Infrastructure and defense services provider Parsons (NYSE: PSN) fell short of the market’s revenue expectations in Q1 CY2026, with sales falling 4.1% year on year to $1.49 billion. On the other hand, the company’s outlook for the full year was close to analysts’ estimates with revenue guided to $6.65 billion at the midpoint. Its non-GAAP profit of $0.79 per share was 15.6% above analysts’ consensus estimates.

Is now the time to buy Parsons? Find out by accessing our full research report, it’s free.

Parsons (PSN) Q1 CY2026 Highlights:

- Revenue: $1.49 billion vs analyst estimates of $1.5 billion (4.1% year-on-year decline, 0.5% miss)

- Adjusted EPS: $0.79 vs analyst estimates of $0.68 (15.6% beat)

- Adjusted EBITDA: $150.9 million vs analyst estimates of $142.8 million (10.1% margin, 5.7% beat)

- The company reconfirmed its revenue guidance for the full year of $6.65 billion at the midpoint

- EBITDA guidance for the full year is $645 million at the midpoint, below analyst estimates of $649.4 million

- Operating Margin: 6.4%, in line with the same quarter last year

- Free Cash Flow was -$18.62 million compared to -$25.26 million in the same quarter last year

- Backlog: $9.31 billion at quarter end, up 2.3% year on year

- Market Capitalization: $5.55 billion

“Our first quarter results highlighted the resilience of our business and our team's high level of execution, as we delivered our highest adjusted EBITDA margin ever, reached record levels for both total and funded backlog, achieved a robust book-to-bill ratio of 1.4x in both segments, and generated record first quarter cash flow. Revenue performance was in line with our expectations, and we continued to complement our organic growth with strategic, accretive acquisitions that enhance our differentiation and drive long-term shareholder value," said Carey Smith, chair, president, and chief executive officer.

Company Overview

Delivering aerospace technology during the Cold War-era, Parsons (NYSE: PSN) offers engineering, construction, and cybersecurity solutions for the infrastructure and defense sectors.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, Parsons’s 10.5% annualized revenue growth over the last five years was impressive. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Parsons’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 4.2% over the last two years was well below its five-year trend.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Parsons’s backlog reached $9.31 billion in the latest quarter and was flat over the last two years. Because this number is lower than its revenue growth, we can see the company hasn’t secured enough new orders to maintain its growth rate in the future.

This quarter, Parsons missed Wall Street’s estimates and reported a rather uninspiring 4.1% year-on-year revenue decline, generating $1.49 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 8.4% over the next 12 months, an improvement versus the last two years. This projection is above average for the sector and indicates its newer products and services will spur better top-line performance.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Parsons was profitable over the last five years but held back by its large cost base. Its average operating margin of 5.6% was weak for an industrials business.

On the plus side, Parsons’s operating margin rose by 2.6 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q1, Parsons generated an operating margin profit margin of 6.4%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

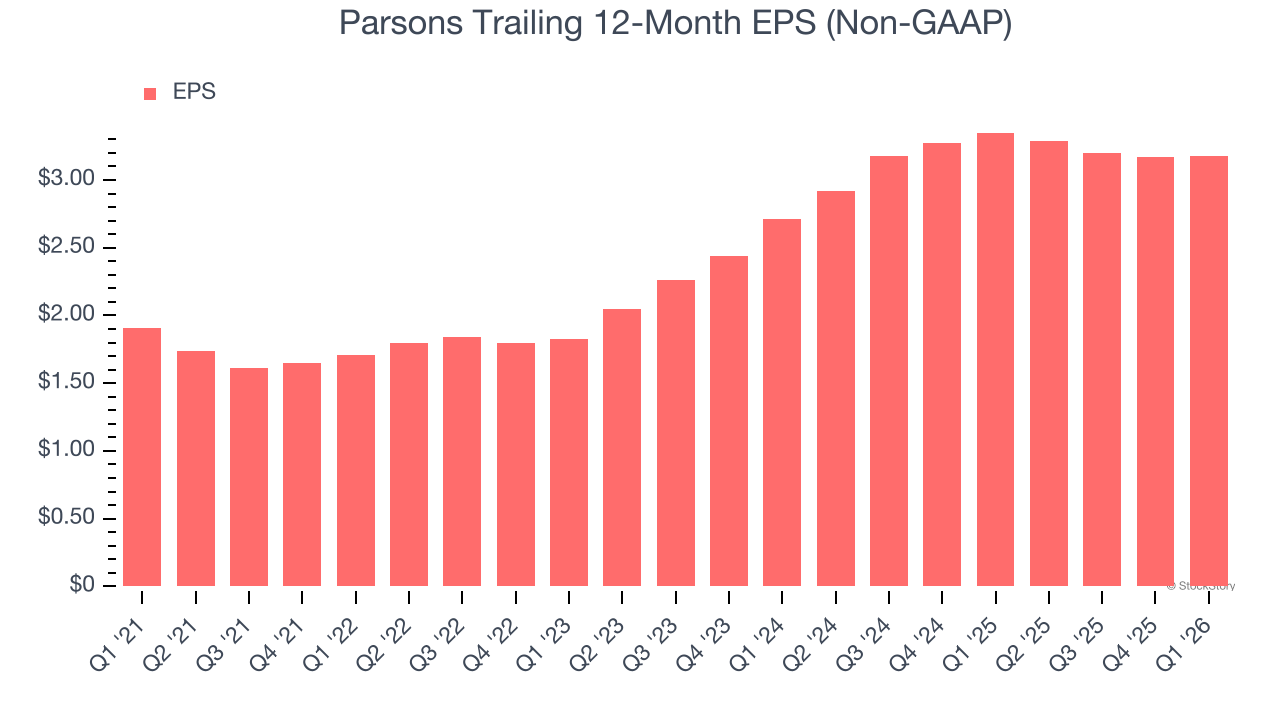

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Parsons’s solid 10.7% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Parsons’s two-year annual EPS growth of 8.3% was decent and topped its 4.2% two-year revenue growth.

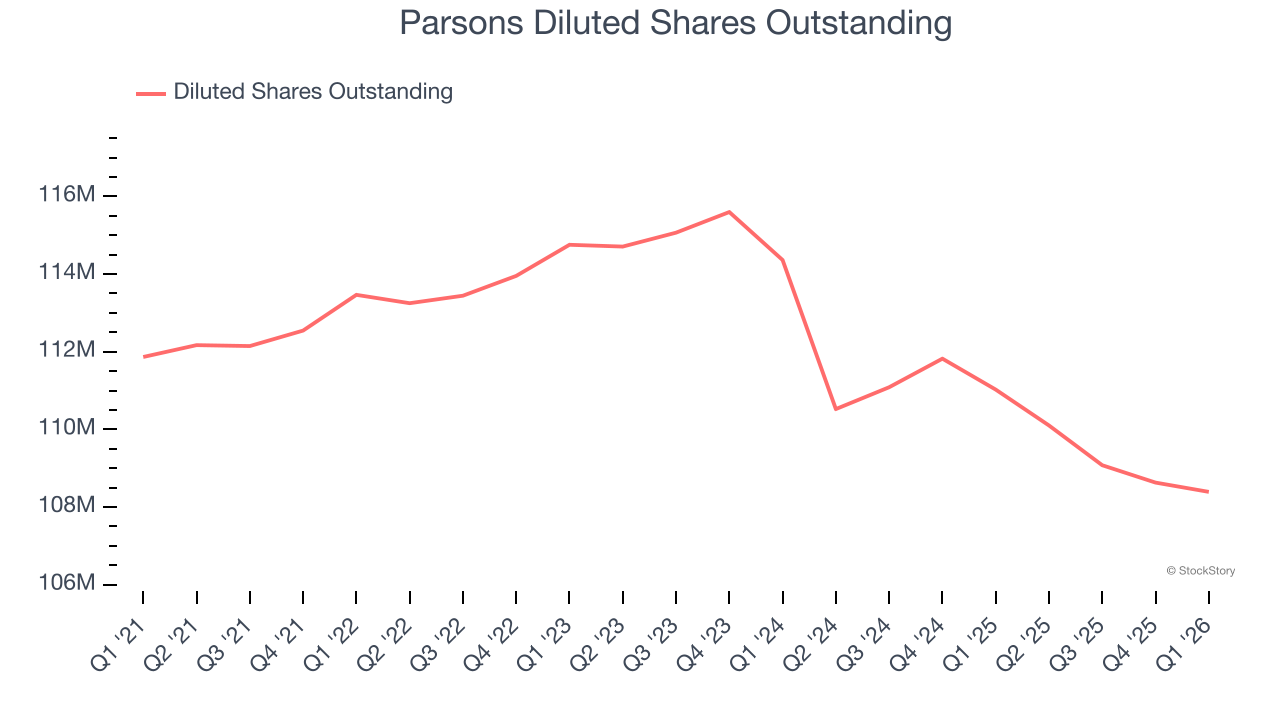

We can take a deeper look into Parsons’s earnings quality to better understand the drivers of its performance. A two-year view shows that Parsons has repurchased its stock, shrinking its share count by 5.2%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q1, Parsons reported adjusted EPS of $0.79, up from $0.78 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Parsons’s full-year EPS of $3.18 to grow 6%.

Key Takeaways from Parsons’s Q1 Results

We were impressed by how significantly Parsons blew past analysts’ adjusted operating income expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. On the other hand, its revenue slightly missed and its full-year EBITDA guidance fell slightly short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock traded up 2.7% to $53.28 immediately following the results.

Sure, Parsons had a solid quarter, but if we look at the bigger picture, is this stock a buy? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).