE: CHD) reported Q1 CY2026 results topping the market’s revenue expectations, but sales were flat year on year at $1.47 billion. Its non-GAAP profit of $0.95 per share was 2.3% above analysts’ consensus estimates.

Is now the time to buy Church & Dwight? Find out by accessing our full research report, it’s free.

Church & Dwight (CHD) Q1 CY2026 Highlights:

- Revenue: $1.47 billion vs analyst estimates of $1.46 billion (flat year on year, 0.7% beat)

- Adjusted EPS: $0.95 vs analyst estimates of $0.93 (2.3% beat)

- Adjusted EBITDA: $379.6 million vs analyst estimates of $356.6 million (25.8% margin, 6.4% beat)

- Adjusted EPS guidance for Q2 CY2026 is $0.88 at the midpoint, below analyst estimates of $0.97

- Operating Margin: 19.8%, in line with the same quarter last year

- Free Cash Flow Margin: 9.7%, down from 11.5% in the same quarter last year

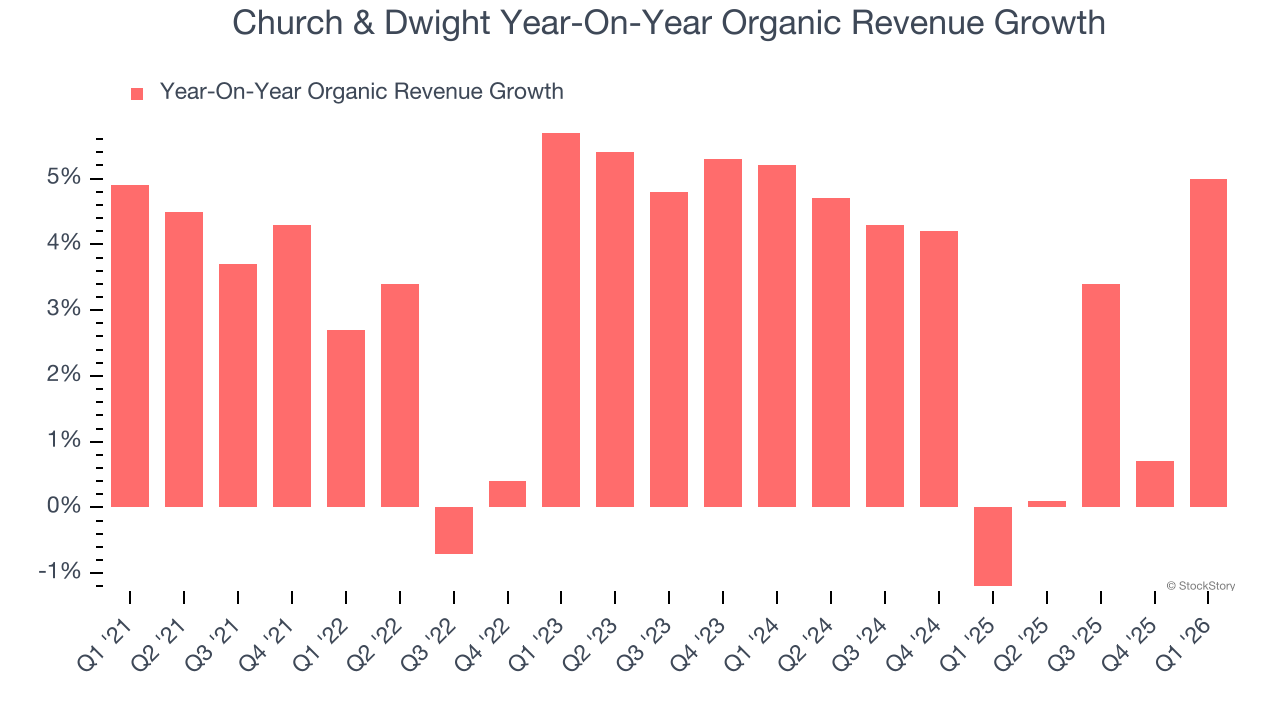

- Organic Revenue rose 5% year on year (beat)

- Market Capitalization: $22.99 billion

Rick Dierker, Chief Executive Officer, commented, “Our brands continue to perform exceptionally well in this dynamic macroeconomic environment. Solid category growth and the performance of our balanced portfolio of value and premium products provide further confidence in our full-year outlook. Our growth was broad-based with volume growth driven by strong innovation and distribution wins across all domestic classes of trade. Our operating model of consistent delivery of sales growth, margin expansion, and efficient working capital management leads to strong cash flow generation, fueling our investments in our existing brands and the acquisition of market leading new brands.

Company Overview

Best known for its Arm & Hammer baking soda, Church & Dwight (NYSE: CHD) is a household and personal care products company with a vast portfolio that spans laundry detergent to toothbrushes to hair removal creams.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $6.21 billion in revenue over the past 12 months, Church & Dwight carries some recognizable products but is a mid-sized consumer staples company. Its size could bring disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale.

As you can see below, Church & Dwight’s sales grew at a sluggish 4.1% compounded annual growth rate over the last three years. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

This quarter, Church & Dwight’s $1.47 billion of revenue was flat year on year but beat Wall Street’s estimates by 0.7%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and indicates its products will face some demand challenges.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Organic Revenue Growth

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

The demand for Church & Dwight’s products has generally risen over the last two years but lagged behind the broader sector. On average, the company’s organic sales have grown by 2.6% year on year.

In the latest quarter, Church & Dwight’s organic sales rose by 5% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

Key Takeaways from Church & Dwight’s Q1 Results

We enjoyed seeing Church & Dwight beat analysts’ organic revenue expectations this quarter. We were also happy its EPS outperformed Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed. Overall, this print still had some key positives. The stock traded up 4% to $100.94 immediately following the results.

So do we think Church & Dwight is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).